You’re Already Using NFC Payments - But Most Apps Are Designed to Increase Spending

EncodeDots4 min read·Just now

EncodeDots4 min read·Just now--

Speed is no longer a differentiator in digital payments.

With platforms like Google Pay and Apple Pay, users expect transactions to happen instantly. NFC (Near Field Communication) technology has made that expectation a standard.

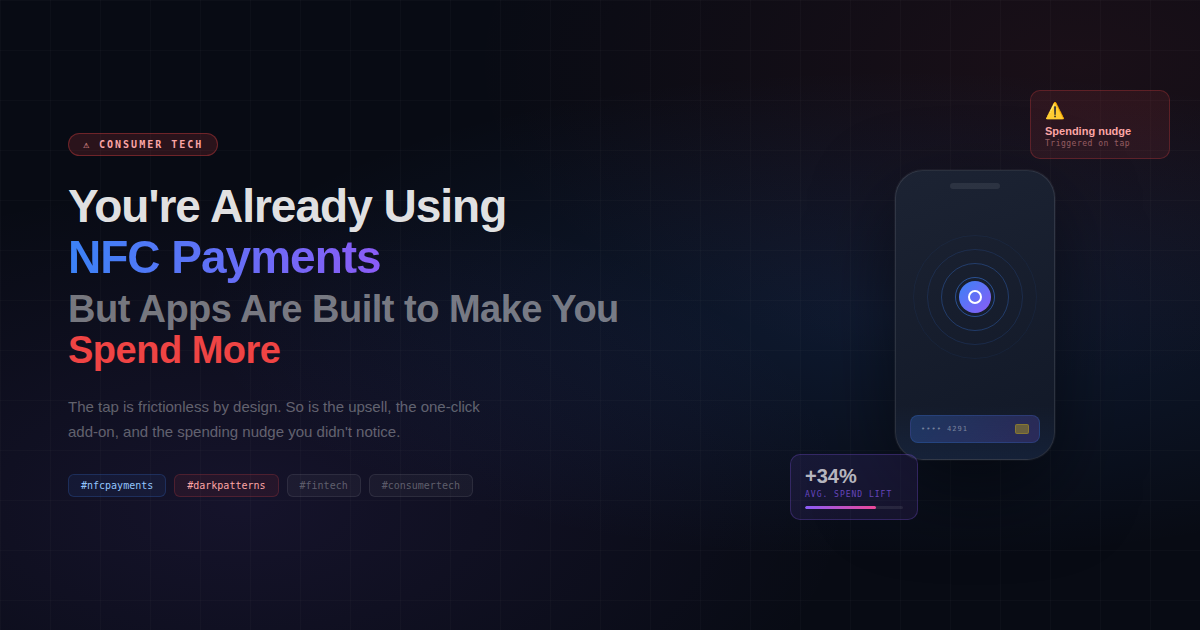

But as payments become faster, a new problem emerges - one that most fintech products overlook:

Loss of user control during transactions

This is where the real opportunity - and challenge - lies.

How NFC Payment Systems Actually Work

Before diving into product strategy, it’s important to understand the foundation.

NFC payments rely on short-range wireless communication between a device (smartphone, smartwatch, or card) and a payment terminal. When a user taps their device:

- The NFC chip transmits encrypted payment data

- Tokenization replaces sensitive card information

- The payment gateway processes the transaction

- Authentication (biometric/PIN) verifies the user

This entire process takes seconds - often less than two.

From a technical perspective, modern NFC systems include:

- Tokenization layers (PCI-DSS compliant)

- Secure Element (SE) or Host Card Emulation (HCE)

- Biometric authentication (Face ID/fingerprint)

- Real-time transaction APIs

This makes NFC payments not just fast, but also highly secure.

The Behavioral Gap: Where Technology Outpaces Awareness

While the technology is advanced, user behavior hasn’t evolved at the same pace.

Traditional payment methods created friction:

- Entering PINs

- Handling cash

- Waiting for processing

That friction acted as a natural checkpoint.

With NFC:

- Transactions are instant

- Decision-making is compressed

- Awareness is reduced

This creates what we call a behavioral gap:

Users act faster than they think.

