From the 2025 Liquidity Peaks to the Q1 2026 Structural Correction

Core Insight: The 50% drop in aggregate Total Value Locked (TVL) from the October 2025 peaks is not a systemic collapse; it is a healthy, capitalist deleveraging cycle. By purging inflationary incentives and speculative loops, the decentralized credit ecosystem has successfully transitioned into a self-sustaining, cash-flow-positive infrastructure. For the first time, protocol survival depends on real utility rather than token printing.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial, investment, or professional advice. We do not recommend any buying, selling, or holding of digital assets.

All views are the author’s own. Digital assets involve high risk and volatility, and readers should conduct their own research before making any decisions.

This report is not sponsored by any mentioned companies.

1. Sector-Wide Macro Analysis: The Anatomy of Market Contraction

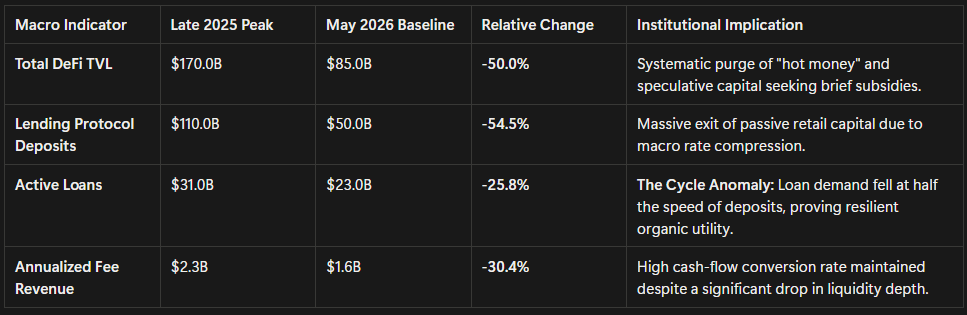

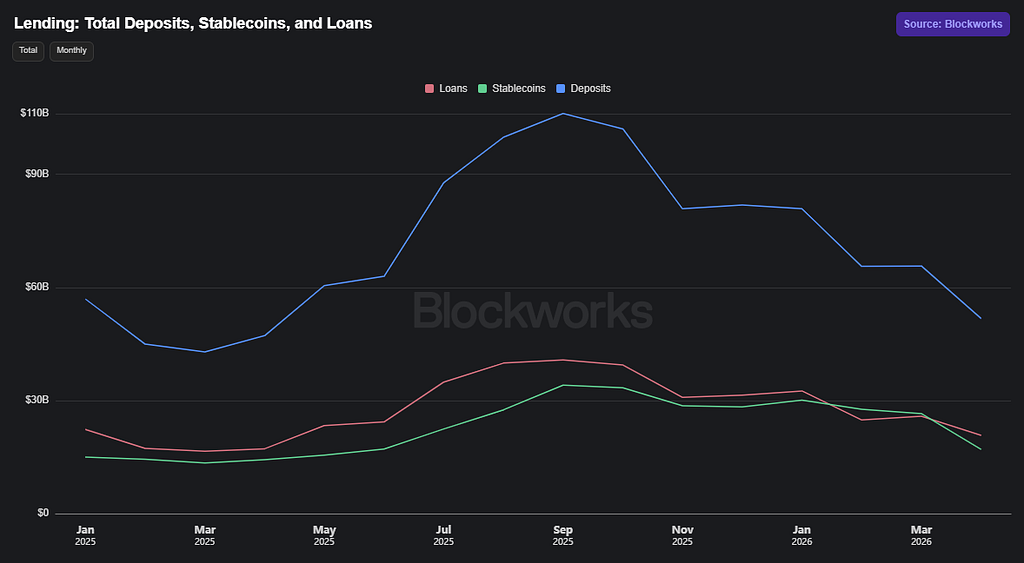

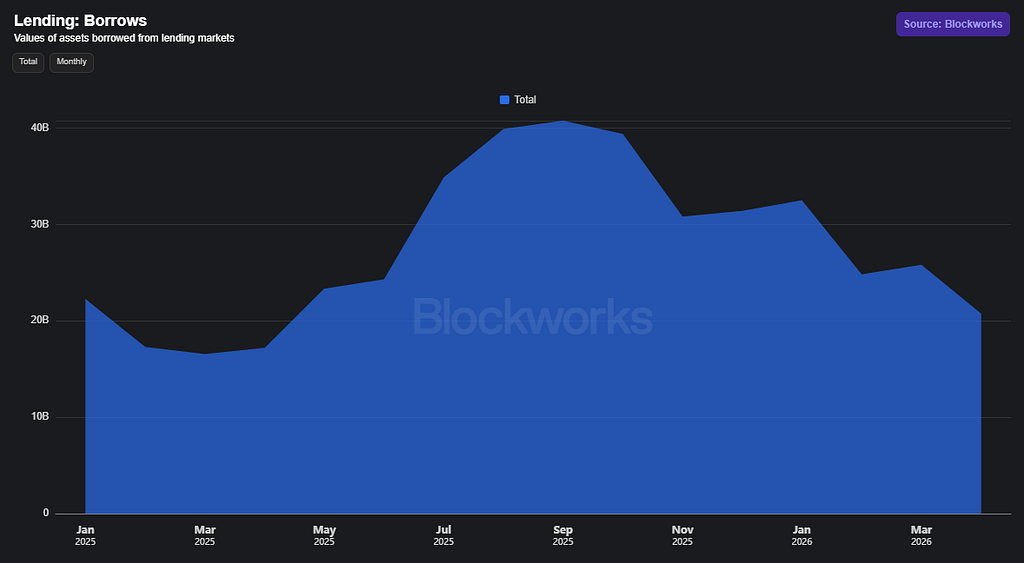

The market realignment between October 2025 and May 2026 served as the ultimate stress test for decentralized credit architectures. Total DeFi TVL contracted from a local peak of $170 billion to a stabilized range of $85 billion. However, a deeper look into underlying credit velocity reveals a sector becoming fundamentally tighter and more capital-efficient.

