Why Did Big Tech Suddenly Go Nuclear? The Answer Is in a 31-Million-Pound Annual Deficit

Capital Street Fx8 min read·Just now

Capital Street Fx8 min read·Just now--

Microsoft Just Restarted Three Mile Island. Meta Wants 7.8 Gigawatts of Nuclear Power. And the World Has a 31-Million-Pound Uranium Shortfall That’s Getting Worse Every Year.

There is a substance on this planet so energy-dense that a pellet the size of a fingertip contains more power than 17,000 cubic feet of natural gas, 1,780 pounds of coal, or 149 gallons of oil.

At the atomic level, splitting one uranium-235 nucleus releases 200 million electron volts of energy. Coal releases 4 eV per reaction. The ratio is 50 million to one. This is not engineering — it is physics.

One kilogram of uranium fuel produces the same energy as 45,000 kilograms of coal.

And right now, in 2026, the world is running short of it.

The Numbers That Tell the Story

Uranium spot price Q1 2026 peak: $101.41 per pound — a 16-year high. Current spot: $85.00 per pound, near a two-year high. Long-term contract price: $90.00 per pound — the highest since 2008, and the signal that actually matters. Annual supply deficit: 31 million pounds — and widening every year through 2040. Operating reactors globally: 440, with 63 more actively under construction. Kazakhstan — the world’s largest uranium producer at 43% of global supply — has announced a 10% production cut in 2026. Russia controls 40% of global uranium enrichment capacity. It is sanctioned.

These numbers do not resolve themselves. They compound.

Why the AI Industry Triggered a Nuclear Renaissance

The nuclear winter lasted a decade. After Fukushima in 2011, uranium prices collapsed from $73 per pound to under $18 by 2016. Germany shut all 17 of its reactors. The industry entered a prolonged underinvestment cycle. New mine development stopped. Enrichment capacity was not expanded. The supply chain atrophied.

Then four events collided between 2022 and 2026 and broke the cycle — not because the politics changed, but because the energy mathematics left no other choice.

Russia invaded Ukraine. The Inflation Reduction Act created $370 billion in clean energy incentives. ChatGPT launched what became an insatiable industrial demand for always-on electricity. And the United States banned Russian enriched uranium imports, removing 35% of American enriched uranium supply at a stroke.

The AI power problem is the most consequential new driver. A single large-scale AI model training run at GPT-4 scale consumes approximately 50 gigawatt-hours of electricity — enough to power 5,000 homes for a year. There are now hundreds of such training runs occurring simultaneously. The IEA projects global data centre electricity consumption will exceed 1,000 terawatt-hours by 2030, equivalent to adding Japan’s entire electricity consumption to global demand in eight years.

Nuclear delivers a 92% capacity factor — it generates electricity 92% of every hour of every year. Solar averages 25%. Wind averages 35%. AI data centres cannot tolerate intermittency. Battery storage at the required scale — hundreds of gigawatt-hours per large data campus — is economically unviable. Nuclear is the only clean energy source that delivers guaranteed 24/7 power at the scale AI infrastructure requires.

The tech industry reached this conclusion simultaneously and independently, and began signing contracts.

The Signed Deals — This Is Not Aspiration, These Are Contracts

Microsoft signed a 20-year power purchase agreement with Constellation Energy to restart Three Mile Island Unit 1 in Pennsylvania at 835 megawatts. The plant that became a symbol of nuclear’s failure in 1979 is now powering Microsoft’s AI infrastructure.

Google signed a contract with Kairos Power for 500 megawatts of Small Modular Reactor capacity, with the first unit targeting 2030 delivery. Google’s stated rationale: achieving 24/7 carbon-free electricity for global data infrastructure.

Meta has committed to a 7.8-gigawatt nuclear target — the single largest corporate nuclear commitment in history. Meta’s AI training and inference data centres require baseload power at a scale no other clean source can provide.

Amazon has invested $500 million in X-energy and is developing a dedicated nuclear campus in Culpeper, Virginia for AWS cloud infrastructure.

Oracle, with Larry Ellison’s direct public announcement, is designing a data campus powered by three Small Modular Reactors.

