Treasury yield gap narrows as traders bet on Federal Reserve’s higher-for-longer rates under Warsh

The 10-year minus 2-year Treasury spread compressed overnight as markets digest the hawkish implications of Kevin Warsh's first day as Fed Chair.

Share

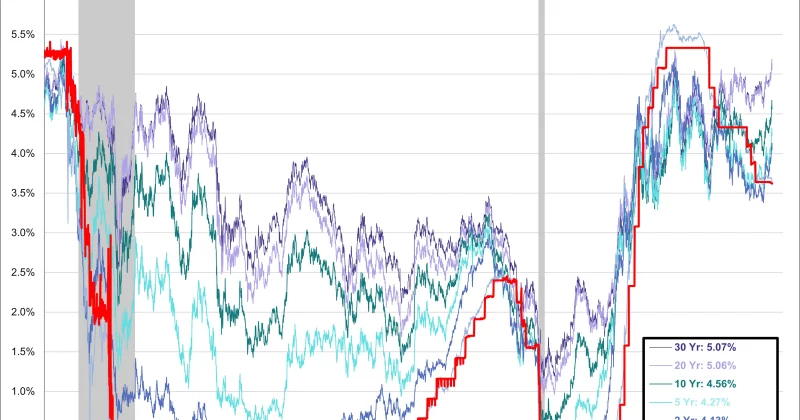

Add us on Google by Editorial Team May. 25, 2026Kevin Warsh has been on the job for less than 24 hours, and bond traders are already repricing the future. The spread between the 10-year and 2-year Treasury yields dropped from 0.49% to 0.43% on May 22, a move that, in yield-curve terms, is the equivalent of the market clearing its throat and saying “buckle up.”

The narrowing signals something specific: traders believe the Fed under Warsh will keep short-term rates elevated for longer than previously expected. When that spread compresses, it typically means markets see less room between near-term borrowing costs and long-term growth expectations.

Day one of the Warsh era

Warsh was officially sworn in as the 17th Chair of the Federal Reserve on May 22, 2026, after the FOMC unanimously selected him for the role. His Senate confirmation on May 13 was anything but unanimous, scraping through on a 54-45 vote that reflected partisan tension over his expected policy direction.

AdvertisementThis isn’t Warsh’s first tour of duty at the Fed. He served as a governor from 2006 to 2011, a period that included the worst financial crisis in a generation.

Two priorities have defined Warsh’s public positioning heading into the job. First, he wants to shrink the Fed’s balance sheet, which currently sits at approximately $6.7 trillion. Second, he’s proposed a new Treasury-Fed accord modeled after the landmark 1951 agreement that formally separated monetary policy from Treasury debt management.

What the yield curve is saying

A flattening yield curve under these circumstances suggests traders believe the Fed will hold policy rates higher even as longer-term growth expectations remain anchored. The 0.43% spread still represents a positively sloped curve, meaning long-term rates remain above short-term rates. But the direction of travel, from 0.49% to 0.43% in a single session, tells you that expectations for rate cuts are being pushed further into the future.

Persistent inflation pressures are the backdrop here. Despite multiple rounds of tightening over the past few years, inflation has proven stubbornly resistant to returning cleanly to the Fed’s 2% target, with recent CPI data showing figures near or exceeding 3%.

What this means for investors

For traditional bond portfolios, a higher-for-longer rate environment means duration risk remains a real consideration. Short-duration instruments and floating-rate exposures look more attractive in this environment.

For the crypto market specifically, Warsh’s tenure adds an unusual variable. He has a history as a crypto-linked investor with prior investments in digital asset firms. A $6.7 trillion balance sheet shrinking meaningfully would drain liquidity from financial markets across the board. Bitcoin and other digital assets have shown strong correlation with global liquidity conditions over the past several years.

Disclosure: This article was edited by Editorial Team. For more information on how we create and review content, see our Editorial Policy.