Global Macro Indicators of the DeFi Credit Market

Top Three Sector Macro Trends

A. The Capital Utilization Efficiency Split

A major divergence appears when comparing deposit contraction (-54.5%) against active loan contraction (-25.8%). In traditional fractional-reserve banking, losing half of your deposit base triggers a catastrophic run on the bank.

In DeFi, it triggered an automatic optimization:

- The system-wide capital utilization rate (loans divided by deposits) sharply increased.

- The remaining capital in the ecosystem is working twice as hard.

- Borrowers engaging in structural economic activities — such as cross-venue arbitrage, delta-neutral yield strategies, and MEV (Maximal Extractable Value) liquidity — have remained entirely intact. Only “yield tourists” providing passive, subsidized liquidity left.

B. The Transition to Pure Cash-Flow Protocols

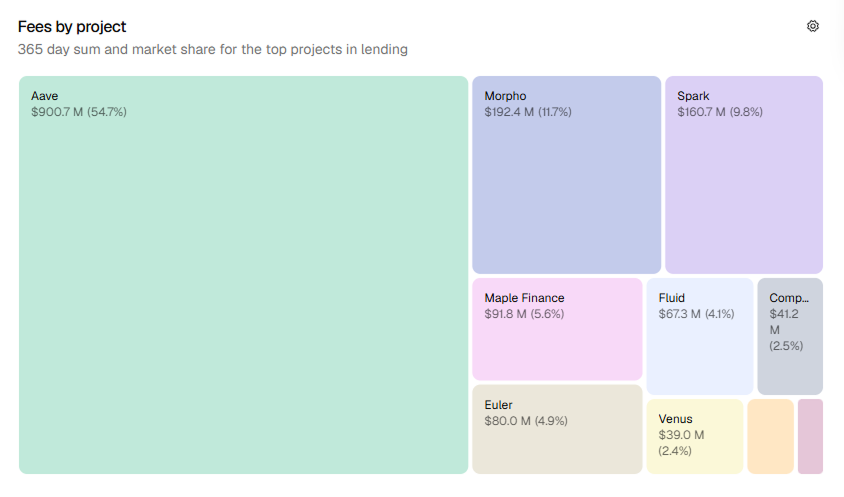

Annualized fee revenue fell by only 30.4% ($1.6B) relative to the 50% drop in raw TVL. This confirms that DeFi has successfully abandoned artificial business growth. In previous cycles, bloated TVL metrics were manufactured by paying out inflationary governance tokens to users (Yield Farming). In 2026, the $1.6 billion generated represents true organic fees paid by borrowers for actual access to liquidity. The sector is now fully sustainable on its own income.

