The Number Nobody is Watching in Circle’s Q1 Results

--

The first article in a series on the infrastructure capture of tokenized finance. Full analysis with valuation framework on Substack.

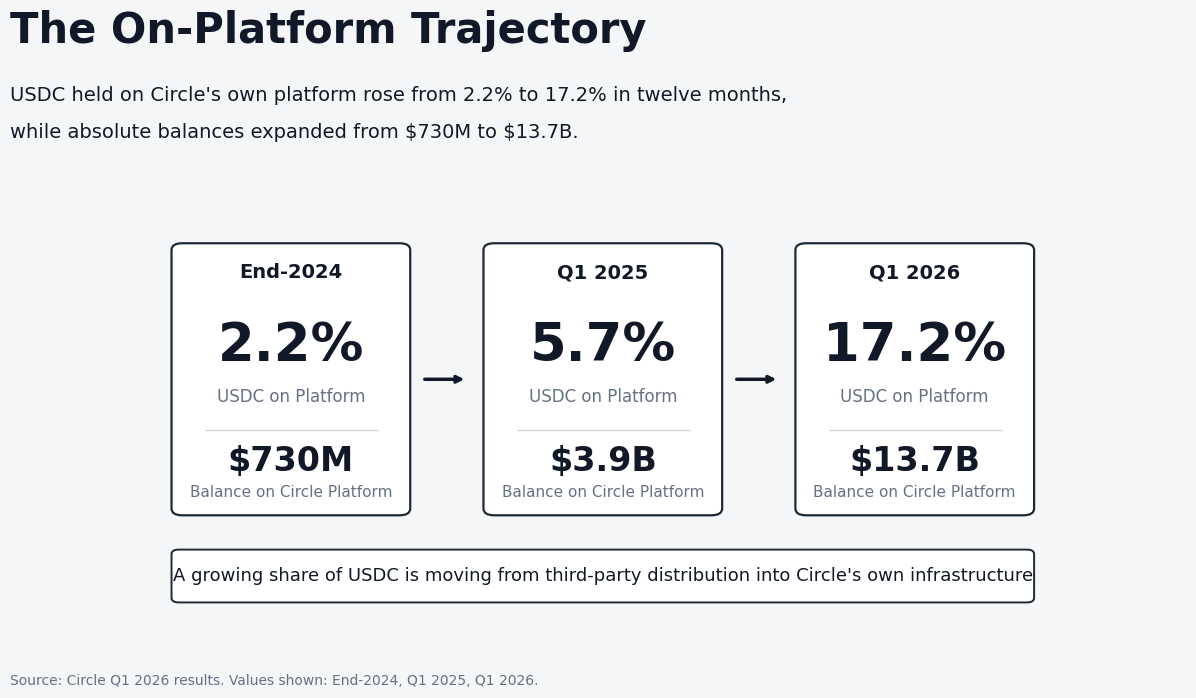

$77 billion of USDC is currently in circulation. Around $13.7 billion of that sits on Circle’s own platform — a number that one year ago was less than $4 billion. At a 3.5% reserve yield, those $13.7 billion generate approximately $480 million of annualized interest income that Circle keeps in its entirety, without sharing any portion with Coinbase, Binance, or any other distribution partner. One year ago the same calculation produced about $130 million. Circle has quietly added more than $350 million of annualized gross economics in twelve months simply by moving stablecoins from the third-party distribution perimeter onto its own infrastructure.

This is the single metric that explains why Circle, despite trading at 54 times trailing EBITDA, is more interesting as an infrastructure play than as a stablecoin issuer. The official narrative is about $77 billion of USDC, 28% stablecoin market share, BlackRock partnership, and Federal Reserve rate trajectory. The actual story is that Circle has spent the last eighteen months building the rails, custody arrangements, payment networks, tokenized yield instruments, and blockchain settlement infrastructure that could turn a stablecoin issuer into the operating layer of tokenized capital markets. The metric that measures whether the strategy is working is the share of USDC held on Circle’s own platform, and that metric has tripled in a year.

This article is the first in a series on the infrastructure capture of tokenized finance. The series is built on a wager that tokenization is not best understood as a single transition but as the parallel capture of three distinct infrastructure layers — money, credit, and the equity registry. Each layer is being claimed by a different company, through a different strategic path. Money goes first because money does not need anyone’s permission to migrate; Circle is the company that made it migrate. The next two articles will trace how Figure Technology Solutions is consolidating the credit layer, and how Bullish Group’s acquisition of Equiniti Trust Company is positioning to capture the equity registry. This first article establishes why money goes first, why Circle has structural advantages that the market has not yet fully priced, and what the $13.7 billion observation actually implies.

Why these $13.7 billion matter — and what they imply for Circle’s revenue trajectory through 2027 — is the subject of the full analysis on Substack. What follows here is the underlying structural argument that makes the on-platform shift possible.

What Circle is today

Circle was founded in 2013 with the proposition that the internet would eventually carry value the same way it carries information. After several years of unsuccessful experiments, the company settled in 2018 on a single thesis: issue a regulated, fiat-backed stablecoin to become the institutional alternative to Tether’s USDT. Seven years later, USDC ended Q1 2026 with $77 billion in circulation and approximately 28% of the dollar-pegged stablecoin market by supply.

The supply share understates Circle’s position. By transaction volume the gap is wider: USDC accounts for 63% of all stablecoin transaction volumes according to Visa Onchain Analytics, with $21.5 trillion processed in the quarter — up 263% year-over-year. USDT remains larger by circulation at roughly $184 billion, but USDC is being used more intensively per dollar outstanding, and that gap is widening.

