Top 10 Cross-Border Crypto Payment Solutions for Global Businesses

Blocsys Technologies Pvt. Ltd.17 min read·Just now

Blocsys Technologies Pvt. Ltd.17 min read·Just now--

More enterprise payment flows now demand near-real-time settlement, yet much of cross-border banking still depends on intermediary chains, cut-off windows, and delayed reconciliation. That operating gap is pushing digital asset payments from a specialist tool into core infrastructure for global businesses.

The shift is visible in high-volume corridors where remittance demand, trade activity, and treasury pressure intersect. For product and finance teams, the implication is strategic. Payment architecture now affects working capital efficiency, counterparty risk, compliance scope, and the user experience at checkout or payout.

The main decision is not whether crypto rails have a role in cross-border operations. It is which architecture matches your business model, jurisdictional footprint, and risk controls. A Europe-based marketplace handling multi-party payouts faces different requirements from a UAE treasury team optimizing stablecoin settlement, or from a platform that needs API-first collection, conversion, and off-ramp flows.

This guide is designed for that selection process. It goes beyond naming vendors and compares the underlying infrastructure choices that matter in practice: API maturity, stablecoin support, fiat integration, custody design, compliance controls, and the tradeoff between building in-house versus buying a managed platform. The emphasis on Europe and the UAE reflects where regulatory expectations, licensing models, and enterprise demand are developing quickly, but many market roundups still treat these regions too broadly.

The goal is to help product leaders, fintech founders, payment architects, and compliance stakeholders evaluate the leading solutions in this space.

The Inevitable Shift to Digital Asset Payments

Cross-border settlement still runs on infrastructure designed for batch processing, intermediary banks, and limited operating hours. That model is increasingly misaligned with businesses selling digital services, coordinating distributed suppliers, or managing treasury across Europe and the UAE. When receivables move instantly but settlement takes days, finance teams absorb the gap through higher cash buffers, slower fulfillment, and more reconciliation work.

Digital asset payments address that mismatch at the settlement layer. Stablecoins such as USDC and USDT give enterprises a way to transfer value on always-on networks, with fewer intermediaries between sender and recipient. For enterprise teams, the strategic question is not whether blockchain can move funds. It is whether a given payment architecture can reduce cost and delay without creating unacceptable compliance, custody, or counterparty risk.

The shift is easiest to see in corridors where remittance volumes, trade flows, and foreign exchange pressure are all high. In those markets, businesses are testing stablecoin settlement because traditional rails often introduce timing risk at the exact point where working capital is tight and payout expectations are immediate.

For product and finance leaders, the implications are broader than payment speed alone. A delayed supplier payment can interrupt inventory release. A fragmented payout stack can increase sanctions screening complexity. A poorly chosen off-ramp partner can turn a lower-fee payment flow into a treasury and audit problem six months later. Tax treatment also needs to be scoped early, especially for firms handling conversion events across jurisdictions. Teams that need to calculate crypto taxes before launch usually discover that ledger design and reporting logic should be part of infrastructure selection, not an afterthought.

Why this matters to enterprise teams

A narrow payments project often expands into an operating model decision.

- Settlement design: Teams must choose where value is held and transferred, in stablecoins, fiat, or a hybrid structure that minimizes conversion points.

- Compliance exposure: Each wallet, exchange, and banking partner changes the KYC, AML, sanctions, and transaction monitoring scope.

- Regional fit: Europe and the UAE have different licensing expectations, banking relationships, and documentation standards for payment activity.

- Operational resilience: Enterprises need fallback paths when a chain is congested, a banking partner limits flows, or a liquidity provider reprices a corridor.

The strongest enterprise platforms are built around that reality. They combine API access, stablecoin support, conversion logic, fiat payout rails, and compliance controls into one operating layer. That is the difference between a crypto feature and payment infrastructure a regulated business can practically deploy.

What Are Cross-Border Crypto Payments A Framework for Businesses

Cross-border crypto payments replace part of the international payment stack with blockchain settlement. A business sends, receives, or holds value across jurisdictions using digital assets instead of relying only on correspondent banking rails. For enterprise use, the discussion is usually about stablecoins, not volatile cryptocurrencies, because finance teams need stable invoice values, predictable settlement, and cleaner reconciliation.

The enterprise question is not whether a payment can move on-chain. It is which parts of the payment flow should move on-chain, where fiat conversion should occur, and which provider owns the compliance burden in Europe and the UAE.