C. The Elimination of Cascading Leverage

The compression of active loans to $23 billion signals that looping leverage (e.g., depositing ETH $\rightarrow$ borrowing USDC $\rightarrow$ buying more ETH $\rightarrow$ re-depositing) has been effectively wiped out. Loans are now predominantly linear and targeted. This institutional turn is highlighted by specialized private-credit protocols like Maple Finance, where corporate active loans grew by +3,336%, bypassing the retail market entirely to service institutional on-chain credit demand.

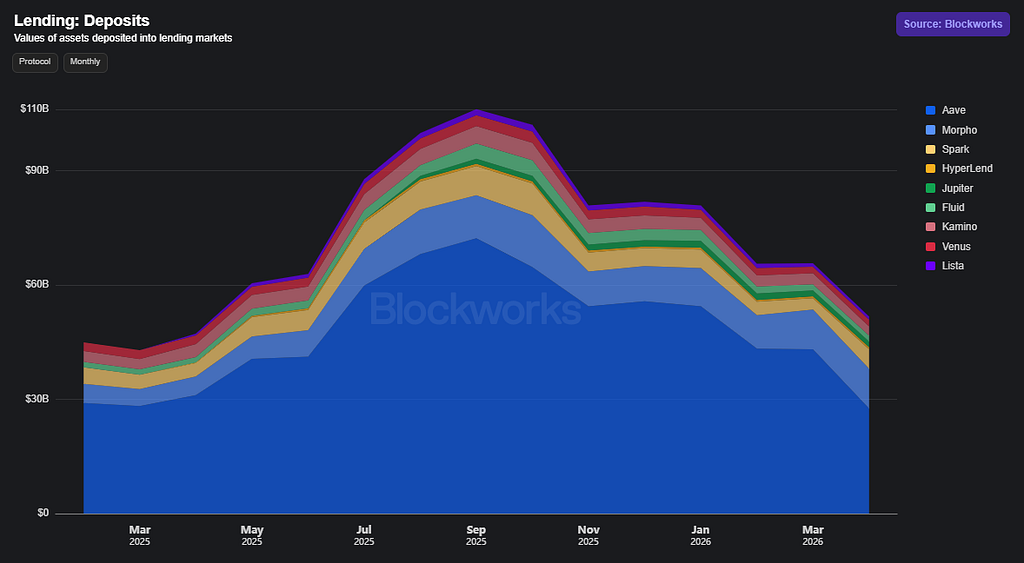

2. Liquidity Consolidation: The End of Fragmentation

The era of hyper-fragmentation — where lookalike protocols popped up daily and diluted billions of dollars in liquidity — is officially over. Capital has fled to safety. The lending landscape has consolidated into a highly efficient oligopoly where over 82% of all credit deposits are held by just three heavyweights:

Total Lending Sector Deposits: $50 Billion

── Aave: $24.9B (49.8%)

── Morpho: $9.6B (19.2%)

── Spark: $6.8B (13.6%)

── Others: $8.7B (17.4%)

Liquidity is explicitly favoring architectures that offer proven smart-contract security, flawless liquidation execution under high volatility, and modular risk parameters.

3. Competitive Landscape: Profiles of the Dominant Models

The lending sector is now driven by three distinct business models, each scaling through a different competitive edge.

Aave: The Institutional Liquidity Vault

Aave functions as the systemically vital reserve bank of Web3. Despite experiencing a cyclical drop in TVL to $24.9 billion, it expanded its active loan book (+6.2%) and pushed its sector deposit market share to a dominant 49.8%.

- Core Driver: Sovereign institutional trust. Large funds, treasury managers, and whales prioritize Aave’s multi-year battle-tested security over higher yields elsewhere. Generating $900.7 million in annualized fees, Aave captures 64.7% of total sector fees, solidifying its position as the primary credit ledger.