The business model is mechanically simple. Circle accepts dollar deposits, issues equivalent USDC, and invests the deposits in short-duration Treasury bills. Approximately 86% of reserves sit in the Circle Reserve Fund managed by BlackRock specifically for Circle, with BNY Mellon as custodian. In Q1 2026, those reserves produced $653 million of reserve income, of which $406 million flowed to distribution partners (mostly Coinbase) and $151 million reached Adjusted EBITDA. That structure — Treasury yield on $77 billion of segregated reserves, split with distribution partners — is what Circle has been. What it is becoming requires understanding one specific structural detail.

The trust premium that nobody mentions

Buried in Circle’s most recent 10-K is one sentence that explains why USDC is structurally different from most other dollar-pegged stablecoins:

The Company holds only bare legal title in the accounts holding the reserve funds, and maintains no legal, equitable, financial or ownership interest over the reserves themselves held for the benefit of Circle stablecoin holders in such accounts.

What this sentence does legally is sever the connection between Circle as a corporate entity and the assets backing USDC. The Treasury bills, repo agreements, and bank deposits backing the stablecoin are held in segregated accounts where Circle functions, in effect, as a passive trustee. If Circle were to enter bankruptcy tomorrow, USDC holders would likely have a significantly stronger claim on the segregated reserves than general unsecured creditors — although the treatment of stablecoin reserves in an issuer bankruptcy remains a relatively untested area of law. The reserves do not belong to Circle in any meaningful legal sense; they belong to the holders of the tokens.

This is not how Tether is structured. Tether Limited holds reserves on its own balance sheet, and USDT holders would have to litigate their claims against a British Virgin Islands entity through whatever bankruptcy or receivership process emerged. The Tether attestations describe the composition of reserves but do not provide the same legal separation. It is also not how the major bank-issued stablecoin experiments work, where the tokenized dollar is essentially a deposit liability and the holder is exposed to bank credit risk like any other depositor.

For retail users moving small amounts of USDC between wallets, this distinction is invisible. For an institutional treasurer deciding whether to hold $500 million in USDC as part of corporate cash management, this distinction is the entire decision. A corporate treasurer is not paid to take credit risk on a stablecoin issuer; she is paid to hold dollars in instruments that are legally as close to dollars as possible. Circle’s legal segregation is arguably the structure that gets USDC closest to being treasury-acceptable as an institutional dollar instrument. No competitor has been able to credibly replicate that structure at scale.

The trust premium shows up in the data. When BlackRock launched its BUIDL tokenized Treasury fund, the chosen settlement currency was USDC. When Visa pilot-tested stablecoin merchant settlement, USDC was the rail. When Stripe relaunched stablecoin acceptance, the default offering was USDC. And as the transaction volume data shows, USDC accounts for 63% of all stablecoin transaction volume despite being only 28% of supply — a 2.25x utilization premium that reflects where the institutional flow concentrates. USDC has become the institutional default in regulated settings, and the differentiator is not pricing or liquidity. It is legal structure.

This is the structural moat that makes Circle’s money layer capture work. It took Circle seven years of regulatory engagement, custody arrangements, and bankruptcy-remote structuring to build. It would take a competitor approximately the same length of time to match it credibly.

Why money goes first

Of the three infrastructure layers this series will track — money, credit, and the equity registry — money was always going to tokenize first. The reason is structural. A dollar tokenized as USDC is still a dollar. It represents a claim on a reserve of Treasury bills and bank deposits, trades at par, and serves the same monetary function. The only thing that changes is the rails it travels on.

Credit and equity are different. Tokenizing them requires rebuilding the scaffolding around the asset — lien registration, transfer agency, regulatory recognition — that took decades to construct under traditional infrastructure. The next two articles in this series will examine exactly how that rebuilding is happening: Figure Technology Solutions taking the credit layer through a 94% cost compression in mortgage origination on the Provenance blockchain, and Bullish Group taking the equity registry through its acquisition of Equiniti, a regulated transfer agent serving 35% of the S&P 500. Both are harder than what Circle did. Both will take longer. And both depend, ultimately, on the money layer that Circle has already built.

Circle gave us money. The next two articles will trace how credit and the equity registry are following. The institutional capital recognizing this — the same group of investors that participated in Circle’s $222 million Arc Token presale in May 2026, including BlackRock, Apollo, ICE, Janus Henderson, Standard Chartered, and Bullish itself — is increasingly placing the same bet across all three layers.

Read the full analysis

The full version of this analysis on Substack covers what the structural foundation produces in practice — the revenue mechanics, the competitive dynamics, and the valuation that the on-platform shift implies:

• The volume × yield compounding math that explains why 39% USDC growth produced only 17% reserve income growth in Q1 2026, and what it implies for 2026–2027 trajectory

• The Coinbase renewal mechanics — why the August 2026 auto-renewal provision favors Circle rather than Coinbase, despite $1.3 billion in annualized distribution payments flowing to a single counterparty

• The BlackRock alliance economics — how a potential competitor became a structural beneficiary, and why the May 2026 ARC Token participation extends that alignment from money into settlement

• The full breakdown of the on-platform shift — where the $13.7 billion actually sits, why it is compounding, and how it could reach $35–45 billion by 2027

• Arc, USYC, and CPN as three distinct adjacent infrastructure builds, each with different competitive dynamics and execution risks

• The valuation framework — probability-weighted scenarios producing a fair value around $120 per share against the current $121, with explicit articulation of bear, base, and bull cases

The next two articles in this series — on Figure Technology Solutions and the credit layer, and on Bullish Group’s acquisition of Equiniti and the equity registry layer — will follow on Substack. Subscribe to receive them as they publish.

→ Read the full analysis on Substack [https://substack.com/@bzmachina/note/p-197486603?utm_source=notes-share-action&r=8elc4f]