Weekly Musings from the Desk | 21 Mar — 25 Apr 2026 (5-Week Issue)

Tau Strategy16 min read·Just now

Tau Strategy16 min read·Just now--

Macro

For a few sessions in late March, markets stopped trading like a collection of asset classes and started behaving like one giant margin call. The usual distinctions between hedge, haven, inflation protection and growth exposure suddenly mattered less than one brutal question: what could still be sold? Gold, which had spent months reinforcing its role as the obvious geopolitical hedge, was dumped hard. Bonds failed to offer much shelter. Equities buckled. The dollar regained its bite. And through that entire stretch, oil kept climbing, turning from an inflation input into the market’s single most important signal. April, in that sense, was defined by two extremes: market-wide liquidation and a violent snapback. What linked them was a macro backdrop still warped by war-driven instability and the energy shock, and still far from delivering the kind of convincing repair that the recovery in price seemed to celebrate.

The stress phase exposed how fragile the old macro playbook had become. Once the oil shock arrived with enough force to rewrite the inflation conversation almost overnight, the unwind spread exactly where these episodes usually spread: through crowded positions, laggard sectors that had only recently started catching a bid, and the high-Sharpe winners of late Q4 and early Q1 that could be sold quickly to raise cash. WTI’s 34.5% surge in five days and Brent’s sprint from the low-$70s to above $110 forced investors to confront a much harsher mix than the one they had been carrying through most of the first quarter: higher energy costs, tighter financial conditions, and far less room for central banks to cushion the damage. Gold then delivered its worst weekly drop in roughly 43 years, falling around 9.5% to 11% toward the $4,490 area, while silver collapsed by roughly 16% in a day. That was not a calm macro rotation. It was a forced-selling cascade through positions that had become too comfortable, too consensus and too easy to finance.

The economic backdrop never fully validated either extreme of the debate. It was not a clean deterioration story, but neither was it the kind of reacceleration that would naturally justify the velocity of the rebound that followed. In the U.S., activity data held up better than the tone of the tape implied. ISM manufacturing beat expectations, and composite PMI also surprised to the upside, leaving the aggregate growth pulse more resilient than many had feared during the initial oil panic. But the labor market looked softer once one moved beneath the headline prints. Downward revisions to prior payrolls offset much of the apparent strength, healthcare hiring was flattered by strike normalization, weather-sensitive sectors accounted for a disproportionate share of the rebound, participation drifted lower, and wage growth eased to roughly 3.5%. The result was a labor market that still looked functional at the surface but softer in composition — enough to cool the clean-growth narrative without fully collapsing it.

Inflation added another layer of discomfort. Headline CPI around 3.3% year-on-year came in around expectations, but that was hardly a clean all-clear once the energy shock was layered on top. Cleveland Fed tracking pointed toward March PCE running hot on a monthly basis, while the broader inflation path was revised higher through the second and third quarters. Core goods softened, but largely because demand was absorbing pressure rather than because policy had created real relief. Shelter remained the dominant services anchor, and even if parts of the owners’ equivalent rent story still look more statistical than fundamental, the practical consequence for the market was straightforward: inflation may be moving toward a peak, but it is not convincingly behind us yet. The best interpretation of the U.S. macro mix was therefore divergence rather than deterioration — resilient activity, cooling labor internals, and an inflation peak that may be approaching, assuming geopolitics does not re-intensify.

China mucks the picture further. The first-quarter GDP print of 5.0% looked reassuring at first glance and helped calm the most immediate fears of a global demand break. But the internals told a less comforting story. March exports slowed sharply to 2.5% year-on-year after the earlier AI-driven surge, missing expectations badly, while imports jumped 27.8% as the commodity bill rose and the trade surplus narrowed. Retail demand and fixed-asset investment remained soft, and property stayed deeply negative. That is not a classic recovery profile. It is a picture of selective industrial strength trying to offset softer domestic demand and a tougher external environment. The takeaway was not that China had rolled over, but that the global macro backdrop remained far more fragile beneath the headline growth prints than surface optimism suggested.

The rates market bore the brunt of this tension. Earlier in the oil shock, the front end repriced sharply as traders took out easing hopes on the curve, with the U.S. 2-year yield rising more than 55 basis points as crude pushed inflation risk back to the center of the policy debate. By late April, only a small portion of that move had retraced. Yields had stopped panicking higher, but they remained elevated enough to remind investors that this was not the sort of risk episode that automatically invites a dovish rescue. The Fed still appears stuck in wait-and-see mode, with labor softening on one side and energy-driven inflation risk on the other. The probability-weighted path may still be somewhat more dovish than the market’s most hawkish pricing implies, especially if labor weakens further or inflation peaks cleanly into the summer, but the distribution of risks has clearly widened in both directions. That alone is enough to keep policy from acting as a comfy backstop.