The US government has committed $80 billion in funding for new reactors under a Trump executive order to quadruple nuclear capacity by 2050 — the largest peacetime commitment to nuclear energy in American history.

The Supply Chain Problem Is Structural, Not Cyclical

Three countries supply more than 70% of the world’s uranium. One country controls 40% of the world’s enrichment capacity. And that country is Russia.

Kazakhstan at 43% of global supply is the Saudi Arabia of uranium. Kazatomprom, the state-owned national uranium company, mines through in-situ recovery — dissolving uranium underground and pumping it to the surface. Cheaper and faster than conventional mining. But entirely dependent on Russian pipeline infrastructure for export. And Kazatomprom is now intentionally cutting output by approximately 10% in 2026, exercising pricing discipline that the world’s largest, lowest-cost producer has never previously deployed.

Canada at 15% of global supply has the world’s best ore grades — Saskatchewan’s Athabasca Basin hosts deposits grading up to 9% uranium oxide, against a global average of 0.1%. But Cameco’s production at McArthur River ran 18% below prior year in 2025 due to equipment reliability issues and remote-site logistics.

Both of Namibia’s significant uranium mines — Rössing and Husab together representing approximately 11% of global supply — are Chinese-owned.

Then there is the step that most commodity analyses miss entirely: enrichment. Mining produces yellowcake. Before yellowcake can power a reactor, it must be converted to uranium hexafluoride, enriched from 0.7% to 4–5% U-235 concentration, then fabricated into ceramic fuel pellets. Russia’s Rosatom controls 40% of global enrichment capacity. The 2024 US ban on Russian enriched uranium created an immediate gap that the $2.7 billion DOE emergency investment in Centrus Energy is working to fill. Building enrichment capacity to replace Russia’s 40% share is a 5 to 10 year project minimum.

The world currently produces approximately 150 million pounds of uranium equivalent annually. Reactors require approximately 181 million pounds. The 31-million-pound deficit is covered by drawdown of secondary supplies — utility inventories, government stockpiles, reprocessed material — that are themselves finite. Those secondary supplies are running down. The deficit widens every year through 2040 as new reactor demand from China’s 28 simultaneously under-construction reactors, the 63 globally under construction, and the coming SMR fleet compounds against a supply chain that spent a decade not investing.

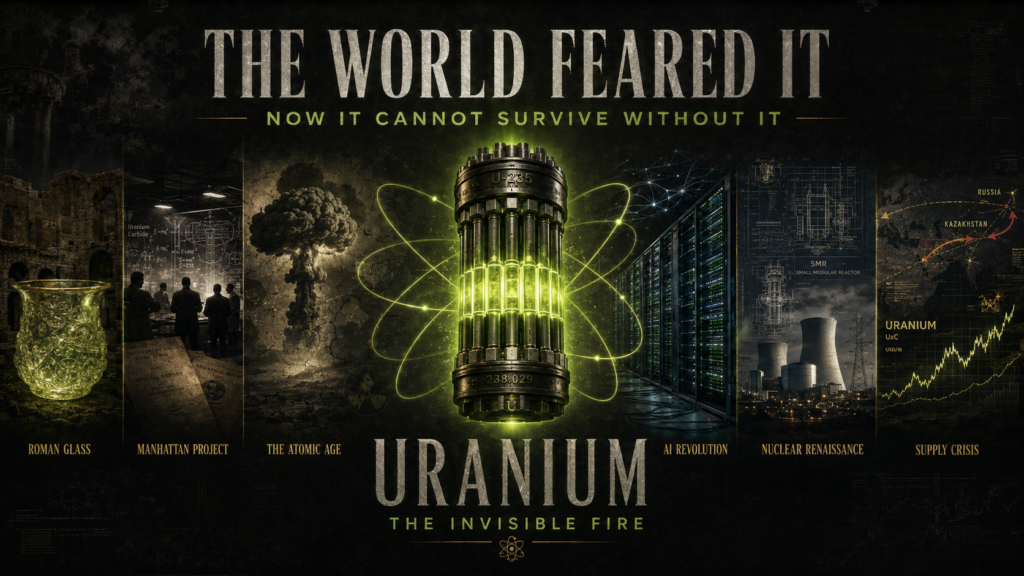

The History Context: From Roman Glass to Three Mile Island

Uranium is not a modern material. Roman glassmakers mixed uranium oxide into their furnaces to produce yellow-green glass — archaeologists found it in Pompeii. The Victorians produced uranium glass objects that glow green under ultraviolet light. Nobody knew what they were handling.