The operating model has three layers

Cross-border crypto payments are best understood as an architecture decision with three interdependent layers.

- Settlement asset

Stablecoins such as USDC or USDT are the common settlement unit because they reduce mark-to-market risk between invoice creation and final receipt. The choice of asset also affects counterparty acceptance, reserve transparency, redemption options, and regulatory treatment. - Blockchain rails

The network determines confirmation time, fee volatility, finality assumptions, and wallet support. For product teams, chain choice is not just a technical preference. It changes unit economics, customer experience, and the design of controls around failed or delayed transactions. - Payment interface

APIs, treasury systems, wallets, compliance tooling, and fiat payout partners turn blockchain transfers into usable business workflows. This is the layer where invoicing, beneficiary management, approvals, transaction monitoring, and ERP sync either work cleanly or create operational drag.

Teams building this stack internally often find that wallet design becomes a major control point. The trade-offs in custodial vs non-custodial wallet architecture shape who holds funds, who signs transactions, and where regulatory responsibility sits.

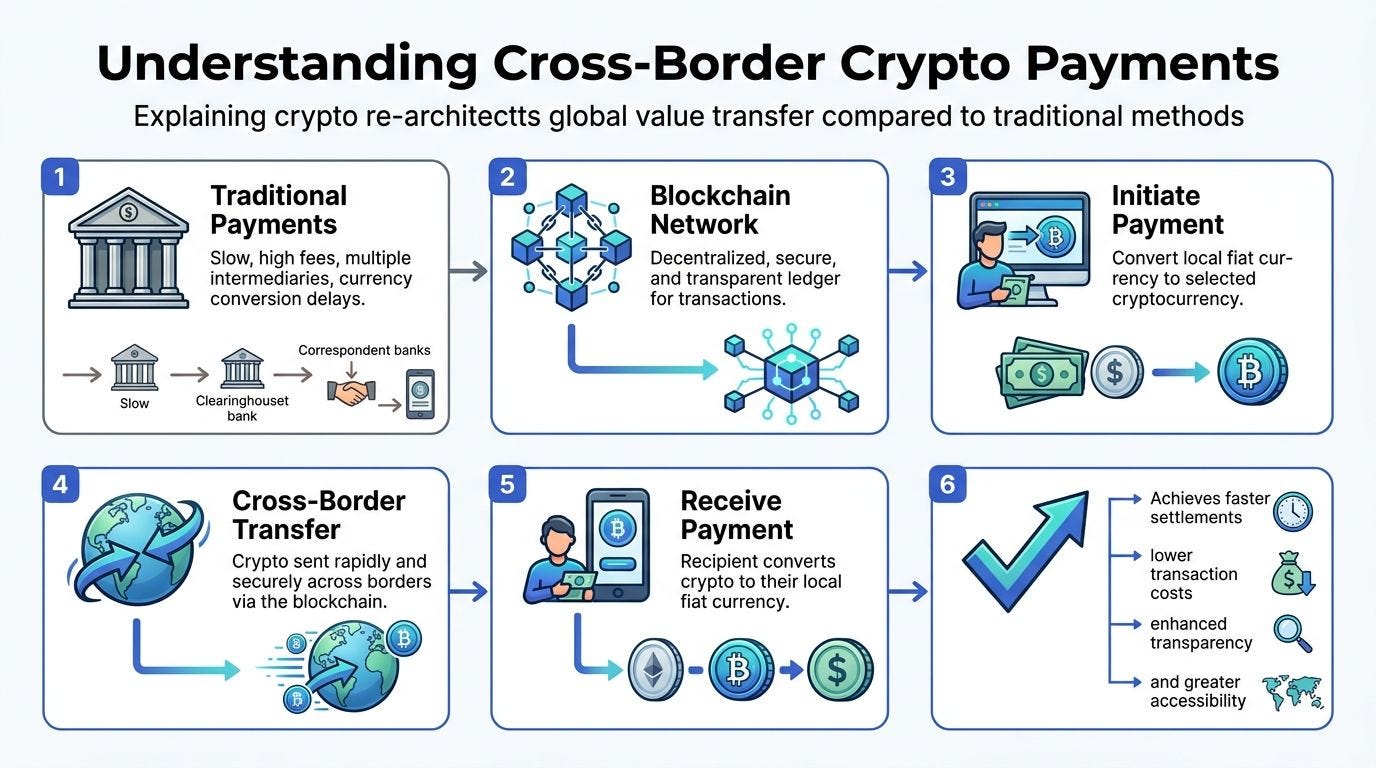

How the payment flow differs from bank-led cross-border transfers

A typical crypto-based cross-border payment has four steps:

- Funding: The payer acquires a supported digital asset, directly or through a liquidity partner.

