Member-only story

The Bond Market Hides Far More Than 3 Factors — I Built a Trading Bot to Prove It

Javier Santiago Gastón de Iriarte Cabrera20 min read·Just now

Javier Santiago Gastón de Iriarte Cabrera20 min read·Just now--

How a 2026 Mathematical Finance paper blew up three decades of conventional wisdom — and how we turned the math into a working MQL5 Expert Advisor

Quantitative Trading · June 2026

Everyone in fixed income knows the story. Robert Litterman and José Scheinkman showed in 1991 that three principal components — level, slope, and curvature — explain over 99% of the variance in bond yields. Three factors. Done. Move on.

For thirty years, this became axiomatic. Risk desks built three-factor hedges. Asset managers built three-factor attribution models. Quants built three-factor trading strategies.

There is just one problem: it was always an artifact of the data transformation, not a real property of bond markets.

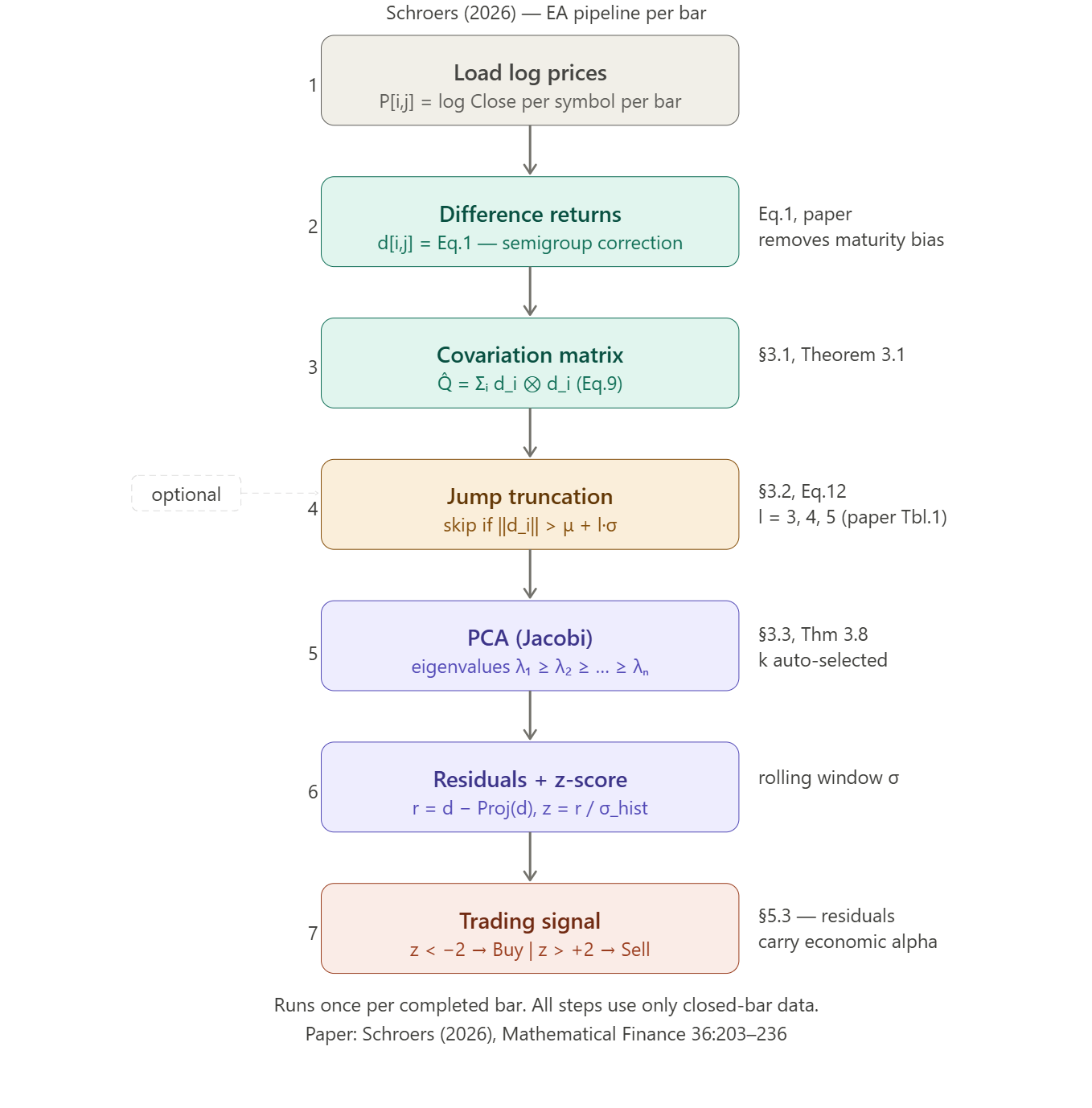

A paper published in 2026 in Mathematical Finance by Dennis Schroers (University of Bonn) tears this assumption apart from first principles. The paper is dense — 34 pages, Hilbert spaces, Jacobi eigendecompositions, infinite-dimensional semimartingales. But buried in the mathematical machinery is something genuinely tradeable: a nonparametric framework that reveals the true number of random drivers in bond markets, and a method for identifying when any single maturity is misbehaving relative to the others.

In this article, I will explain the key insight of the paper in plain terms, show you the exact math that makes it work, walk through the…