Henri Becquerel discovered radioactivity in 1896 when uranium ore left on a photographic plate in a dark drawer developed the plate without light. Marie Curie mapped the phenomenon and named it — and died in 1934 from aplastic anaemia caused by decades of radiation exposure. Her laboratory notebooks remain so radioactive they require lead-lined storage and protective clothing to access today.

Enrico Fermi achieved the first self-sustaining nuclear chain reaction beneath a squash court at the University of Chicago in 1942. No cooling system. No regulatory approval. The first commercial nuclear power station opened in 1956 — Calder Hall, switched on by Queen Elizabeth II. France made the most consequential energy decision of the 20th century: build 75% nuclear. By 1990, France had the cheapest electricity in Europe.

Then came Three Mile Island in 1979. Chernobyl in 1986. Fukushima in 2011. Three accidents in 32 years that froze Western nuclear development for a generation. Fukushima produced zero radiation deaths — but uranium prices collapsed from $73 to under $18 by 2016.

In 2024, Microsoft restarted Three Mile Island. The building that became the symbol of nuclear’s failure is now the symbol of its return.

What Moves on Uranium — The Instruments Active Traders Watch

The uranium supply story does not stay in the uranium spot market. It transmits across multiple instruments that active traders in forex and commodity CFDs follow directly.

AUD/USD — Australia holds 28% of global uranium reserves, the largest national reserve base in the world. Australian uranium miners and the broader commodity export story make AUD sensitive to uranium demand signals alongside its better-known iron ore and copper correlations.

USD/CAD — Canada produces 15% of world uranium supply. Saskatchewan’s Athabasca Basin is the world’s highest-grade uranium province. CAD correlates with the uranium cycle through Cameco — the world’s largest publicly traded uranium company — and broader Canadian resource sector sentiment.

BHP Group (LSE: BHP, £21.84) — Olympic Dam in South Australia is the world’s largest known uranium deposit. BHP produces uranium as a byproduct of copper mining at Olympic Dam and holds enormous optionality on the uranium price cycle.

Cameco Corporation (CCO on TSX) — the world’s largest pure-play uranium miner. McArthur River, the world’s richest uranium mine. The most direct equity expression of uranium spot price movements.

Energy sector indices and ETFs — uranium’s renaissance is directly intersecting with the energy transition narrative that has been driving institutional reallocation away from pure fossil fuel exposure.

The Setup

Uranium hit $101.41 in Q1 2026 — a 16-year high. It has pulled back to $85 spot, with long-term contract prices at $90, the highest since 2008. The pullback is not a reversal of the structural story. It is a pause within it.

The 31-million-pound annual deficit widens every year through 2040. Kazakhstan is cutting output. Russia’s enrichment capacity is sanctioned. China is building 28 reactors simultaneously. Microsoft, Meta, Google, Amazon, and Oracle have signed binding nuclear contracts to power AI infrastructure that cannot tolerate intermittency.

The supply crisis did not develop quickly. It was built over a decade of underinvestment that began when Fukushima scared the world away from nuclear in 2011. The consequences of that decade of underinvestment are now unavoidable, unfolding in slow motion, quantifiable in a 31-million-pound number that grows each year.

Uranium is not a trade. It is a structural realignment of where the world gets the energy it needs to run artificial intelligence at civilisational scale. The only question for traders is which instruments express that realignment most cleanly — and at what point in the cycle they are positioned.

Full analysis — including the complete 80-year uranium history, national demand programmes across 28 countries, Small Modular Reactor technology breakdown, enrichment chokepoint deep dive, and detailed trade scenarios across time horizons — is published at the Capital Street FX Research Desk: https://www.capitalstreetfx.com/daily-blog/uranium-invisible-fire-80-years-fission-fear-power/

Capital Street FX is a regulated global forex and CFD broker, licensed by FSC Mauritius and FSA SVG, operating since 2012.