The Role of BIN Routing in Cross-Border Payments

--

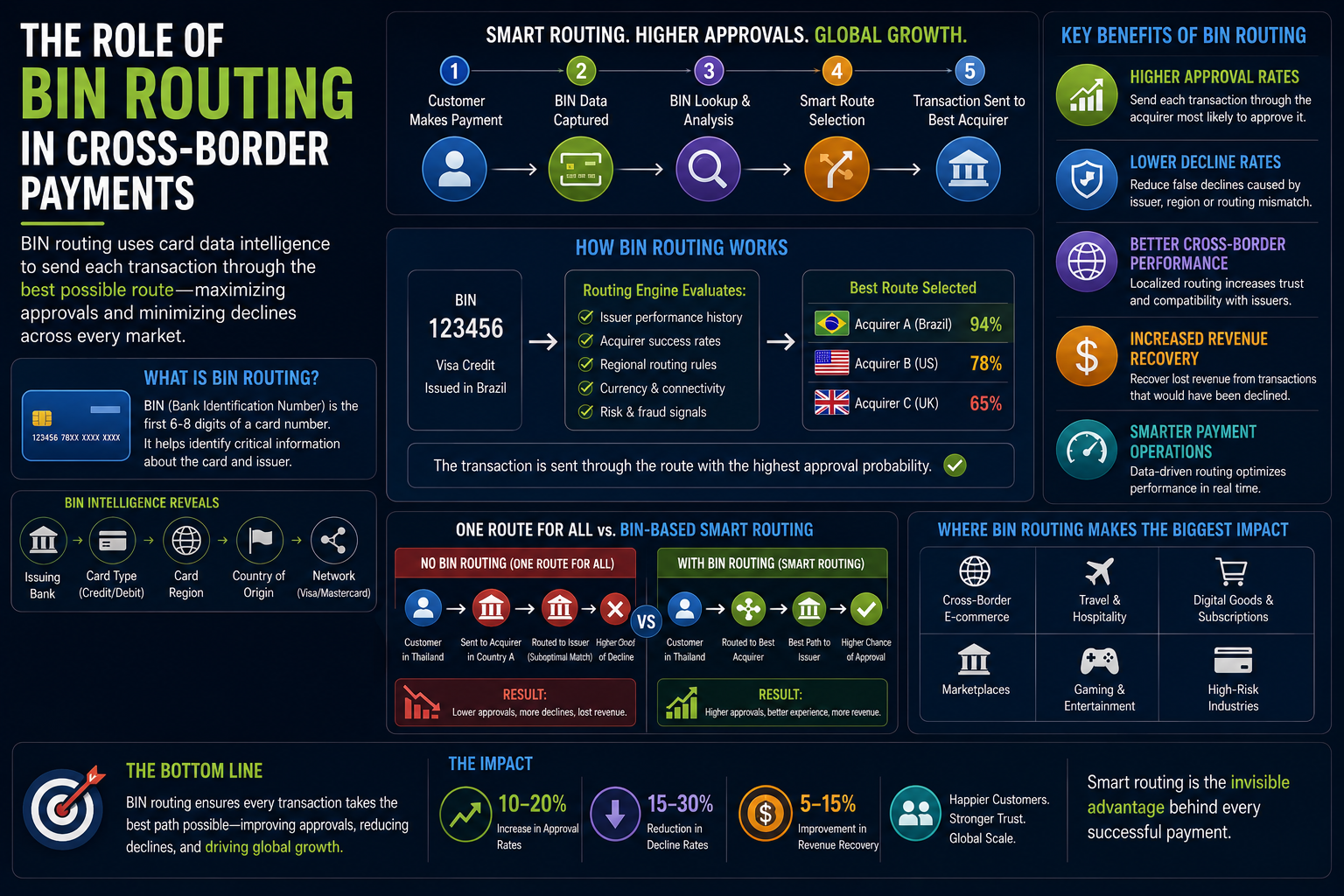

BIN routing has become a critical tool for improving cross-border payment performance. The Bank Identification Number, or BIN, refers to the first digits of a payment card that identify the issuing bank and country.

Modern payment systems use BIN data to make intelligent routing decisions before transactions reach the issuer. This improves authorization efficiency and reduces unnecessary declines.

