THE PROTOCOL THAT GREW TOO FAST TO SELL

VICTOR RAPHAEL3 min read·Just now

VICTOR RAPHAEL3 min read·Just now--

Three Buyers Came at the Right Moment. He Wanted More. By the Time He Was Worth More, the Deal Had Become Impossible.

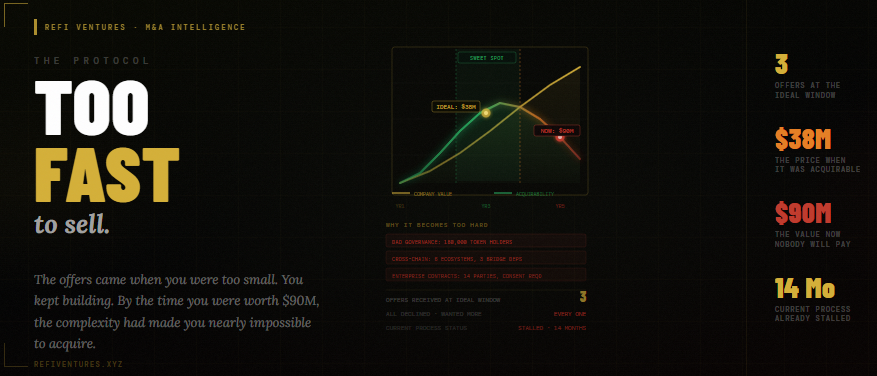

The first offer arrived when the protocol was valued at $22 million. He declined. Too low.

The second came fourteen months later at $38 million. He declined again. The protocol was growing and he knew it. The third was $41 million. He countered at $65 million. The buyer walked.

Two years later the protocol was generating $11 million in annualized fees and had a reasonable claim to a $90 million valuation. It had also expanded to six blockchain ecosystems, accumulated 180,000 DAO token holders with governance rights over any structural change to the protocol, and signed fourteen enterprise contracts with consent-to-assignment clauses that made a transfer of ownership legally complex to execute without each counterparty’s individual agreement.

He was worth more. He was also nearly impossible to acquire.

The acquisition process he launched at $90 million had been running for fourteen months. Three serious buyers had entered due diligence and exited. Not because of the product. Not because of the price. Because of the closing mechanics.

Every Web3 protocol has an acquirability curve that runs parallel to its value curve — and they do not peak at the same time. In the early stages both curves rise together. The protocol is worth more and easier to acquire simultaneously. Then the complexity compounds. Governance structures accumulate. Multi-chain deployments create dependency chains that require coordinated transitions. Enterprise contracts add consent requirements. Token holder bases grow into constituencies that must be managed, not just notified. The value continues to climb. The acquirability begins to fall.

The inflection point — the moment where value and acquirability are both at their highest simultaneously — is the optimal acquisition window. It is not marked on any calendar. It is not announced. It passes while founders are focused on building the next milestone.

The founder above hit his optimal window somewhere between the $38 million and $41 million offers. At that point his governance structure was manageable, his chain deployments were limited enough that a technical transition was feasible, and his enterprise contracts were early enough in their terms that consent-to-assignment could be obtained with reasonable effort. He declined all three offers because the price felt insufficient relative to where he was heading.

He was right that he was heading somewhere. He was wrong that the acquirability would follow him there.

The compounding complexity problem in Web3 and AI acquisitions accelerates faster than founders anticipate. Each new blockchain integration is not merely one more item in a due diligence checklist — it is an additional dependency chain, an additional security audit requirement, and an additional set of smart contract risks that an acquirer must underwrite. Each governance expansion is not just community growth — it is a vote pool that an acquirer must navigate without triggering a community revolt that destroys the asset they are buying. Each enterprise contract with a consent clause is a party whose approval must be secured, whose legal team must be engaged, and whose potential objections must be managed before the deal can close.

At some threshold of complexity, the transaction cost of acquiring a protocol approaches the transaction cost of building a competing one. That threshold is lower than most founders realize and much lower than it would be for a comparable SaaS business, where the technical assets are more portable and the stakeholder structure is more conventional.

The founders who consistently exit at premium multiples are the ones who understand this dynamic before it becomes their constraint. They monitor their own acquirability as deliberately as they monitor their growth metrics. They know when the complexity of their governance structure, their multi-chain deployment, and their contractual obligations is approaching a threshold that will make them difficult to acquire — and they make the exit decision before that threshold is crossed, not after.

Growth is not a reason to delay. Sometimes it is the reason to move.

The window where your value and your acquirability align is the only window that matters.

Assess your acquisition window before it closes at refiventures.xyz