Why housing is shaped — by the system, not by people — to stay just out of reach.

I thought I understood how buying a house works. Earn well. Save consistently. Upgrade when ready. Simple.

Then I opened a few listings in a major Indian metro. ₹1.2 crore. ₹1.6 crore. ₹2.2 crore. And something didn’t make sense. Because technically, it was affordable. But practically, it didn’t feel that way at all.

The Illusion of Affordability

That’s the strange part about housing today. It doesn’t feel impossible; it feels just possible enough to pull you in.

Across global markets, homes typically cost 4–6 times annual income. In Indian Tier-1 metros, that ratio often stretches to 10x or 12x. On paper, a well-earning household looks at a ₹1.5 crore home, and the math seemingly works. But real life is lived in the margins.

What the Math Doesn’t Show You

Let’s look at the mechanics of a typical urban purchase:

- The Home: ₹1.5 crore

- The Loan: ₹1.2 crore (after a ₹30 lakh down payment)

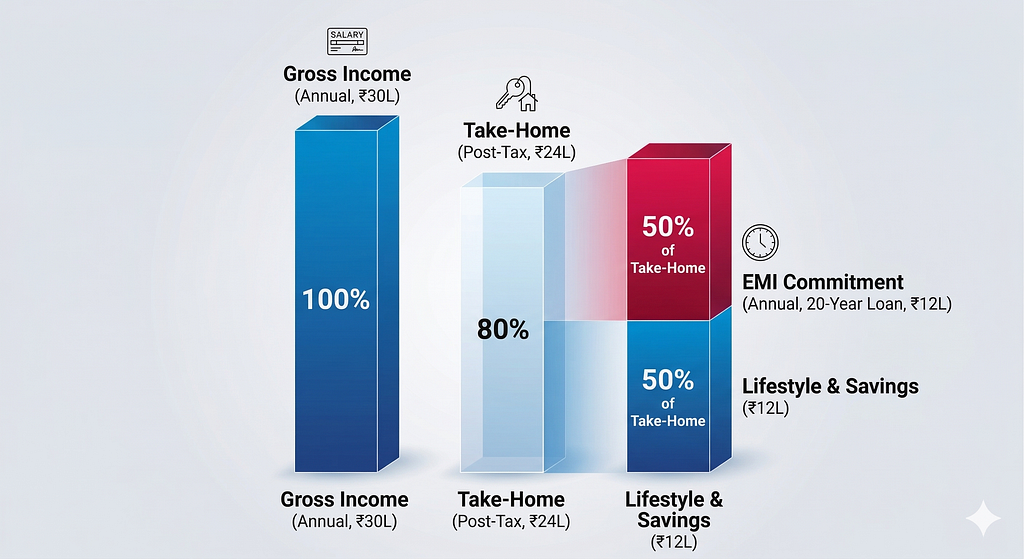

- The Commitment: ~₹1 lakh/month (at 8.5% for 20 years)

On an annual income of ₹30 lakh, a ₹12 lakh EMI looks like 40% of your earnings. But that’s before the taxman takes his share. After taxes, your actual take-home is closer to ₹23–24 lakh.

In reality, you aren’t committing 40% of your income; you are committing 50–60% of your actual liquid life. This isn’t just affordability. This is compression.

“The system doesn’t want housing to be impossible; it wants it to be just possible enough to ensure a 20-year commitment.”

The Global Bid: Why Local Income Is No Longer the Anchor

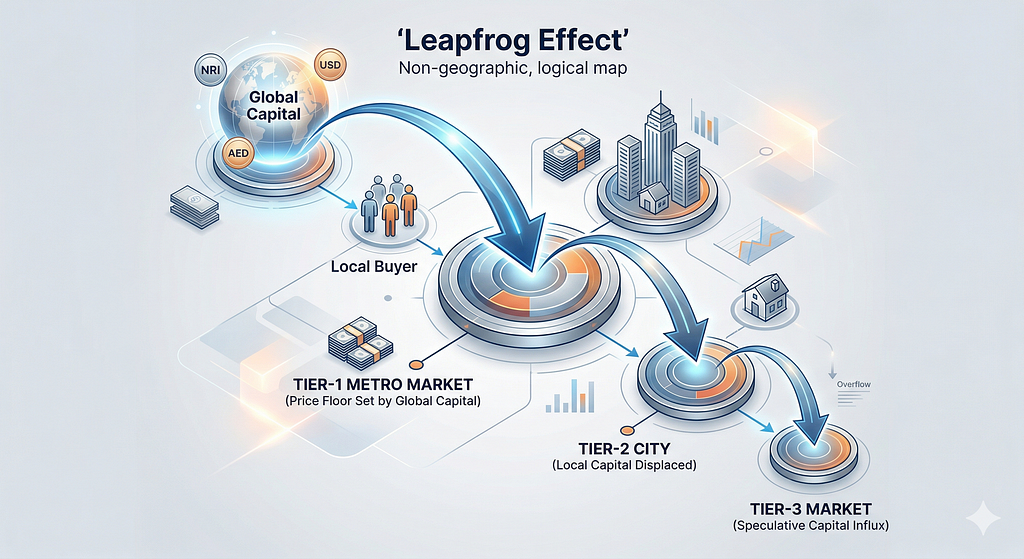

We often assume we are bidding against the couple next door. In reality, a house in a major Indian city has become an International Asset Class.