Warsh’s confirmation hearing hammered on that message without fully changing the near-term story. His four themes — central-bank independence, institutional regime change, staying in the Fed’s lane, and a preference for rate tools over routine balance-sheet activism — were each orthodox in isolation. Taken together, they implied a more ambiguous policy architecture than markets have grown used to. He gave no clean signal on the rate path, linked rate decisions to balance-sheet choices, and appeared more interested in redesigning the communication and institutional framework than in promising any immediate easing bias. The implication is less about a near-term rate surprise than about the nature of the next backstop: likely narrower, less theatrical, and less instinctively market-soothing than the post-crisis Fed model investors have internalized.

FX told the same story in a different twang. The dollar’s March rally was never a vote of confidence in the U.S. economy. It was the sound of the global system reaching for the deepest pool of liquidity when hedges were failing everywhere else. As the conflict escalated and crude surged, the U.S. benefited from better relative terms of trade than energy importers, the hawkish repricing of Fed expectations restored a rate-differential anchor, and an already crowded dollar short was violently unwound. DXY pushed back above 100 and held the squeeze through late March and into early April. The ceasefire then marked the inflection, and the dollar retraced much of the conflict-driven impulse. Even so, the moderation felt more like technical cooling than the return of a clean anti-dollar regime. FX stopped confirming acute stress; it did not begin confirming a simple new macro expansion.

Commodities were where the contradictions were laid bare. Crude was the only asset that consistently behaved like a genuine geopolitical hedge during the stress phase, and that very success worsened the broader macro picture by tightening financial conditions and pushing inflation expectations higher. Oil then peaked on April 7, one day before the ceasefire, and began to retrace as de-escalation took hold. Gold told the opposite story. It failed precisely when it was most needed, exposing how much of the precious-metals complex had turned into a crowded expression of comfort rather than a robust absorber of stress. Yet gold also bottomed early, reversing sharply on March 23 and recovering well before the broader market restored calm. That sequence matters. It suggests the liquidation was more positioning-driven than fundamental. Once the forced selling cleared and real yields stabilized, the structural bid underneath gold re-emerged. Across oil, gold and the dollar, the unwind did not happen in unison; it happened in the order that each asset’s positioning had become most distorted.

Then there was equity telling the two stories in sequence. The first was capitulation. The second was momentum. Once markets decided that the conflict was more likely to settle into a prolonged impasse than explode into a true worst-case escalation, the rebound became ferocious. The Nasdaq’s 12- and then 13-session winning streak captured the speed of the move, but the mechanics underneath mattered just as much. This was one of the fastest recoveries on record because it was powered by the collision of underexposed positioning, systematic buying and earnings momentum at precisely the moment new highs were being reclaimed. Prime desks recorded the first net buy in U.S. equities in roughly two months, initially driven more by short covering than by aggressive new long addition, and institutional leverage remained relatively lean heading into earnings season. That is a powerful setup when results come in strong: positive surprises force re-grossing and chase, while disappointments do not require much new selling because the community was already light.

Sector leadership also became much clearer as the rebound matured. Energy, which had led through the stress phase as the clean beneficiary of the geopolitical premium, began correcting as de-escalation set in, rotating from leadership into a source of funds. Software remained under pressure even after a partial rebound, while AI infrastructure, semis and large-cap hardware regained sponsorship quickly. That divergence had been understood conceptually for some time; in April it became operationally visible in positioning and then validated by earnings. Across the hardware chain, beats from the key semiconductor and infrastructure names were strong enough to force immediate upward revisions, and the common thread was unmistakable: AI-driven demand remained the dominant revenue accelerator, data-center demand was still the fastest-growing end market, and management commentary continued to point to demand running ahead of supply. That means the rally should not be dismissed as purely mechanical. Positioning helped ignite it, but earnings in the right parts of the index gave it real fuel.

Given the speed of the recent recovery, some caution is warranted. The medium-term macro backdrop still looks compromised. The US economy has yet to show the kind of clean reacceleration that would justify a durable and uncomplicated bullish reset. Oil and inflation have not disappeared as constraints, and the Fed is still boxed in. For all its woes, markets do not need those issues fully resolved to extend further in the near term. With highs reclaimed, technicals improving, institutional exposure still far from stretched, and earnings in the most important parts of the index continuing to deliver, this can still develop into a highly tradable momentum extension, even if the grimmer arithmetic returns later in the year. That is probably the most powerful conclusion from the past five weeks. The liquidation exposed a broken cross-asset regime; the rebound showed how far price can travel anyway. For now, dips still look more buyable than shortable — but that judgment rests on momentum, flows and earnings, not on any genuine repair in the macro foundation.

