Bitcoin faces 2026's densest macro test as CPI, Warsh, and Trump-Xi collide

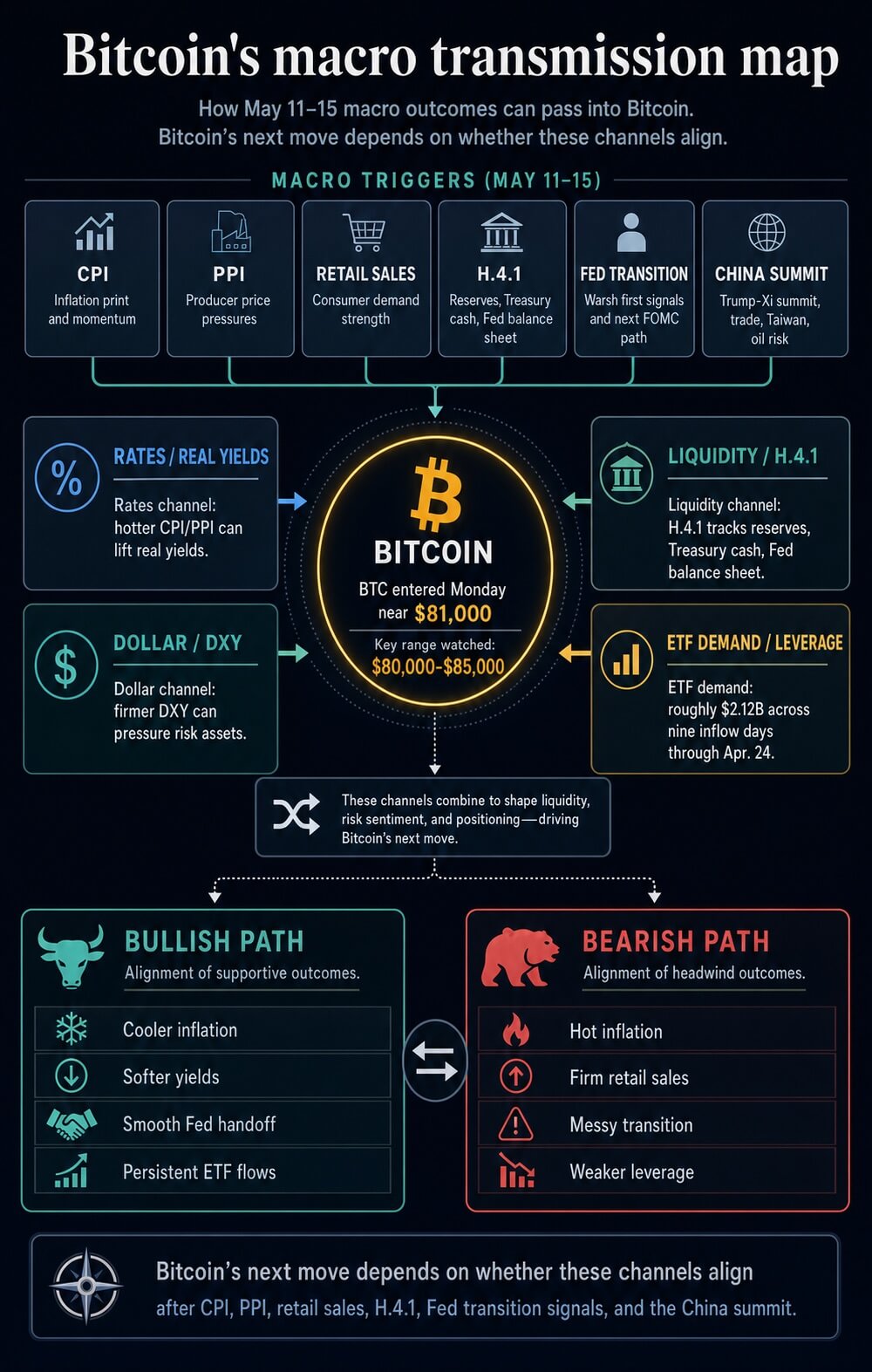

This week (May 11-15) has a credible claim to being the most consequential macro window of 2026 so far, as it compresses every channel currently driving risk assets into a single sequence.

Inflation, producer costs, consumer demand, Fed liquidity, central bank leadership, trade risk, oil risk, and the dollar are all scheduled to move within five trading days.

Bitcoin enters that window as a liquidity-sensitive institutional asset, making the calendar a direct test of whether the recovery above $80,000 has macro sponsorship or only positioning support.

The strongest rival week came earlier in the year, when the Iran conflict and the Strait of Hormuz shock pushed energy markets into the center of the inflation debate.

The St. Louis Fed's review of market reactions to military action against Iran marked Feb. 28, Mar. 1, and Apr. 13 as key shock points for oil, volatility, and geopolitical repricing.

That episode carried the larger single exogenous impulse. It changed the inflation path through energy, widened the risk premium in crude, and forced investors to reprice the Fed's tolerance for cutting into a supply shock.

