Part 1 argued ESG didn’t fail by accident we made it that way. Abstraction over accountability. Scores that measured everything except what mattered. Part 2 mapped what a functioning sustainable finance ecosystem actually requires: stacked targets, interoperable taxonomies, labelled instruments tied to outcomes, portfolios held to account. Both articles were conceptual. A diagnosis and a blueprint. This one applies them.

I started writing this piece as a thought experiment. What would happen if the sustainable finance ecosystem we described in Part 2 actually got stress-tested not by a scenario model, but by a real shock? Then the Strait of Hormuz closed, and the thought experiment became unnecessary.

The Strait has been effectively shut since early March. Brent crude hit $128 in early April. The IEA has called it the largest supply disruption in the history of the global oil market [1]. The IMF’s Spring Meetings this week carry a mood as dark as anyone there can remember, with Kristalina Georgieva noting that high global anxiety tends to boost attendance. This year it hit a record [2].

It would be easy to write this article about the energy crisis, the widening EM spreads, currency sell-offs and the IMF scrambling to stand up a dozen new country programmes. That story matters, and it is unfolding in real time.

But it is not the story I want to tell.

The more important story and the one this series has been building toward is what the crisis reveals about the countries that prepared and what it suggests about the path available to those that still can. Because sustainable finance, done properly, was never an abstraction. It was always a description of what long-term fiscal resilience can look like.

The link we have been building to

In Part 1, I argued that ESG failed because it optimised for scores rather than substance with backward-looking metrics, income-biased proxies, no real linkage to credit fundamentals. In Part 2, I mapped the ecosystem needed to fix that: national targets cascading into fiscal frameworks, taxonomies that work across borders, instruments tied to verifiable outcomes.

The implicit claim across both pieces was that these were not “nice to have” sustainability features bolted onto sovereign debt management. They were a part of sovereign debt management where good governance, credible transition plans, and honest fiscal architecture are what determine whether a country retains market access through a shock or loses it.

That claim is no longer implicit. The Hormuz crisis is making it explicit, in live market data.

The countries that built credible transition frameworks and reduced structural energy import dependency are absorbing this shock measurably better than those that relied on cheap fossil imports and deferred the transition. Poland’s rapid renewable capacity build-out from 4GW of solar in 2020 to nearly 25GW by end-2025, now exceeding 50% of total power capacity is positioning it to structurally reduce energy import exposure over the medium term, even as coal still dominates current generation. Chile’s sustainability-linked bonds tied to specific, independently verified emissions and renewable targets brought a diversified investor base now providing relative pricing stability amid broad EM volatility. Demand for Chile’s recent placement exceeded 15 billion euros [3].

Meanwhile, Indonesia budgeted $22.5 billion for fuel subsidies this year based on crude staying around $70. It is now above $100. Southeast Asia produces roughly 2 million barrels of oil per day and needs 5 million [4]. That dependency is a structural challenge, not cyclical. And the fiscal cost of maintaining it through subsidies is crowding out exactly the investment that would reduce it.

This asymmetry is not random. It maps directly onto the sustainable finance ecosystem we described.

Decarbonisation as fiscal strategy

Here is where the conversation needs to shift and particularly for longer-term investment from crisis response to structural opportunity.