- Transfer: Value moves across a blockchain network to the recipient or the recipient’s payment provider.

- Conversion or retention: The recipient either keeps the asset, converts it to fiat, or sweeps it into treasury.

- Reconciliation: On-chain activity is matched to invoices, counterparties, fees, and internal ledger entries.

Traditional international wires route through a chain of banks, cut-off times, nostro and vostro balances, manual compliance reviews, and corridor-specific FX processes. Crypto payment flows compress several of those layers, but they do not remove the need for controls. They shift where those controls need to exist.

That distinction has become visible in corridors where settlement speed and banking access directly affect working capital. For exporters, marketplaces, and treasury teams, the benefit is usually not the transfer itself. It is faster availability of funds, fewer intermediaries, and a narrower gap between payment initiation and usable cash.

The business impact sits in finance, compliance, and product design

Cross-border crypto payments change operating mechanics in ways that a simple vendor comparison often misses.

- Treasury efficiency: Faster settlement can reduce buffers held only to absorb bank delays and cut the number of conversion steps across entities.

- Product flexibility: Platforms can support contractor payouts, merchant settlements, or marketplace disbursements in corridors where bank coverage is weak or slow.

- Compliance design: KYC, AML, sanctions screening, travel rule handling, and transaction monitoring still apply. The difference is that these controls must be mapped across wallets, APIs, and off-ramp partners rather than only across banks.

- Regional architecture: Europe and the UAE often require different partner selection, recordkeeping, and licensing assumptions. A provider that works technically in both regions may still create compliance friction in one of them.

A useful decision framework is to ask where the firm wants to hold risk. Some businesses want an all-in-one provider that bundles wallets, conversion, and payouts. Others prefer direct wallet control, a separate liquidity layer, and their own compliance stack. That build-versus-buy decision starts here, at the definition stage, not after vendor selection.

Finance teams should also plan for tax treatment from the start. Payment flows that include conversion, custody changes, or asset reclassification can create reporting complexity across entities and jurisdictions. Teams that need to calculate crypto taxes before launch usually discover that ledger structure and reconciliation logic belong in the payment architecture, not in a later reporting patch.

Key Evaluation Criteria for Enterprise Crypto Payment Solutions

Enterprise selection should start with implementation risk, not feature count. A provider can support dozens of assets and still fail your rollout if its controls, settlement model, or API assumptions conflict with how your finance and compliance teams operate in Europe and the UAE.

Security and compliance controls

The first screening question is whether the provider reduces regulatory exposure or shifts it back to your team. Cross-border crypto payment programs tend to break at the points where custody, screening, approvals, and audit evidence intersect. That matters more than checkout UX for treasury payouts, marketplace disbursements, and B2B settlement flows.

Four control areas deserve early review:

- Custody model: Does the provider hold funds, or does your organisation control wallets and signing?

- Ongoing KYC and AML controls: Can the system support repeated checks, risk scoring, and case management after onboarding?

- Sanctions and travel rule workflows: How are exceptions escalated, reviewed, and recorded?

- Audit trail quality: Can finance, risk, and compliance teams reconstruct a payment lifecycle without manual blockchain forensics?

Custody often determines the rest of the architecture. It shapes licensing exposure, operational segregation, incident response, and how client money is handled across entities. Teams comparing providers should review the trade-offs in custodial vs non-custodial wallet architecture, especially if the product handles third-party funds or needs clear separation between treasury and customer balances.

API design and technical architecture

Enterprise product teams should assess a crypto payment API the same way they assess a banking or ERP integration. Documentation quality matters, but so do state models, idempotency, webhook delivery, retry behaviour, and the provider’s approach to chain abstraction. Weak design in any of those layers creates operational debt that surfaces later as failed payouts, duplicated events, and reconciliation effort.

