Fintech-Driven Financial Inclusion in Emerging Markets

Vaibhav Gupta4 min read·Just now

Vaibhav Gupta4 min read·Just now--

Imagine paying a school fee, saving for a rainy day, and getting a micro-loan — all from a low-cost phone, in minutes. That’s the everyday reality fintech is unlocking across emerging markets and it’s changing lives at scale. Before delving deeper into this topic, let’s try to understand this using a simple definition & some examples.

1) What do we understand from Financial Inclusion?

Simple definition: Financial inclusion means everyone can access and use affordable, appropriate, and safe financial services, payments, savings, credit, and insurance to improve their lives and livelihoods.

Real-world examples that make it tangible:

- Mobile money wallets in Africa let market vendors accept digital payments and store value safely, reducing cash risk and enabling micro-savings. In 2023, mobile money processed $1.4 trillion globally; 2024 estimates point even higher

- Instant payment rails such as UPI (India) or Pix (Brazil) make peer-to-peer and merchant payments free or near-free, boosting digital commerce and inclusion. UPI crossed 15B transactions/month by late 2024.

- Neobanks (e.g., Nubank in Brazil) onboard underserved consumers with intuitive apps, micro-credit lines, and fee-lite accounts. Nubank surpassed 100M customers and became many Brazilians’ “main bank,” shifting inclusion and competition.

FACT- The Global Findex 2025 shows 79% of adults globally now have an account, with mobile phone access transforming usage patterns; yet usage and resilience gaps remain.

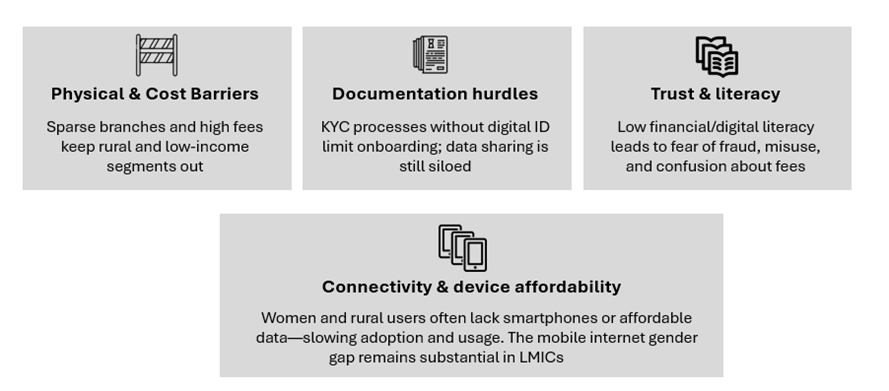

2) Why Financial Exclusion Persists, what are the major barriers to it?

Despite economic progress across the globe, exclusion sticks due to:

The trendlines shown below shows historical data from India which highlight these barriers:

The trendlines shown below shows historical data from India which highlight these barriers:

- Youth account ownership has grown steadily, but gaps remains.

- Remittance costs for transfer are still high, showing affordability challenges

3. The Fintech revolution: How digital solution drive inclusion

a) Mobile Money & Interoperability

Mobile wallets bring safe storage, low-cost transfers, and growing use cases (merchant, remittances). Interoperability — wallets talking to each other — boosts adoption and usage.

b) Agent Models

Agent networks extend last-mile cash-in/out, KYC, and onboarding — critical where branches don’t exist. Evidence from Bangladesh shows agents materially expanding inclusion for rural communities.

c) Instant Payment Rails

UPI (India) and Pix (Brazil) demonstrate how real-time, low-cost payments catalyze usage for everyday transactions; open, interoperable QR ecosystems lower acceptance costs for MSMEs. Chart shown below gives the idea about how rapidly the digital payments (UPI) Is growing in INDIA.

d) Digital Lending (with caveats)

App-based microcredit can be a lifeline for emergencies and micro-enterprise — but needs guardrails to prevent debt traps. Kenya’s DCP Regulations (2022) began addressing data protection, pricing, and collections.

e) Neobanks & Super-apps

Designing for underserved segments (low limits, simplified UX, debt relief tools) increases inclusion and sustainable profitability (e.g., Nubank’s ROE >30% in 2024).

4) Tangible Impacts — Stories & Data

- SSA’s mobile money scale: Registered accounts hit 1.75B, processing $2.7M a minute; merchant payments grew 14% to ~$74B (2023). This is more than “money transfer” — it’s commerce, savings, and credit rails for the informal economy

- Kenya’s leap: Inclusion jumped from ~27% (2006) to >80% (2021) with M-PESA, agency banking, and digital credit (though risks must be managed)

- India’s DPI flywheel: Aadhaar (ID), Jan Dhan (accounts), and UPI (payments) together lifted usage; RBI’s FI Index reached 67.0 in Mar 2025, reflecting gains across access, usage, and quality

- LATAM inclusion surge: Account ownership jumped from 55% (2017) to 74% (2021); with progressive regulation and open finance, several countries now surpass 80%

5) What’s Next- Emerging Trends Powering Inclusion

a) Open Finance (beyond banking)

High-level guidelines (IMF/UNSGSA/World Bank) emphasize secure data-sharing with consumer consent to expand access to savings, insurance, and MSME credit — especially for women-owned businesses

b) Real-Time Payments & Interoperable QR

Account-to-account (A2A) systems are scaling globally; instant rails + tokenization will transform cross-border remittances and merchant acceptance for nano-MSMEs.

c) Neobank scale & inclusive product design

Nubank shows inclusive UX and micro-credit limits can grow profitably while serving low-income segments; debt renegotiation and payroll loans aim at financial health, not just access.

d) CBDCs & cross-border interoperability

91% of surveyed central banks are exploring CBDCs; pilots focus on payment efficiency and inclusion — especially for remittances and offline access. Work is advancing in tandem with stablecoin regulation

6) Conclusion: Inclusion Is Moving from “Access” to Financial Health

Fintech has proven that access can scale; the next frontier is financial health — helping people and MSMEs use services confidently, build resilience, and grow. If we combine instant rails, open finance, agent-assisted design, and responsible credit, we can convert billions of micro-transactions into durable prosperity. Let’s build that flywheel — together

References-

The State of the Industry Report on Mobile Money 2024 | Publication | FinDev Gateway

The impact of mobile money interoperability on financial inclusion

The organisation of digital payments in India — lessons from the Unified Payments Interface (UPI)

Challenges & Risks in Digital Lending in Nigeria — Vendor Credit