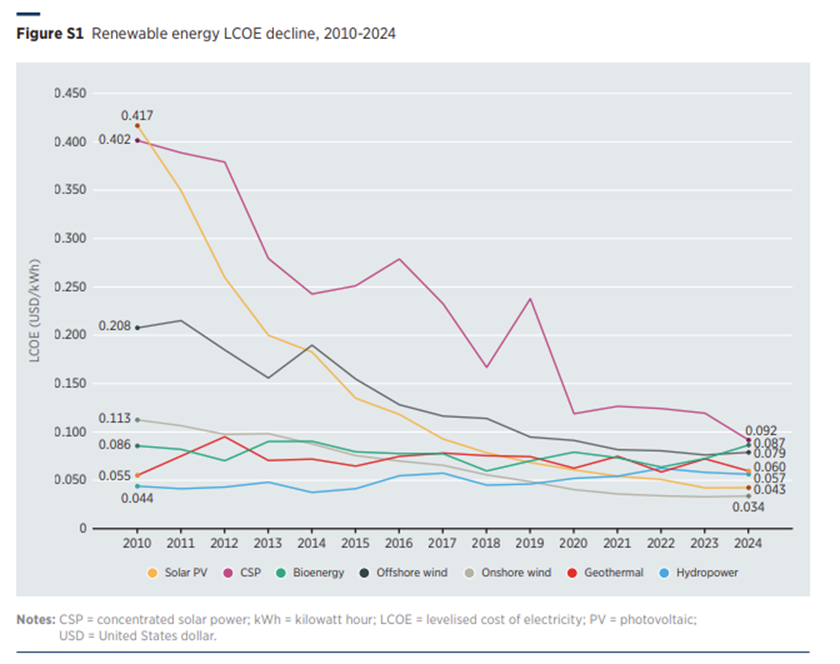

The economics of decarbonisation have changed faster than most fiscal frameworks have absorbed. IRENA’s 2025 data is striking: 91% of all new utility-scale renewable projects now produce electricity at lower cost than the cheapest fossil fuel alternative. Solar is 41% cheaper on average. Onshore wind, 53%. Existing renewables avoided $467 billion in fossil fuel costs in 2024 alone [5].

For energy-importing countries, this is not an environmental aspiration. It is the low-cost path to macroeconomic stability. Academic research confirms what practitioners already sense: renewable energy deployment in emerging economies measurably reduces energy import dependency [6]. That reduction flows directly into stronger current accounts, more stable currencies, lower imported inflation, and ultimately more fiscal space for development.

The Rockefeller Foundation made the point sharply in March: previous oil shocks failed to produce lasting structural change because they lacked at least one of three conditions; affordable alternatives, credible market incentives, or access to finance at scale. For the first time, all three are now in place [7]. Solar costs have collapsed. The EU’s Carbon Border Adjustment Mechanism, fully in force since January 2026, alongside others, imposes real costs on carbon-intensive production. And labelled bond markets have crossed $6 trillion cumulatively.

The question is no longer whether the transition is economically rational. It is whether governments will embed it in fiscal architecture before the next shock arrives.

What governments can do

This is where Parts 1 and 2 become operational.

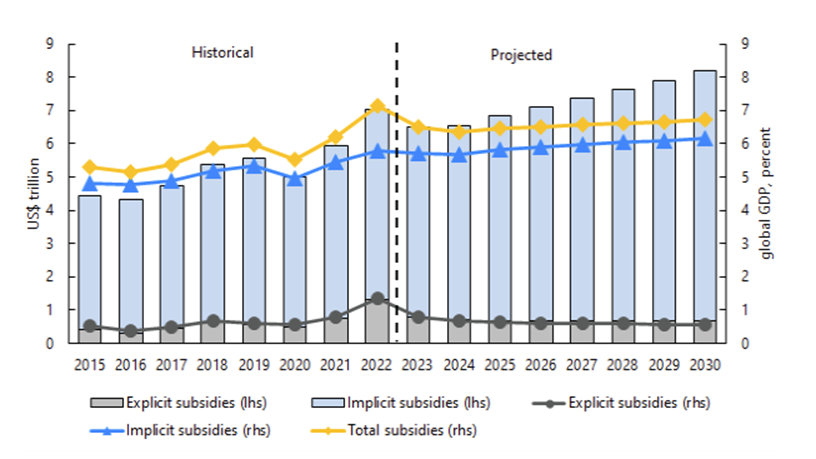

Reform subsidies, redirect the savings. The IMF’s own data shows that removing explicit fossil fuel subsidies would reduce CO₂ emissions by 6%, avoid 70,000 premature deaths annually, and raise 0.6% of GDP in government revenue [8]. Full price reform across 121 emerging and developing economies would generate roughly $3 trillion which is broadly in line with their additional spending needs for the UN Sustainable Development Goals. That is not a rounding error. It is the transition budget, hiding in plain sight inside the subsidy line.