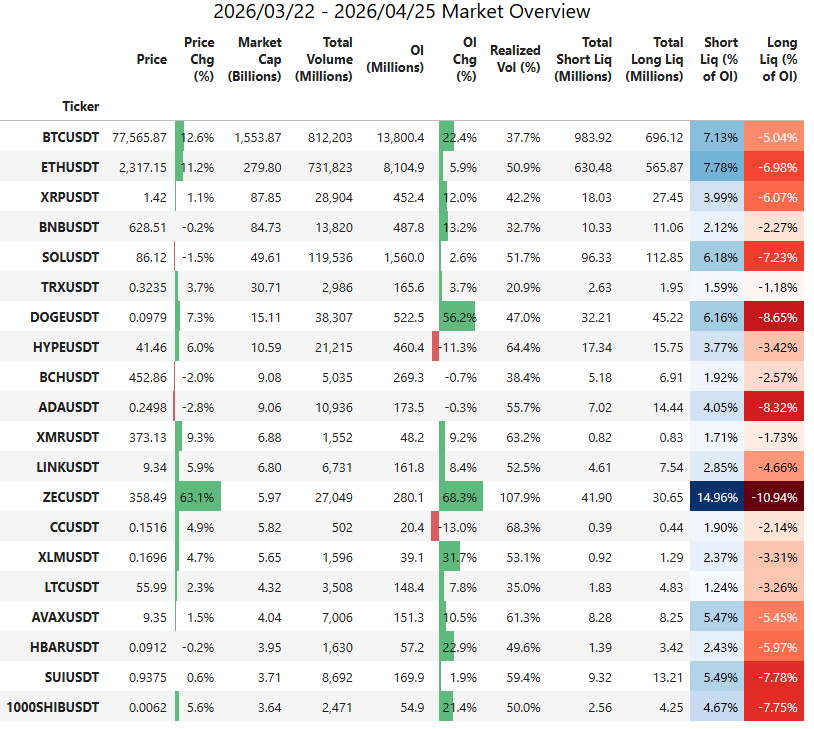

Crypto

The cryptocurrency market staged a measured recovery between March 22 and April 25, 2026, following the sharp deleveraging seen earlier in the quarter, though the rebound was neither linear nor broadly distributed. Bitcoin climbed from the mid-$60,000 range at the end of March to test the high-$70,000 area by late April, briefly approaching $79,000 — its highest level in nearly three months — before consolidating just below that threshold. Ethereum followed with a more muted advance, rising from roughly $2,000 to the $2,300 area, continuing its pattern of lagging the benchmark asset.

The recovery unfolded against a backdrop of easing but still-fragile macro conditions. A partial de-escalation in Middle East tensions, including an extension of a ceasefire involving Iran, helped stabilize energy markets and revive broader risk appetite. Crypto assets, which had traded as high-beta expressions of macro sentiment earlier in the year, participated in this shift, with Bitcoin rallying more than 20% from its late-March lows. Importantly, this period also reinforced Bitcoin’s evolving role within the broader macro landscape. While it has yet to demonstrate the consistency required of a true safe-haven asset, it is increasingly difficult to characterize it as merely a high-beta proxy for risk. Instead, Bitcoin is beginning to occupy a more nuanced middle ground, functioning as a form of alternative monetary-risk asset that can attract institutional demand even in uncertain macro conditions. At the same time, global markets saw a renewed bid for speculative assets, including high-growth equities, reflecting a tentative re-engagement with risk across asset classes.

At the same time, the period exposed fragilities in traditional hedging relationships. Gold, which had been expected to provide a defensive offset, experienced episodes of liquidity-driven selling during peak stress as investors unwound profitable positions to meet margin calls. Against that backdrop, Bitcoin’s relative resilience — despite its volatility — stood out, contributing to the perception that it can serve as a complementary, if still imperfect, hedge within a diversified macro portfolio.

