US credit card delinquencies hit highest level since 2011 at 13.1%

More than one in eight dollars of credit card debt is now seriously overdue, approaching the post-financial crisis peak as consumer stress intensifies.

Share

Add us on Google by Editorial Team May. 27, 2026Some 13.1% of all US credit card balances are now at least 90 days overdue. That’s the highest reading since the tail end of the last financial crisis, and it’s closing in on the 13.7% peak hit in late 2010.

The figure, drawn from New York Fed data published on May 12, represents a 0.4 percentage point jump from the previous quarter. More alarming is the trajectory: serious credit card delinquencies have climbed 5.5 percentage points since Q3 2022. That pace of deterioration actually exceeds the increase seen during the 2007-2010 period.

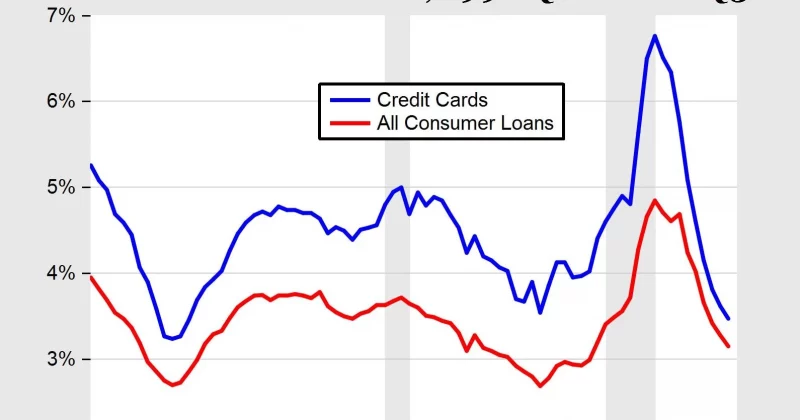

The numbers behind the stress

Total US household debt now stands at roughly $18.8 trillion, according to the same NY Fed report. Credit card balances specifically sit at approximately $1.25 trillion, which actually ticked down slightly from the prior quarter.

Balances declining while delinquencies rise tells a specific story. It suggests that consumers aren’t piling on new debt at the same rate, but the debt they already carry is becoming harder to service.

AdvertisementThe overall household delinquency rate remained relatively stable at around 4.8%. Credit cards carry far higher interest rates than mortgages or auto loans. When households come under pressure, unsecured revolving debt is typically the first thing that goes unpaid.

Transitions into serious delinquency for credit cards held steady in Q1, while early-stage delinquency transitions actually declined slightly. That mixed signal could mean the worst of the new borrowers falling behind has stabilized, but those who were already behind are sinking deeper.

Who’s getting hit hardest

The pain is concentrated in lower-income communities, which tracks with historical patterns. What’s less expected is that affluent areas are also seeing notable rises in delinquency rates. That’s a departure from the post-2008 playbook, where the crisis was overwhelmingly a story about subprime borrowers and underwater homeowners.

One curious footnote from the data: households in ZIP codes with high crypto exposure showed lower relative increases in credit card delinquencies among lower-income demographics. The implication is that digital asset holdings may have provided a modest financial cushion. The differences were marginal, and the evidence is limited.

What this means for investors

Consumer spending drives roughly two-thirds of US GDP. When more than one in eight credit card dollars is seriously delinquent, that’s not just a banking sector problem.

The last time delinquencies were this elevated, the Federal Reserve was in the middle of its post-crisis zero-rate policy. Today’s rate environment is meaningfully different, with borrowing costs substantially higher.

What is worth watching closely: whether that 13.7% post-crisis peak acts as a ceiling or a speed bump. If delinquencies breach that level in the coming quarters, it would mark the worst consumer credit environment in modern US history outside of a declared recession.

Disclosure: This article was edited by Editorial Team. For more information on how we create and review content, see our Editorial Policy.