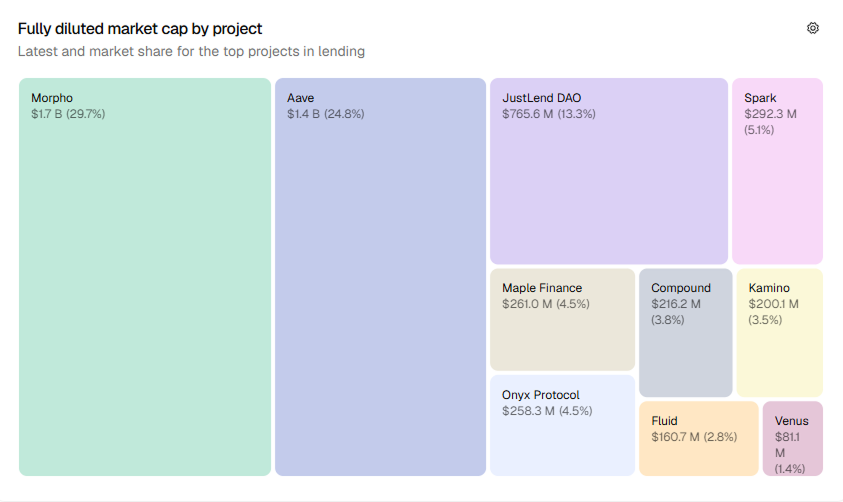

Morpho: The Modular Efficiency Challenger

Morpho is the breakout fintech innovator of the year, expanding its TVL by +73.8% and active loans by +116.1% amidst a broader market drawdown.

- Core Driver: Peer-to-peer optimization and modular risk. Instead of pooling all system assets into a singular, interconnected liquidity pool (the traditional Aave model), Morpho isolates risk into specific asset pairs. This prevents a single asset exploit from compromising the entire platform and optimizes capital efficiency, passing superior borrowing and lending rates back to consumers.

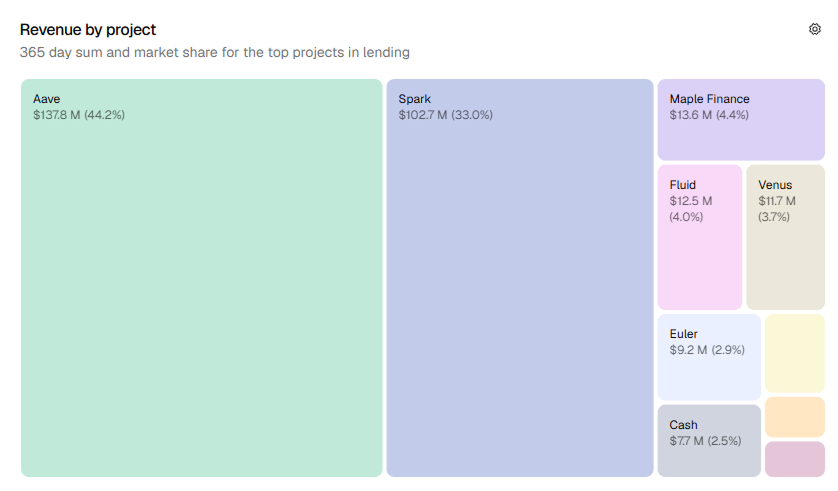

Spark: The High-Yield Monetization Engine

Spark boasts the highest capital-to-profit conversion efficiency in the industry. Operating on a modest 13.6% market share ($6.8B TVL), it successfully converts that liquidity into 33% of the entire lending sector’s net income ($102.7M).

- Core Driver: Deep architectural synergy with the Sky (formerly MakerDAO) ecosystem and its native stablecoins, coupled with exceptional user acquisition. Spark’s active user footprint (DAU) surged by +273%, capturing high-velocity retail and algorithmic traffic.

4. Technological Infrastructure: Where the Capital Resides

The 2026 correction has formalized a functional division of labor across public blockspace: Ethereum acts as the global settlement ledger, while Layer-2 networks and specialized Layer-1 networks host execution.

- Ethereum ($58B TVL / 49%): Its ecosystem dominance slipped below 50% for the first time. Ethereum has cemented its status as a premium security vault. Whale entities hold base liquidity here but settle high-frequency actions elsewhere due to gas fee dynamics.

- Solana ($22B TVL / 19%): Driven heavily by DePIN (Decentralized Physical Infrastructure Networks) demand, Solana’s credit growth is increasingly bound to real-world infrastructure rather than pure speculative velocity.

- Base ($14B TVL / 12%): Acting as the fastest-growing L2, the Coinbase-backed network serves as the primary gateway for corporate and fiat-to-crypto capital on-ramping.

Strategic Outlook

The structural correction of Q1 2026 has brought much-needed maturity to decentralized finance. The lending ecosystem has verified its capacity to autonomously contract, self-liquidate under immense stress without bad debt cascades, and sustain massive fee generation without state bailouts.

Moving deeper into 2026, market share will be won on three specific fronts: Depth of Liquidity (Aave), Modular Efficiency (Morpho), and Productive Monetization (Spark).

The Great DeFi Realignment was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.