For example, if a card originates from a specific country, the payment can route through a local acquirer within that region rather than an international processor.

Localized routing increases issuer trust because the transaction appears more domestic and less risky.

BIN routing also helps businesses optimize costs. Different acquirers offer varying interchange rates, approval performance, and settlement structures depending on the region.

Enterprise merchants often combine BIN routing with multi-acquiring strategies to maximize payment efficiency globally.

Fraud management benefits as well. BIN data provides additional insight into issuer behavior, geographic patterns, and transaction risk signals.

Subscription businesses use BIN routing to improve recurring payment success by identifying the most effective acquiring path for specific issuers.

As payment infrastructure becomes more sophisticated, BIN routing is evolving into a foundational layer for international payment optimization and scalable global commerce.

BIN routing has become a critical tool for improving cross-border payment performance. The Bank Identification Number, or BIN, refers to the first digits of a payment card that identify the issuing bank and country.

Modern payment systems use BIN data to make intelligent routing decisions before transactions reach the issuer. This improves authorization efficiency and reduces unnecessary declines.

For example, if a card originates from a specific country, the payment can route through a local acquirer within that region rather than an international processor.

Localized routing increases issuer trust because the transaction appears more domestic and less risky.

BIN routing also helps businesses optimize costs. Different acquirers offer varying interchange rates, approval performance, and settlement structures depending on the region.

Enterprise merchants often combine BIN routing with multi-acquiring strategies to maximize payment efficiency globally.

Fraud management benefits as well. BIN data provides additional insight into issuer behavior, geographic patterns, and transaction risk signals.

Subscription businesses use BIN routing to improve recurring payment success by identifying the most effective acquiring path for specific issuers.

As payment infrastructure becomes more sophisticated, BIN routing is evolving into a foundational layer for international payment optimization and scalable global commerce.

BIN routing has become a critical tool for improving cross-border payment performance. The Bank Identification Number, or BIN, refers to the first digits of a payment card that identify the issuing bank and country.

Modern payment systems use BIN data to make intelligent routing decisions before transactions reach the issuer. This improves authorization efficiency and reduces unnecessary declines.

For example, if a card originates from a specific country, the payment can route through a local acquirer within that region rather than an international processor.

Localized routing increases issuer trust because the transaction appears more domestic and less risky.

BIN routing also helps businesses optimize costs. Different acquirers offer varying interchange rates, approval performance, and settlement structures depending on the region.

Enterprise merchants often combine BIN routing with multi-acquiring strategies to maximize payment efficiency globally.

Fraud management benefits as well. BIN data provides additional insight into issuer behavior, geographic patterns, and transaction risk signals.

Subscription businesses use BIN routing to improve recurring payment success by identifying the most effective acquiring path for specific issuers.

As payment infrastructure becomes more sophisticated, BIN routing is evolving into a foundational layer for international payment optimization and scalable global commerce.

BIN routing has become a critical tool for improving cross-border payment performance. The Bank Identification Number, or BIN, refers to the first digits of a payment card that identify the issuing bank and country.

Modern payment systems use BIN data to make intelligent routing decisions before transactions reach the issuer. This improves authorization efficiency and reduces unnecessary declines.

For example, if a card originates from a specific country, the payment can route through a local acquirer within that region rather than an international processor.

Localized routing increases issuer trust because the transaction appears more domestic and less risky.

BIN routing also helps businesses optimize costs. Different acquirers offer varying interchange rates, approval performance, and settlement structures depending on the region.

Enterprise merchants often combine BIN routing with multi-acquiring strategies to maximize payment efficiency globally.

Fraud management benefits as well. BIN data provides additional insight into issuer behavior, geographic patterns, and transaction risk signals.

Subscription businesses use BIN routing to improve recurring payment success by identifying the most effective acquiring path for specific issuers.

As payment infrastructure becomes more sophisticated, BIN routing is evolving into a foundational layer for international payment optimization and scalable global commerce.

Businesses that prioritize payment infrastructure optimization gain stronger approval rates, improved customer trust, and more sustainable international growth. In modern global commerce, payments are no longer just operational systems — they are strategic revenue infrastructure.