Institutional flows re-emerged as a central driver, marking a notable inflection from the outflow-dominated environment of February. U.S. spot Bitcoin ETFs recorded approximately $1.32 billion in net inflows in March, ending a four-month streak of redemptions and signaling a return of demand from large allocators. This momentum extended into April, with multiple sessions of sizable inflows — including single-day additions exceeding $600 million on April 17 — and cumulative flows reaching into $3.81 billion over the March–April window. These inflows provided a structural bid for Bitcoin, tightening available supply and reinforcing the perception that institutional capital continues to anchor market liquidity. This growing influence of ETF flows also points to a deeper shift in how price discovery is occurring. Bitcoin’s recent price behavior increasingly reflects institutional rebalancing activity rather than purely momentum-driven or retail-led dynamics, effectively establishing an “ETF anchor” that provides a more stable layer of demand during periods of market stress. As a result, price formation has become more structurally grounded, with large allocators playing a more consistent role in defining support levels.

However, the flow picture remained uneven. Periodic outflows persisted, including notable redemptions at the start of April and intermittent daily withdrawals mid-month, highlighting the still-tactical nature of institutional positioning. This push-pull dynamic was reflected in price action, which alternated between momentum-driven advances and consolidation phases rather than establishing a sustained breakout trend.

Microstructure developments suggest that the market entered a cleaner but more fragile state. Following the sharp reduction in leverage during February and early March, derivatives positioning stabilized at lower levels. While comprehensive open interest data remained below prior peaks, the market exhibited signs of rebuilding activity through episodic short squeezes that contributed to upward price momentum, particularly as Bitcoin approached the $75,000–$80,000 range. The presence of such squeezes indicates that positioning remained skewed enough to fuel sharp moves, though not to the extent seen during earlier phases of the cycle.

Ethereum’s performance remained comparatively subdued throughout the period. Despite participating in the broader recovery, ETH failed to exhibit the same degree of institutional sponsorship as Bitcoin, with ETF flows and on-chain activity lagging. The ETH/BTC ratio remained near cycle lows, reflecting persistent relative weakness and reinforcing the market’s preference for Bitcoin as the primary vehicle for directional exposure.

Across the altcoin complex, rotational themes have been mixed and cross-sectional dispersions pronounced. Large-cap tokens such as Solana and XRP tracked Bitcoin’s directional moves but with higher volatility and weaker follow-through. Select pockets of strength emerged in narrative-driven segments — including AI-linked tokens and certain Layer-1 ecosystems — though these rallies were episodic rather than indicative of a broad-based rotation into risk. Market breadth remained narrow, with liquidity concentrated in a limited set of high-conviction assets. This concentration of liquidity had pronounced consequences in the long tail of the market. Lower-liquidity tokens proved particularly vulnerable, with some names such as RAVE and ARIA experiencing drawdowns of up to 90% as modest selling pressure overwhelmed limited market depth. These moves were less indicative of project-specific deterioration and more reflective of structural illiquidity in an environment where capital allocation remained highly selective.

At the same time, pockets of structural fragility within the altcoin ecosystem further weighed on sentiment. Security breaches at protocols such as Drift Protocol (~$270 million) and KelpDAO (~$290 million) exposed vulnerabilities within the DeFi and liquid restaking stack, prompting a more defensive posture across on-chain lending markets. Major platforms such as Aave effectively acted as system backstops by tightening risk parameters, reinforcing the cautious tone across higher-risk segments of the market. More speculative sectors continued to lag. Memecoins, NFTs and lower-cap tokens saw limited participation, reflecting a structural shift in retail behavior and a still-constrained liquidity environment. While total market capitalization recovered modestly from March lows, trading volumes remained below earlier peaks, suggesting that the rebound was driven more by incremental institutional flows than by a full return of speculative demand.

A broader structural shift is also becoming harder to ignore: stablecoins are increasingly central to crypto market liquidity. Regulatory debates in April underscored that point, with policymakers raising concerns over monetary transmission, market fragmentation and the risk of cross-border dollarization as stablecoin adoption expands. That does not suggest stablecoins were the primary catalyst behind the recent rally — they were not. But it does highlight how crypto’s internal market infrastructure has matured. Capital can now remain within the ecosystem, move rapidly when sentiment improves and provide a deeper pool of liquidity even as the broader macro backdrop remains fragile. In practical terms, that helps explain why Bitcoin was able to regain momentum without requiring a repeat of the broad-based speculative frenzy seen across digital assets in 2021. Liquidity channels are more developed than in previous cycles, even as market leadership remains concentrated.

Looking ahead to May, the balance of risks appears more evenly distributed than earlier in the quarter. On the constructive side, the re-emergence of ETF inflows, tightening supply conditions and reduced leverage provide a more stable foundation for further gains. A sustained breakout from the current range, however, would likely require a continuation of these supporting factors rather than a material improvement in macro conditions. In particular, ongoing institutional sponsorship via ETF inflows, the absence of renewed geopolitical shocks, and a macro backdrop that remains stable — if not outright supportive — would be sufficient to extend the rally. In that sense, further upside does not depend on a clean “risk-on” environment, but rather on the persistence of incremental demand within an only partially healed macro landscape.

