Member-only story

When the Numbers Look Good But the Edge Isn’t There: A Case Study in BMY

A walk through simple backtesting, parameter sensitivity, and walk-forward validation — and what happens when all 3 tell you the same uncomfortable truth.

Kryptera13 min read·Just now

Kryptera13 min read·Just now--

The Setup

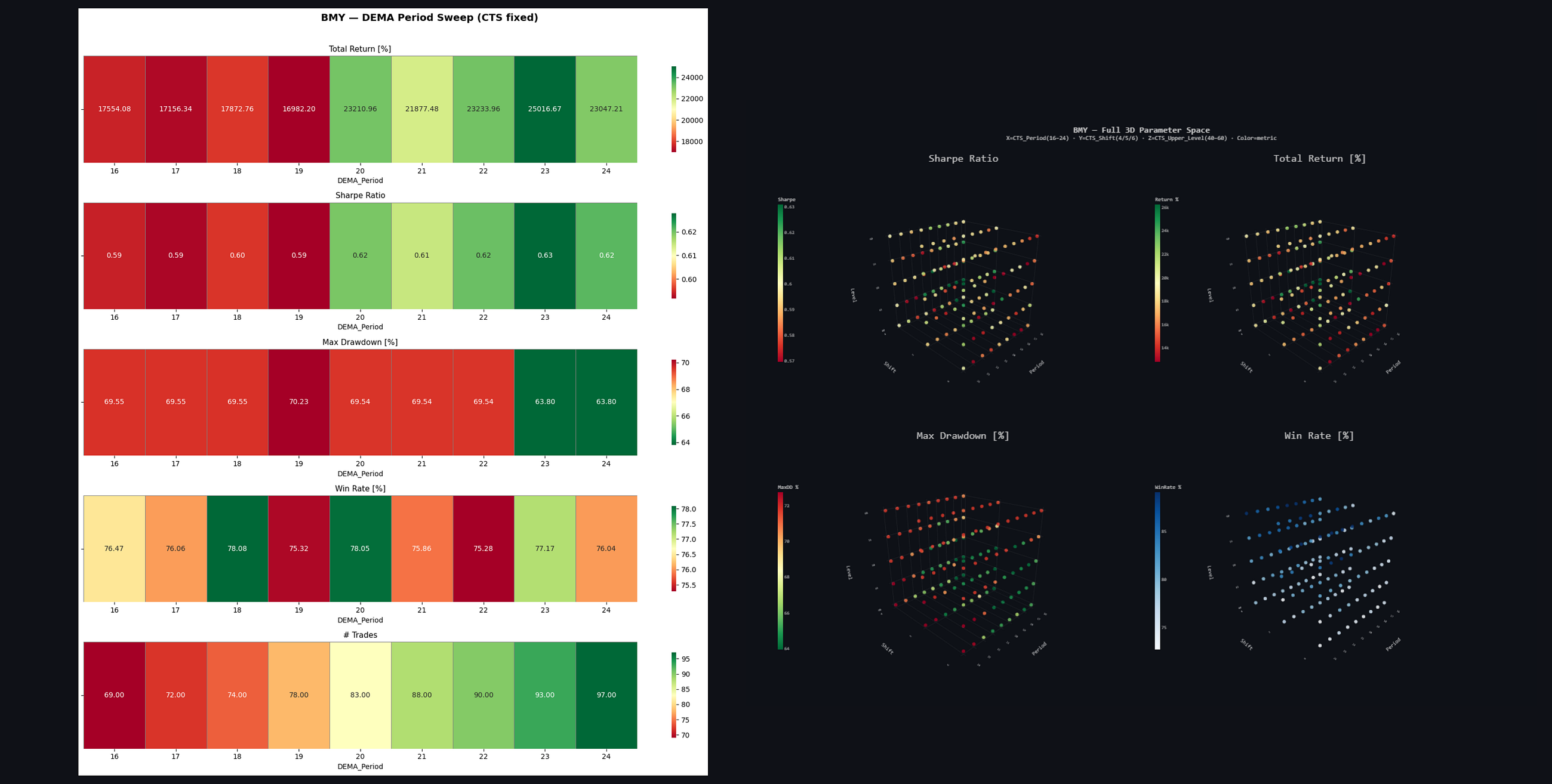

Every strategy starts with an idea. This one is straightforward: buy Bristol-Myers Squibb (BMY) when price falls below its Double Exponential Moving Average (DEMA) — a momentum-filtered trend signal — and exit when the Commodity Channel Strength (CTS) indicator crosses back below an upper threshold after being overbought. Entry on weakness, exit on exhaustion.

2 indicators. 4 parameters. Simple logic.

Entry: Close < DEMA(period)

Exit: CTS(period, shift) crosses below upper_levelThe backtest runs on daily data from 1976 to 2026 — fifty years of BMY price history. Fees at 0.1%, slippage at 0.2%. Realistic enough.

Stage 1: The Simple Backtest

import pandas as pd

import numpy as np

import yfinance as yf

import vectorbt as vbt

# -------------------------

# Download Data

# -------------------------

symbol = "BMY"

start_date = "1976-01-01"

end_date = "2030-01-01"

interval = "1d"

df =…