Rodrigo Valdes was blunt at the Spring Meetings: broad-based energy subsidies distort price signals, are regressive, hard to unwind, and create international spillovers [2]. He is right. But the political economy is brutal when you try explaining carbon pricing to a finance minister whose population cannot afford to cook. The answer is not to avoid reform but to sequence it credibly: targeted cash transfers to protect the vulnerable, paired with visible investment in the domestic energy infrastructure that will lower costs permanently.

Make transition plans investable. Part 2 argued that NDCs and transition commitments only become real when they cascade into fiscal frameworks, budgets, and issuance strategies. Recent research reinforces this: the fine print of an NDC and how governments plan to fund their commitments matters as much to sovereign bondholders as the headline emissions target [9]. A credible plan with a financing pathway compresses spreads. A pledge without market plumbing does not.

The ASCOR framework, now covering 70 countries, gives investors a transparent tool to assess exactly this including whether sovereign climate commitments translate into policy, institutions, and capital allocation, or whether they remain performative [10]. This is the kind of infrastructure that makes Part 2’s stacked targets operational. And it exposes, clearly, which governments have done the work and which are still relying on labels.

Issue credibly — whether labelled or not. Chile’s experience shows that sustainability-linked bonds can genuinely expand fiscal space when the targets are material, the verification is independent, and the broader policy framework is coherent. But the instrument is not the point. The point is credibility. A conventional bond issued by a government with a genuine transition framework, transparent fiscal architecture, and credible NDC will price better than a “green” bond from a government that has none of those things. Markets price systems, not labels. That was Part 1’s central argument, and this crisis is confirming it daily.

The Anthropocene Fixed Income Institute’s work on sovereign transition linkers which includes a framework being developed for Mexico points toward what comes next: instruments that connect directly to transition milestones, not just use-of-proceeds buckets [11]. Mexico’s adoption of IFRS S1 and S2 for listed issuers this year creates the disclosure backbone such instruments need.

The models need fixing too

There is a deeper problem underneath all of this, and it is worth naming honestly.

The models governments use to assess fiscal risk are systematically understating climate and transition exposure. A February 2026 report from the University of Exeter and Carbon Tracker which draws on expert judgement from more than 60 climate scientists and found that economic models used by governments, central banks, and investors fail to capture extreme events, compounding shocks, and the cascading failures that actually reshape economies. They call it a “faulty radar” [12].

I have seen the desk-level version of this across my career. You model a 2-standard-deviation move. The market delivers a 5 to 15-standard-deviation event. The event wasn’t an obscurity, it was that your risk framework was built for the wrong distribution. Now scale that to sovereign fiscal frameworks that determine borrowing capacity for entire nations.

Lee Buchheit, who has spent four decades restructuring sovereign debt and advising finance ministers through crises exactly like this one, frames the stakes in terms that every bondholder should hear. Fiscal space, he argues, is not an abstract policy metric. It is the capacity a government has to borrow, at a reasonable rate, to deal with a crisis it has not yet imagined. And when a country accumulates debt to the point where that capacity is exhausted, it has not merely created a fiscal problem for itself it has trespassed upon the fiscal space of the next generation. He calls it an intergenerational sin [15].

That framing matters here because it connects the debt sustainability debate directly to the transition investment debate. Every dollar of fiscal space consumed by fossil fuel subsidies or crisis-driven borrowing at punitive rates is a dollar unavailable for the infrastructure that would have prevented the crisis in the first place. The sin is not just borrowing it is borrowing without building.