The March inflation data then showed how that shock entered the official series. The March CPI report showed consumer prices rising 0.9% month over month and 3.3% year over year, with energy up 10.9% and gasoline up 21.2%. The March PPI report showed final demand prices rising 0.5% in March and 4.0% over the prior 12 months, the largest annual increase since February 2023.

Those prints gave 2026 a genuine inflation shock rather than a routine data scare.

April 28-29 was the other major comparison point because it combined an FOMC decision, dissents, oil-related inflation anxiety, and the Senate Banking Committee's movement on Kevin Warsh.

The Fed held rates at 3.5% to 3.75%, but the April FOMC statement carried an unusually fractured vote. One governor dissented in favor of a 25 basis point cut, while three officials supported the hold and opposed language that leaned toward easing.

That meeting exposed a central bank split between inflation caution and growth insurance.

May 11-15 ranks above those weeks in event density.

The Iran shock was larger as a geopolitical impulse. The April FOMC was sharper as a policy signal.

This week combines both transmission paths and adds a leadership handoff. It forces markets to price in inflation persistence, consumer resilience, Treasury and reserve mechanics, Fed credibility, and U.S.-China geopolitical risk simultaneously.

For Bitcoin, that makes it the broadest macro stress test of the year so far.

The official calendar stacks inflation, demand, Fed liquidity, leadership risk, and China into one macro test sequence

The official sequence begins with inflation.

The Bureau of Labor Statistics has the April CPI release scheduled for Tuesday, May 12 at 8:30 a.m. ET.

It then has the April PPI release scheduled for Wednesday, May 13 at 8:30 a.m. ET.

That pairing gives markets a two-day signal on whether the March energy shock and tariff pressure are still moving through consumer and producer prices, or whether the inflation impulse is already losing force.

Thursday broadens the test from prices to demand and liquidity.

The Census Bureau has April retail sales scheduled for Thursday, May 14 at 8:30 a.m. ET.

The Federal Reserve's May calendar lists H.4.1 balance sheet data for the same day at 4:30 p.m. ET.

That means markets receive a consumer-demand signal in the morning and a liquidity signal after the close.

A strong retail number alongside hot inflation would reinforce the case for policy restraint. A weaker retail print alongside softer inflation would give the next Fed chair more room to argue that the economy can absorb lower rates.

The balance sheet release carries direct information for crypto. The May 7 H.4.1 report showed total Fed assets near $6.71 trillion, reserve balances around $3.03 trillion on average, and the Treasury General Account near $878 billion on average.

For Bitcoin, the direction of reserves and Treasury cash balances often carries more direct market information than the headline size of the Fed's asset portfolio.

Falling reserves and a large Treasury cash balance can keep liquidity tight even when investors expect easier policy later.

Friday then adds the leadership handoff.

Jerome Powell's official term as Fed chair ends May 15, while his Board term runs to January 2028.

Powell also said at the Apr. 29 press conference that he expected to continue serving as a governor for a period after the chair term, while keeping a low public profile.

Kevin Warsh's nomination sits on the same track. The Senate Banking Committee held a nomination hearing on Apr. 21, and the committee later advanced him on a party-line vote.

Warsh could inherit his first inflation test before markets know his reaction function

Wednesday's official anchor is PPI, while the Fed calendar lists other officials and provides no primary-source basis for making a chair speech the central event.

The larger issue sits at the end of the week: Warsh could inherit his first inflation signal before his reaction function is visible.

If CPI or PPI accelerates, the new chair begins boxed in by data.

If inflation cools, he begins with room to define how quickly the Fed can pivot without inviting a bond-market credibility premium.

President Donald Trump's China trip then widens the map. He is scheduled to meet Xi Jinping in Beijing during a May 14-15 visit, according to AP.

That summit adds trade, tariffs, Taiwan, oil logistics, and dollar-risk channels to the same window as CPI, PPI, retail sales, H.4.1, and the Fed leadership transition.

A constructive summit could lower the trade-risk premium and ease the dollar bid.

A tense summit could lift the dollar and pressure offshore liquidity, especially if energy security and the Iran war remain tied to the negotiations.

That combination makes the week structurally different from the usual CPI cycle. Inflation data alone can move Bitcoin. A new Fed chair inheriting that data can change how markets price the next several meetings.

Warsh's nomination has already been framed around institutional change at the central bank, including questions about models, communications, bond holdings, and the Fed's reaction function.

That creates an immediate test: does the market treat the transition as a path toward a more responsive Fed, or as a source of uncertainty around independence, inflation tolerance, and the long-run policy framework?

A hotter sequence would put Warsh in the hardest possible opening position.

CPI and PPI strength would raise doubts about near-term cuts.

Strong retail sales would reduce the urgency for demand support.

Elevated oil prices would keep the inflation path vulnerable.

A tense Beijing summit would support the dollar through trade and geopolitical risk.

In that environment, a dovish signal from the incoming chair could backfire if bonds interpret it as political pressure or premature easing.

Bitcoin might initially respond to the idea of easier policy, but a rise in real yields and the dollar would likely cap that response.

Bitcoin's macro test transmission map runs through real yields, the dollar, ETF flows, leverage, and reserves

Bitcoin enters the week near $81,000 after recovering from the high-$75,000s around the Apr. 29 FOMC period.

