Member-only story

The Mirage of the Clean Backtest

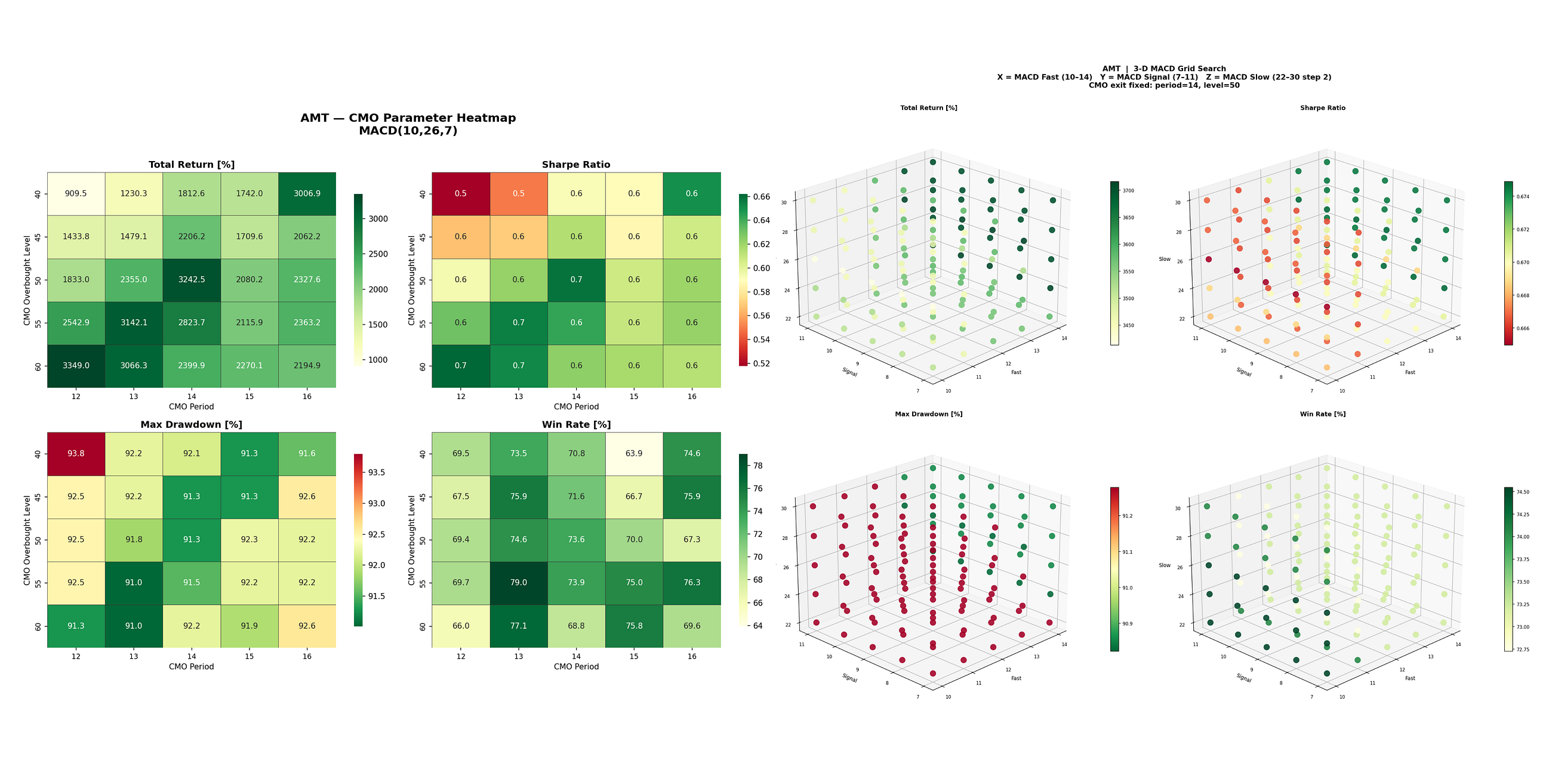

A MACD momentum + CMO exit strategy on American Tower looked exceptional in backtesting — robust parameters, smooth equity curve, 2,500% return. Walk-forward testing told a quieter truth.

Kryptera13 min read·Just now

Kryptera13 min read·Just now--

Every systematic trader eventually meets this strategy. The idea is clean, the indicators are well-established, and the in-sample numbers are genuinely impressive. But once you apply walk-forward validation — the closest approximation to live trading that backtesting software can offer — the story changes. Not because the strategy is broken, but because it was never capturing an edge above what the underlying asset was already doing.

This is the autopsy of that strategy on American Tower Corporation (AMT).

The Strategy

import pandas as pd

import numpy as np

import yfinance as yf

import vectorbt as vbt

# -------------------------

# Download Data

# -------------------------

symbol = "AMT"

start_date = "2002-01-01"

end_date = "2030-01-01"

interval = "1d"

df = yf.download(symbol, start=start_date, end=end_date, interval=interval, multi_level_index=False)

df.reset_index().to_csv("AMT_clean.csv", index=False)

# -------------------------

# Necessary Parameters

# …