Recent data from early 2026 shows that the share of NRIs in Indian property purchases has climbed to 18–20% — nearly double what it was a decade ago. In the luxury and “ultra-prime” segments, that number jumps to 25–30%.

For a global professional earning in USD or AED, a premium Indian apartment is a Currency Play. They aren’t buying based on a local salary; they are buying with Global Capital. This creates a Leapfrog Effect that ripples through the economy:

- Tier-1 Displacement: Global capital sets a high price floor in the Metros. Local high-earners, priced out of their own city’s “prime” zones, move their capital “down” into Tier-2 cities.

- The Chain Reaction: Buyers in Tier-2, seeing prices surge from this Tier-1 influx — some by over 70% in five years — move their capital into Tier-3 towns.

- The Overflow: Money moves downward through the tiers, but the price pressure moves upward everywhere.

The price of a home in a smaller city is no longer driven by its local job market, but by the “overflow” of capital from a city hundreds of miles away. Capital is always more mobile than a local paycheck.

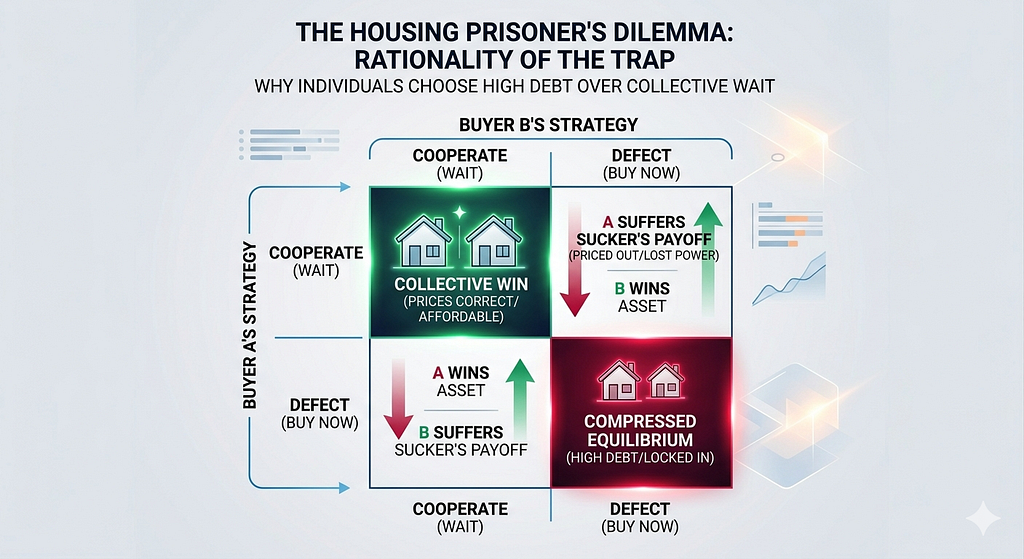

The Prisoner’s Dilemma: Why the “Trap” is Rational

If we look at this through the lens of Game Theory, we can see why individuals continue to buy even when the math is skewed. This is a classic Prisoner’s Dilemma, where rational actors make a choice that is sub-optimal for the group but necessary for the individual.

Imagine you are one of those actors. You have two choices: Buy Now or Wait.

If everyone “Cooperated” and waited, the lack of demand would force prices down. That is the collective win. But in a market with thousands of invisible competitors, you cannot coordinate. This creates the Sucker’s Payoff. If you wait for a “correction” that never comes while everyone else buys, you are left with the catastrophic risk of being permanently excluded from the market.

The market settles into a Nash Equilibrium. No buyer can improve their situation by changing their strategy alone. Even if you know the house is overpriced, your most “rational” move is still to buy — simply to protect yourself from being left behind.

The Three Essentials — and the One That Stretches

We grow up with the mantra: Roti, kapda, makaan. Food, clothing, shelter.

Food is protected because it is a survival baseline. Clothing is accessible because it scales with technology. But housing? Housing is where the pressure is allowed to build. It is the one essential that absorbs demand, aspiration, credit, and investment all at once.

While food and clothing have been commoditized, housing has been successfully financialized.

This Isn’t a Bug. It’s a Calibration.

It’s easy to think the market is “broken.” But from a systemic perspective, what if it’s working perfectly? Think about the outcomes:

- Banks secure 20 years of predictable, low-risk interest.

- Sellers capture maximum value from global and local competition.

- The Workforce becomes stable. The moment you take a loan, your risk appetite drops. You stay in the job. You keep earning.

Housing isn’t becoming “too expensive.” It is becoming perfectly calibrated. Not too expensive to stop you from signing the papers, but not cheap enough to ever truly free you.

“Housing is the most efficient labor-productivity tool ever designed. It ensures you won’t quit the job you hate because the 1st of the month is always coming.”

Maybe Nothing Is Broken

We often view high housing prices as a problem that needs “fixing.” But what if this is simply the evolution of the modern economy?

What if the “Makaan” of the 21st century is doing exactly what the system needs it to do: keeping us earning, planning, and committing our future income decades in advance?

It’s not by design. It’s by evolution. The market hasn’t failed; it has found the exact price point that keeps the gears turning.

Note on AI usage: This article was researched and written with the assistance of AI for data structuring and tonal refinement.

You Can Almost Afford a House. That’s the Problem. was originally published in DataDrivenInvestor on Medium, where people are continuing the conversation by highlighting and responding to this story.