That rally improved the chart structure, but the next leg depends on whether macro variables confirm the move. The relevant channel is now broader than spot demand on crypto exchanges.

Bitcoin now trades through real yields, the dollar, ETF allocation flows, leverage conditions, and the same liquidity variables that shape equities and credit.

The first channel is rates.

A hot CPI print would likely lift nominal yields and real yields if markets conclude that the Fed has less room to cut. A cooler CPI print would likely ease that pressure, especially if core inflation softens alongside headline inflation.

The distinction is important because an energy-driven headline shock can produce an awkward signal.

Powell said after the Apr. 29 meeting that officials wanted to see progress beyond the energy shock and tariff effects before easing.

If April shows hot headline inflation with cooler core inflation, the market reaction may depend on whether Warsh signals patience, urgency, or a willingness to look through the oil impulse.

The second channel is the dollar.

CryptoSlate's prior work on Bitcoin, M2, and dollar strength showed how a stronger dollar can interrupt the transmission from expanding global liquidity to BTC.

That remains the central macro risk. Bitcoin can benefit from easier policy expectations, but a rising dollar can offset that impulse by tightening global financial conditions.

This is why the Trump-Xi meeting sits inside the Bitcoin trade. Trade relief can soften the dollar and lower risk premia. Escalation can lift the dollar and pressure offshore liquidity.

The third channel is the Fed balance sheet and Treasury cash.

A Thursday H.4.1 release showing rising reserves and easing pressure from the Treasury General Account would give Bitcoin a stronger liquidity foundation.

A release showing reserve drain alongside a still-large Treasury cash pile would make any rally more dependent on ETF inflows and leverage.

CryptoSlate's analysis of debt, liquidity, and Bitcoin has already shown that aggregate liquidity can look supportive while the usable liquidity reaching risk assets remains constrained.

The next major Bitcoin move depends on whether macro test channels align

The fourth channel is institutional flow.

Since the launch of U.S. spot Bitcoin ETFs, BTC has become easier for traditional portfolios to buy, rebalance, and sell.

CryptoSlate's coverage of the ETF-driven market-structure shift described how institutions have become a primary force in Bitcoin liquidity and price formation.

A separate analysis of passive money noted that U.S. spot Bitcoin ETFs had accumulated roughly $58.4 billion in cumulative net inflows by late April, with IBIT above $60 billion in net assets, reinforcing how far Bitcoin has moved into traditional allocation workflows through ETF wrappers.

That structure works in both directions.

ETF inflows can amplify a macro relief rally when yields fall, and the dollar weakens. ETF outflows can accelerate downside when real yields rise, the dollar strengthens, and leveraged traders are forced to reduce exposure.

A hot CPI and PPI sequence, strong retail sales, falling reserves, and a tense Trump-Xi outcome would be the most difficult mix for BTC because every transmission channel would point toward tighter financial conditions.

A cooler inflation sequence, resilient but slowing retail sales, improving reserves, and a less hostile China signal would give Bitcoin the strongest macro foundation it has had in 2026.

A cooler sequence would change the setup. Softer CPI and PPI would validate the idea that the March energy spike was passing through rather than embedding.

A slower but stable retail number would support a soft-landing path. A Thursday balance sheet release showing firmer reserves would improve the liquidity backdrop. A constructive Trump-Xi meeting would reduce the trade-risk premium and could weaken the dollar.

In that scenario, Warsh would have more room to define a gradual policy pivot without starting his tenure under immediate inflation pressure.

Bitcoin would then have a clearer path to test higher levels, provided ETF creations expand, and derivatives positioning avoids an unstable long build.

The mixed outcome may be the most realistic one.

Headline inflation can stay firm because of energy while core inflation cools. Retail sales can remain solid in nominal terms while real demand slows. The Fed balance sheet can show a large aggregate asset base while reserves remain under pressure. Trump and Xi can produce limited trade relief while leaving Taiwan, oil logistics, and tariff enforcement unresolved.

That mix would keep Bitcoin in a macro waiting zone. It would reward intraday volatility, but it would withhold the confirmation needed for a durable range expansion.

The next test is specific.

- Watch Warsh's first signals on inflation tolerance, balance-sheet policy, and central-bank independence.

- Watch the June FOMC path, especially whether the statement language shifts after the leadership handoff.

- Watch real yields and DXY before treating Bitcoin's move as confirmation.

- Watch H.4.1 reserves and the Treasury General Account before assuming liquidity has improved.

- Watch spot ETF net flows, funding rates, and liquidation clusters before treating a breakout as structurally supported.

If those variables align, May 11-15 becomes the week Bitcoin regained a macro tailwind after months of rate, dollar, and oil pressure.

If they fail to align, the week becomes a sharper lesson in the post-ETF regime: Bitcoin can trade like a scarce asset, a liquidity asset, and an institutional risk asset at the same time.

The direction of the next major move will come from which identity markets choose after CPI, PPI, retail sales, H.4.1, Warsh, and Trump-Xi all hit the same window.

The post This week Bitcoin faces as a new fed chair colliding with inflation in its biggest macro test of the year appeared first on CryptoSlate.