The strongest platforms usually perform well across four technical dimensions:

Technical area What to verify API maturity Clear documentation, idempotency, predictable status models Chain support Stablecoin support across the networks your users and counterparties use in production Treasury tooling Conversion logic, batching, payout routing, reconciliation exports Failure handling Monitoring, alerting, retry behaviour, and exception workflows

Stablecoin support needs closer inspection than a simple asset list. Enterprise teams should ask which token standards are supported, on which chains, with what confirmation logic, and under what settlement assumptions. USDC on Ethereum, USDC on Solana, and USDC on Polygon may serve different cost, speed, and risk profiles. A provider that abstracts those differences well can shorten time to market. A provider that hides them poorly can create support and treasury issues later.

Fiat on and off ramp capability

Fiat connectivity is where many promising crypto payment stacks become hard to operate at scale. The strategic question is not whether a provider can convert funds. It is whether conversion works reliably in your target corridors, with predictable settlement timing, acceptable spreads, and records your finance team can post without manual work.

For Europe, that usually means practical EUR settlement coverage, banking partner quality, and payout consistency across SEPA-linked flows. For the UAE, the harder questions often concern AED liquidity, local payout confidence, documentation standards, and the resilience of banking relationships behind the crypto layer. Providers with similar front-end capabilities can differ materially here.

Regulatory clarity in a jurisdiction tends to improve fiat connectivity first, then accelerate product adoption. That pattern matters for enterprise planning because it affects corridor rollout order, partner selection, and whether a buy decision today will still fit your operating model in 12 months.

Cost structure and hidden operational spend

Headline fees rarely capture the actual economics of a crypto payment deployment. Procurement teams should model the full operating cost of the payment flow, including FX spread, conversion timing, prefunding requirements, fragmented liquidity, failed transaction handling, support escalation, and month-end reconciliation.

A stronger vendor review asks:

- What events trigger conversion or spread costs?

- Who controls the FX decision and settlement timing?

- How are failed payouts, refunds, and reversals processed operationally?

- Which reconciliation steps remain manual after go-live?

Low quoted fees do not help if your team still has to reconcile wallets to payout files, explain timing differences to finance, and investigate exceptions across multiple counterparties. In practice, the better enterprise choice is often the provider that reduces compliance ambiguity, shortens engineering effort, and limits back-office exceptions, even if its visible transaction fee is not the lowest.

That is the decision framework enterprise teams should use. Evaluate providers as infrastructure partners with implications for risk, reporting, and regional scale, not as simple payment widgets.

Top 10 Cross-Border Crypto Payment Solutions for Europe & UAE

Enterprise teams entering Europe and the UAE usually discover that provider selection is less about brand recognition and more about settlement design. The shortlist changes quickly once product, treasury, and compliance leads map the actual flow of funds: who receives stablecoins, where conversion occurs, which entity books revenue, and what reporting must be produced for auditors and regulators.

For that reason, this list should be read as a decision tool, not a ranking. Some vendors are strongest at checkout acceptance. Others are better suited to treasury settlement, supplier payouts, or platform-led orchestration across multiple jurisdictions. For Europe and UAE-based operations, the more useful lens is technical and compliance fit: API depth, stablecoin standards, fiat exit options, entity support, and the operational burden left with your finance team after go-live.

Crypto Payment Gateway Comparison for Europe & UAE

A procurement team should also assess how any selected vendor fits a wider Web3 regulatory compliance framework for multi-jurisdiction payment operations, especially if the business will hold customer funds, automate payouts, or serve Europe and the UAE from a shared product stack.

BitPay

BitPay remains relevant for businesses approaching crypto acceptance through a familiar merchant acquiring model. That matters in larger organisations where finance, legal, and procurement teams want a payment flow that resembles existing card processor reviews.

Its fit is strongest for standardised acceptance. It is less attractive where the product requires custom payout logic, treasury routing across entities, or tighter control over how and when conversion happens.

CoinGate

CoinGate is usually a practical option for e-commerce merchants that want crypto acceptance without building much internal payment infrastructure. Its value comes from speed of deployment and a relatively direct invoicing and checkout model.

For European businesses, that can align well with online retail and invoice-based sales. UAE-based teams should test whether local fiat settlement, treasury timing, and operational support match internal finance controls rather than assuming checkout simplicity solves the full payment problem.

CoinsPaid

CoinsPaid is more relevant where payment operations extend beyond customer checkout. It often appears on enterprise shortlists for recurring settlements, partner disbursements, and businesses with meaningful crypto-denominated inflows.

That distinction matters. A company with treasury exposure, internal wallet operations, or payout obligations needs more than a payment page. It needs clear reconciliation outputs, defined exception handling, and predictable fiat exit routes across target corridors.