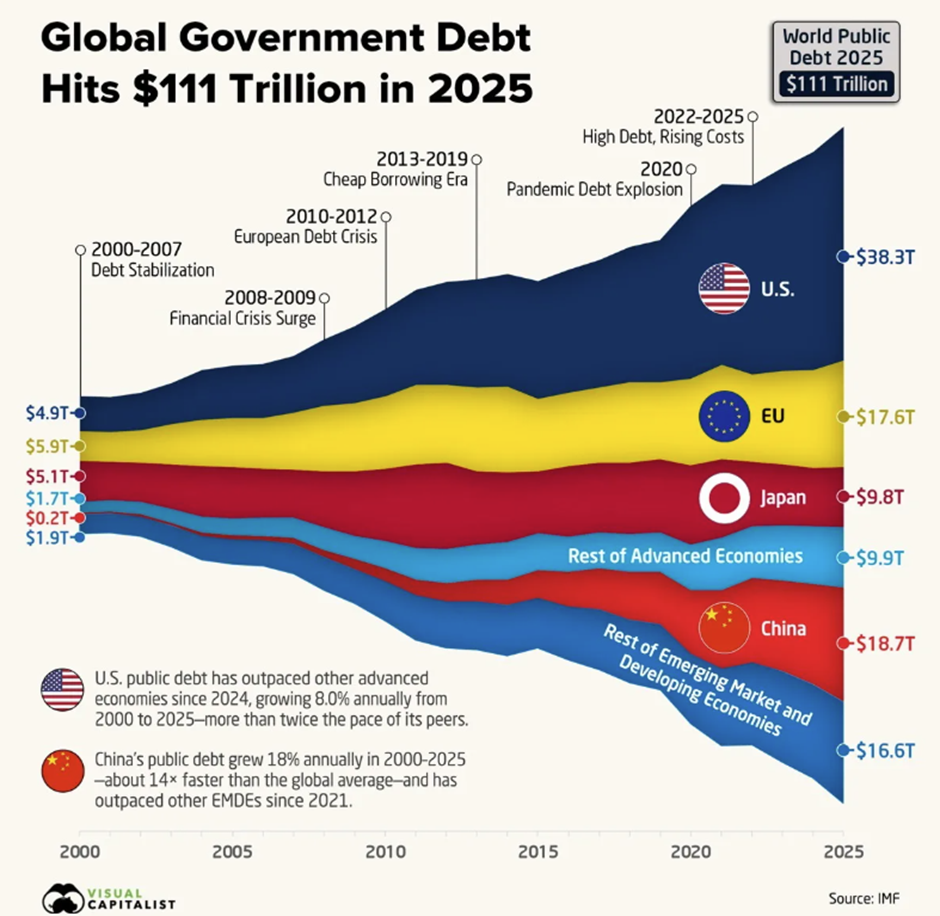

And this is not just an emerging market problem. It is tempting to read this article as being about Indonesia or Nigeria, but the fiscal space question applies with equal force to the countries whose bond markets set the global risk-free rate. The US deficit ran at 5.9% of GDP in 2025 and the CBO projects 5.8% for 2026 which is well above the 50-year average of 3.8% and with general government debt now at 121% of GDP [16]. The UK’s deficit stands at roughly 3.6% of GDP, with the OBR forecasting gradual reduction but against a backdrop of rising defence spending and an ageing population [17]. Global public debt is projected to exceed 100% of GDP by 2029, a level not seen since 1948 [18].

DM sovereign investors have long worried about this trajectory. What this crisis clarifies is that the deficit conversation and the transition conversation are the same conversation. Countries that use fiscal space to build energy independence and productive low-carbon infrastructure are investing in the resilience that protects future borrowing capacity. Countries that use it to maintain subsidies, defer structural reform, and roll over debt on the assumption that markets will always refinance, developed or developing and are making exactly the bet Buchheit warns against.

The IMF and World Bank are reviewing the Low-Income Country Debt Sustainability Framework, with findings expected mid-2026. IISD’s analysis makes the gap concrete: over half of country authorities surveyed are not comfortable with how climate was reflected in their most recent debt sustainability assessment [13]. The framework that determines whether 70% of low-income countries receive loans or grants is, by the admission of its own users, not capturing the risk that matters most.

If we are serious about fiscal space and about the sustainable finance ecosystem described in Part 2 then the analytical infrastructure has to catch up.

The architecture is the resilience

This is where the series arrives.