At the same time, the absence of a decisive macro catalyst — particularly around monetary policy — continues to limit upside conviction. ETF flows remain the key marginal driver, but their inconsistency underscores the fragility of sentiment. Should macro conditions deteriorate or geopolitical risks re-escalate, the market remains vulnerable to renewed volatility, particularly given the still-muted participation in higher-beta segments.

In that context, Bitcoin is likely to retain its leadership role as the preferred institutional asset, benefiting from both liquidity depth and structural demand via ETFs. Ethereum and the broader altcoin complex may continue to lag until clearer evidence of sustained risk appetite and capital rotation emerges. The market’s trajectory into May will therefore depend less on internal crypto developments and more on whether the tentative stabilization in global macro conditions can evolve into a durable risk-on environment.

Crypto Vol

The volatility complex over these five weeks traced a path from residual stress to controlled optimism, completing the bottoming unwind that February’s selloff had first set in motion. What emerged felt not so much like complacency — implied volatility (‘IV’) did not collapse to indifferent lows — but a definitive break from panic pricing of protection even as the macro backdrop never fully tidied up. Across the board in option space, the same theme has increasingly manifested. What ensued was a market being comfortable with a constructive push higher rather than aggressively paying for downside protection.

BTC front-month ATM IV compressed from 54 vol on March 22 to roughly 41 vol by April 24 — a 13 vol normalization that broadly tracked the recovery in spot, which advanced from 69K to 78K. The front-week ATM collapse was even more striking, sliding from 59 vol to below 35 vol as realized volatility (‘RV’) faded into the rally; what had been a 50-handle RV at the open of the window settled below 35% by the end of the five weeks. With RV printing in the mid-30s against IV in the low 40s, the volatility risk premium (‘VRP’) remained healthier than the razor-thin December levels but offered no obvious carry edge.

ETH traced a parallel decompression with call skews visibly more bid in comparison to BTC. ETH 30-day ATM IV eased from 76 vol to 62 vol, a similar absolute move to BTC’s, yet on a relative basis ETH underperformed BTC’s vol compression. ETF inflows put a credible floor under price, but the options tape never priced leadership; ETH stayed caught between reduced panic and unconvinced upside. ETH vol can decline alongside BTC vol without implying the same quality of conviction underneath, and through this period it did precisely that.

BTC front-month 25-delta skew (put-over-call) tightened but never flipped positive even with spot grinding to multi-week highs. Traders stopped paying as much for downside protection but never started paying meaningfully for upside skew. ETH 25-delta skew was the more interesting reading: it tightened from roughly 5 vol at the end of March to near flat at sub-1 vol on April 17 right before breaking 2300, then re-widened sharply back to 5 vols by April 23 as ETH’s late-April rally lost momentum, the precise asymmetry consistent with the broader read that ETH never fully escaped its identity problem during this period.

Block flow through the window traced the same arc. The put-call ratio on the block tape compressed from 1.6 into the 0.5–0.6 range from early April onward, a clear directional repricing of demand for downside protection. Dealer is long gamma in a narrow pocket from 78K to 80K and short gamma from 75K and below, with the heaviest short pockets clustered at 68K to 75K. Above the long pocket, the exposure thins quickly. ETH shares a similar profile where short gamma mostly concentrates near topside at 2300 and 2400.

From a tactical perspective, that leaves crypto vol in a much more nuanced place than a simple ‘vol lower -> better risk-adjusted return -> bullish’ reading would suggest. The short-term message is constructive. As long as BTC continues to absorb macro stress better than the rest of the cross-asset complex, IV can remain suppressed enough to support a grind higher, and lower crash premia can continue drawing traders back into more directional expressions. But the medium-term caution should also be obvious. The same macro variables that broke the cross-asset map in March — oil, rates, dollar stress, geopolitical headlines — have not disappeared. They have merely simmered in price terms. If those variables re-accelerate, vol can reprice far faster than the current calm implies.

That puts us in a delicate balance where crypto vol no longer reflects a market bracing for imminent disorder, and that shift is real; yet it also does not reflect a market that has fully escaped macro gravity. The best way to describe the current state is rented calm: stable enough to trade, constructive enough to respect, but not the kind of low-vol regime that invites an ambitious extrapolation. At least for now, volatility is confirming the momentum extension, but its durability is by no means guaranteed.