Earlier market evidence in this article showed why that competition has shifted toward settlement architecture and away from pure acceptance features. Buyers should read CoinsPaid through that lens.

A short technical explainer is helpful before comparing the rest of the field.

NOWPayments

NOWPayments is frequently selected by teams that want broad token support and flexible checkout options. That can help businesses selling to crypto-native customers who hold a wide mix of assets.

The trade-off is operational complexity. More accepted assets usually mean more treasury decisions, more conversion rules, and more accounting treatment to define internally. For enterprise teams, a narrower stablecoin policy is often easier to control than broad token optionality.

Utrust xMoney

Utrust, now xMoney, is generally assessed for front-end payment experience and merchant conversion. That makes it more relevant for brands that see crypto payments as a customer-facing feature rather than a treasury rail.

European merchants may value that focus if checkout quality directly affects sales completion. Product teams building embedded financial workflows should still verify whether the platform supports the reporting, payout controls, and back-office processes required after payment acceptance.

TripleA

TripleA is regularly shortlisted by firms that place regulatory alignment high in the selection process. That tends to matter more in Europe and the UAE, where governance expectations are rising for onboarding, transaction monitoring, and reporting.

The strategic question is not whether a provider uses compliance language in its positioning. It is whether the implementation model reduces operational risk. Ask how investigations are handled, what artefacts are available for audit, and whether finance teams can reconcile settlements without manual casework.

If a provider cannot explain exception handling, investigation workflows, and reporting outputs in detail, it is not ready for enterprise deployment.

TransFi

TransFi is better understood as corridor infrastructure than as a simple checkout tool. Its appeal is stronger for businesses managing supplier payments, contractor disbursements, and cross-border platform payouts where crypto and fiat must interact within one payment flow.

In Europe and the UAE, corridor depth matters more than feature breadth. Banking partners, payout coverage, settlement timing, and conversion control usually determine whether the service can support production volume.

Binance Pay

Binance Pay can be efficient when both sides of a transaction already operate inside the Binance ecosystem. In those cases, onboarding friction may be lower and execution may be faster for ecosystem-native counterparties.

That efficiency comes with concentration risk. Enterprises should assess dependence on one exchange environment, limits on interoperability, and whether internal risk policy permits that degree of operational coupling.

Paychant

Paychant is most relevant where crypto-to-fiat conversion sits close to payment collection or payout release. That model can suit businesses that want minimal digital asset exposure and rapid movement into fiat accounts.

The diligence work should stay practical. Review funding timelines, reconciliation data, failed conversion handling, and how support is escalated when settlement breaks across borders.

Coinbase Commerce

Coinbase Commerce tends to appeal to businesses that want a familiar brand and a relatively direct route into crypto acceptance. That can support adoption where customer trust influences checkout completion.

Its fit is usually better for straightforward merchant acceptance than for complex payment infrastructure. Teams building multi-entity products, embedded wallets, or automated treasury workflows will often need additional orchestration layers beyond the core acceptance service.

Build vs Buy How to Choose Your Payment Infrastructure Path

The build-versus-buy decision usually becomes clearer once you identify where the payment system creates strategic value. If payments are a support function, buying is often rational. If payments define your margin, user workflow, or treasury edge, building part of the stack becomes more defensible.

When buying is the right answer

Buy if your core need is standardised payment acceptance, business payouts, or fiat on and off ramp access with a known integration pattern. This is often the right path for SaaS companies, e-commerce businesses, or service exporters that need to move quickly and don’t want to own custody, routing, and compliance logic internally.

The benefit isn’t only speed. It’s reduced implementation scope. Your team can focus on product and treasury policy rather than wallet security, chain monitoring, and payout orchestration.

When building creates strategic leverage

Build when payments are part of the product itself. That includes trading infrastructure, embedded settlement layers, tokenised marketplaces, treasury systems, or high-frequency payout products where generic gateway logic becomes restrictive.

Ripple’s XRP network illustrates the type of performance threshold that can justify custom design in specific flows. According to Web3 Enabler’s analysis of cross-border payment assets, XRP delivers settlement in 3 to 4 seconds with fees under $0.01, supports 1,500 TPS baseline scalability up to 65,000 TPS through payment channels, and can produce 40% to 60% cost savings over SWIFT transfers. Those characteristics matter most when your payment path is latency-sensitive or integrated into trading and treasury operations.