Part 1 diagnosed why ESG failed: we built it for marketing, not for measurement. Part 2 mapped the fix: stacked targets, interoperable taxonomies, credible instruments, portfolios held to account. This piece argues that the fix is not optional. It is what macroeconomic resilience looks like and not as an overlay, but as financial architecture.

Decarbonisation is not a luxury that countries pursue once they have fiscal space. It is how they create fiscal space. Lower energy import dependency, more stable current accounts, reduced subsidy burdens, diversified investor bases, compressed borrowing costs. The transmission mechanism runs in both directions and the countries that understood this before the Strait of Hormuz closed are proving it now.

The IMF’s Global Financial Stability Report, published this week, documents another dimension of the challenge: 80% of the $4 trillion in portfolio flows to emerging markets now comes from nonbanks through investment funds, hedge funds, pension funds up from 40% two decades ago [14]. That capital is structurally more volatile, more sensitive to global risk, more prone to synchronised exits. The cycle this creates is familiar to anyone who has watched sovereign debt markets over multiple decades: a gorging on cheap debt when markets are flush, followed by a painful purging through restructuring, followed by another gorging. The pattern is as old as sovereign lending itself, but the speed and scale of nonbank capital has compressed the cycle. When a shock hits, the capital that was supposed to fund the transition can reverse faster than governments can respond.

Which makes the architecture even more important. Credible fiscal frameworks, genuine transition plans, and honest instruments do not just lower borrowing costs in good times. They retain capital in bad times. They are the difference between managing a crisis and being managed by one.

Ajay Banga’s warning at the Spring Meetings sits behind all of this: 1.2 billion young people in developing countries will reach working age in the next 10 to 15 years, while only 420 million jobs are expected to be created [2]. That gap cannot be addressed without stable, long-duration investment in productive, low-carbon infrastructure. And that investment cannot happen without the ecosystem this series has described.

The honest conclusion, uncomfortable as it mirrors Part 1, is that the system still is not ready. Not because the ambition is missing, but because we have not finished building the plumbing. The difference now is that we can see through live market data, in every widening spread and every subsidy blowout exactly what the cost of that incompleteness is.

And exactly what the reward would be for finishing the job.

[1] IEA Oil Market Report, April 2026 [2] IMF, “Cushioning the Middle East War Shock,” Spring Meetings Curtain Raiser, April 2026; Atlantic Council Spring Meetings Coverage; Ajay Banga on the World Bank Group’s Jobs Agenda, Atlantic Council [3] Chile Ministry of Finance, Sustainability-Linked Bond Framework & 2026 Placement; Green Finance LAC Coverage [4] Carnegie Endowment, “Southeast Asia’s Agency Amid the New Oil Crisis,” April 2026 [5] IRENA, “Renewable Power Generation Costs in 2024,” July 2025 [6] Sohag et al., “Does renewable energy development reduce energy import dependency in emerging economies?” Energy Economics, 2024 [7] Rockefeller Foundation, “Another Energy Crisis Is Here. This Time, the Way Out Is Different,” March 2026 [8] IMF, “Underpriced and Overused: Fossil Fuel Subsidies Data 2025 Update,” December 2025 [9] LSE Impact Blog, “What Makes National Climate Action Investable?” November 2025 [10] ASCOR Project, Transition Pathway Initiative Centre, LSE [11] Anthropocene Fixed Income Institute, “Mexico Transition Linker,” 2026 [12] University of Exeter & Carbon Tracker, “Recalibrating Climate Risk,” February 2026 [13] IISD, “The IMF and World Bank Are Reforming Their Main Debt Sustainability Assessment Tool,” 2026 [14] IMF Global Financial Stability Report, Chapter 2, April 2026 [15] Lee Buchheit, Library of Mistakes event, Edinburgh, 2025 [16] CBO, “The Budget and Economic Outlook: 2026 to 2036,” February 2026 [17] OBR, Economic and Fiscal Outlook, March 2026 [18] IMF, “Global Debt Remains Above 235% of World GDP,” September 2025

ESG Was Always About Resilience. The Sovereign Bond Market Just Proved It. was originally published in DataDrivenInvestor on Medium, where people are continuing the conversation by highlighting and responding to this story.