Over time, this leads to:

- Increased micro-transactions

- Reduced spending visibility

- Lower financial awareness

Why Most NFC Payment Apps Fail at Scale

Many fintech products succeed in onboarding users but struggle with long-term engagement and retention.

The reason?

They are built as transaction tools, not financial systems.

Common limitations include:

1. Lack of Behavioral Design

Apps focus on enabling payments, not guiding user decisions.

2. No Real-Time Financial Feedback

Users complete transactions but don’t understand their impact.

3. Over-Optimization for Speed

Faster is better -until it removes awareness completely.

4. Weak Personalization

Same experience for all users, regardless of spending habits.

What High-Performance NFC Payment Apps Do Differently

The next generation of NFC-based fintech apps is shifting from payment enablement → financial intelligence.

Here’s what separates high-performing products:

1. Context-Aware Transactions

Instead of just processing payments, advanced systems analyze:

- Time of transaction

- Spending category

- User behavior patterns

This allows apps to provide contextual insights, such as:

“You’ve spent 20% more this week compared to last week.”

2. Real-Time Financial Visibility

Users don’t want reports later - they need insights instantly.

High-performing apps integrate:

- Live dashboards

- Instant notifications

- Spending summaries per transaction

3. Intelligent UX Layers

UX is no longer just about simplicity.

It’s about decision support.

Examples include:

- Soft spending alerts

- Budget-based nudges

- Smart reminders before high-value transactions

4. Security + Trust Engineering

Beyond encryption, trust is built through:

- Transparent transaction logs

- Fraud detection alerts

- User control over payment permissions

Technical Architecture Behind Scalable NFC Payment Apps

To build a high-performance NFC payment system, the architecture must support:

Core Components:

- NFC interface layer (HCE / Secure Element)

- Payment gateway integration (Stripe, Razorpay, Adyen)

- Tokenization engine

- Authentication module (OAuth + biometrics)

- Backend microservices (Node.js / Java / Go)

Infrastructure:

- Cloud-based architecture (AWS / GCP / Azure)

- Real-time data pipelines (Kafka / PubSub)

- Scalable APIs (REST / GraphQL)

Compliance:

- PCI-DSS

- GDPR / data privacy

- Banking regulations

Without this foundation, scaling becomes difficult.

Where the Real Opportunity Lies

The future of NFC payments is not just about faster transactions.

It’s about intelligent financial ecosystems.

Businesses that succeed will:

- Design for behavior, not just functionality

- Combine speed with financial awareness

- Build trust through transparency

This is where most generic apps fail - and where well-designed systems win.

If you’re planning to build or scale an NFC payment solution, focusing only on features is not enough.

- The real challenge is designing a system that is fast, secure, and behavior-aware.

We’ve explored this in detail - from architecture to real-world implementation strategies - including how modern fintech apps are built for scale and user trust.

Final Thought

NFC payments didn’t just make transactions faster - they fundamentally changed how people experience spending. What once required a conscious decision is now reduced to a seamless tap, removing the natural pause that helped users stay aware of their financial choices. This shift may seem small, but over time, it reshapes behavior, making spending feel less intentional and more automatic.

As convenience increases, awareness often decreases. Users are no longer actively deciding - they are simply reacting within a frictionless system. And when that awareness fades, so does control. This is where most NFC payment apps fall short: they focus on enabling transactions, but fail to support responsible financial behavior.

The real opportunity for fintech products is not just to process payments faster, but to design systems that balance speed with awareness. Apps that introduce visibility, context, and intelligent feedback will not only improve user experience but also build long-term trust and engagement.

The companies that understand this shift won’t just build better payment apps -

They’ll build systems that shape how people think, feel, and act around money.

But here’s the real challenge.

Most NFC payment apps today are still built for transactions, not for behavior.

If you’re exploring how to build or scale an NFC payment solution, this is the layer that actually defines success - not just how fast payments happen, but how intelligently your product supports user control.

We’ve explored this in depth - from architecture to real-world fintech implementation- including how modern NFC payment systems are designed for scale, security, and user behavior.