A simple decision lens

Decision factor Buy Build Time to market Faster Slower, but more tailored Upfront engineering load Lower Higher Control over flows Limited to vendor model High Compliance design Shared with provider Internal responsibility Product differentiation Low to moderate High where payments are core

For businesses building proprietary settlement or liquidity infrastructure, custom development often makes more sense than stitching together merchant tools. In those cases, specialised teams working on OTC trading platform development can help design payment and execution layers that fit institutional workflows rather than retail checkout logic.

The Future of Global Crypto Payments A 24-Month Outlook

The next two years won’t be defined by whether crypto payments exist. They’ll be defined by which providers can operate as regulated, programmable financial infrastructure across multiple jurisdictions.

Regulation will reward operational maturity

Europe’s regulatory direction and the UAE’s licensing posture both push the market toward better-defined payment models. That doesn’t mean every provider will converge. It means weaker operators will find it harder to hide thin controls behind broad product claims.

AI will move into transaction operations

The biggest near-term shift is likely to happen inside compliance operations rather than user interfaces. Providers will increasingly use automation to score counterparties, route exceptions, monitor transaction patterns, and support faster investigations. Teams building internal payment products should plan for this now, not treat it as a later enhancement. A useful reference point is how AI agents are changing crypto payment workflows in monitoring, routing, and operational automation.

Stablecoin routing will become more modular

The strongest platforms will combine stablecoin settlement, fiat on and off ramps, and programmable routing rather than forcing businesses into a single corridor design. BVNK is a good example of this direction. According to BVNK’s overview of enterprise crypto payment gateways, its gateway supports multi-chain stablecoin settlements across 130+ jurisdictions, processes $25B+ annually, offers 24/7 fiat on/off-ramps, and uses smart routing to reduce latency by 70% for INR-to-USD flows while supporting real-time compliance workflows.

The long-term winners won’t be the providers with the longest token lists. They’ll be the ones that make settlement, compliance, and reconciliation feel like one coherent system.

CBDCs may influence parts of the market, but private stablecoins are still better aligned with the speed of current product development. For most businesses, the strategic move now is to design payment architecture that can adapt to either path.

How Blocsys Accelerates Your Cross-Border Payment Strategy

The struggle for organizations considering crypto payments is not with the concept itself, but with implementation boundaries: which parts should sit with a vendor, which parts should remain in-house, and which parts need custom engineering because they affect treasury, compliance, or product differentiation.

That matters most for businesses building exchanges, tokenisation systems, trading venues, embedded wallets, or cross-border settlement products. In those cases, a gateway alone usually isn’t enough. The team also needs architecture for wallet flows, ledgering, compliance automation, stablecoin handling, and integration across banking and blockchain layers.

Blocsys works in that layer of the stack. The company helps fintechs, exchanges, and digital asset businesses build production-ready blockchain and AI-powered platforms, including tokenisation systems, trading infrastructure, and intelligent compliance workflows. If your team is evaluating whether to integrate third-party payment providers, build proprietary rails, or combine both models, Blocsys Technologies is one development partner operating in that implementation space.

The practical value isn’t just code delivery. It’s reducing the gap between product strategy and operational reality. A payment stack has to clear architecture review, legal review, treasury review, and launch readiness. Teams that design those workstreams together usually avoid the most expensive rebuilds later.

Frequently Asked Questions

How do businesses manage crypto price volatility for cross-border invoices

Most businesses avoid using volatile assets for invoicing unless the asset itself is part of the commercial agreement. In practice, they invoice in fiat terms and settle using stablecoins such as USDC or USDT. That keeps the payment rail digital while reducing exposure between invoice creation and settlement.

What are the best practices for securing corporate treasury funds in crypto

Start by separating operational wallets from treasury storage. Limit hot wallet balances to what the business needs for active settlement. Use role-based approvals, internal reconciliation controls, and clear signing policies. The bigger governance question is who can move funds, under what circumstances, and how exceptions are reviewed.

Are there tax reporting differences between accepting stablecoins and volatile assets

Yes, there can be. Stablecoins may simplify valuation and accounting compared with volatile assets, but they still create reporting and record-keeping obligations. Businesses should track acquisition value, settlement timing, conversions into fiat, and counterparty records in a way that matches their jurisdiction and entity structure.

If you’re building a payment product, evaluating crypto off-ramp solutions, or designing enterprise cross-border settlement infrastructure, connect with Blocsys Technologies for expert guidance on architecture, compliance workflows, and implementation strategy.