$600 Billion Spent. $20 Billion Earned. Do the Math.

The Internet Changed the World — But Cisco Still Crashed: $600 Billion Reasons to Stay Clear-Eyed About the AI Boom

The technology is real. The revolution is real. That doesn’t mean the market is pricing it correctly.

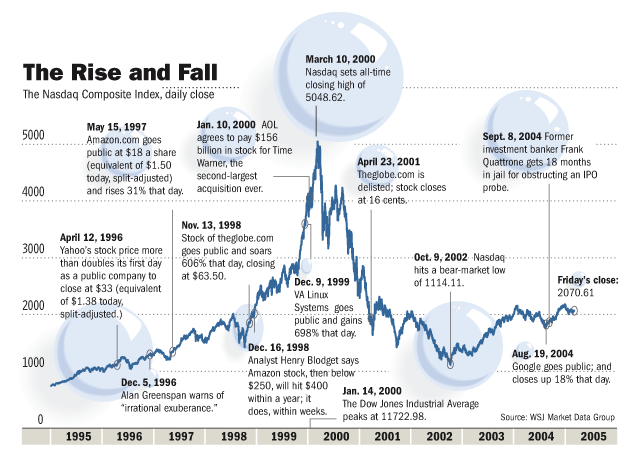

If you had bought Cisco at its peak in March 2000, you’d still be waiting — more than 25 years later — to break even. The Nasdaq had surged roughly 600% between 1995 and 2000. Then it gave all of it back in two years, down 78%. The technology itself survived. The investors didn’t always.

That history feels uncomfortably familiar today. Ray Dalio has warned that the current AI investment climate resembles the dot-com era. Even Sam Altman, OpenAI’s CEO, has publicly acknowledged that “bubble” doesn’t feel entirely wrong. When the man building the thing admits the froth might be real, that’s worth pausing on.

The uncomfortable question: Why do revolutionary technologies so often destroy the wealth of the people who bet on them earliest?

Three Parallels Between 1999 and Now

1. The market prices the perfect future — immediately.

In the late 1990s, everyone understood the internet was a civilizational shift. Correct. But the market priced in a flawless path to monetization for companies that wouldn’t generate profits for a decade. The same dynamic is playing out with AI. Markets always overshoot when a real revolution appears. The technology survives. The valuation survives less reliably.

2. Infinite infrastructure, manufactured demand.

During the dot-com boom, WorldCom and others laid fiber-optic cable as if demand would grow forever. It didn’t. The infrastructure glut triggered a cascade of bankruptcies. Today, big tech companies are spending over $200 billion annually on data centers and chips. Corporate FOMO — not demonstrated customer demand — is driving the capital allocation.

3. Circular money and the return of vendor financing.

Lucent Technologies collapsed partly because it lent money to cash-poor startups, who then used those loans to buy Lucent’s equipment. Revenue looked great — until the startups went under. Today, chip manufacturers are investing in AI companies like OpenAI, which then use that capital to purchase chips from those same manufacturers. Neo-cloud companies are borrowing against their GPU assets to lever up into more hardware. The circularity is real. It’s a structural fragility that didn’t exist three years ago.

Capacity Bubble, Not a Valuation Bubble

Here’s where precision matters, because the lazy version of this argument gets it wrong.

Nvidia is not Cisco. In 2000, Cisco traded at 200x earnings — speculation dressed as valuation. Nvidia today trades at roughly 38x forward earnings, with net margins above 50% and quarterly cash flows that dwarf what Cisco ever produced. Its customers are Apple, Google, Microsoft, and Meta. Nvidia is genuinely one of the strongest companies in the world.

The risk isn’t the stock. It’s something more structural: a Capacity Bubble, where the rate of infrastructure buildout is dramatically outpacing the rate at which end-user applications generate revenue to justify it. The stock isn’t fake. The utility of all that infrastructure, at the scale it’s being built, remains unproven.

Three Walls the Market Is Pretending Don’t Exist

Wall #1: The $600 Billion Revenue Question.

Sequoia Capital’s David Cahn published an analysis in 2024 with a simple methodology: take Nvidia’s data center revenue run-rate, double it to reflect total data center costs, and calculate the end-user revenue needed to justify that build-out. The answer is roughly $600 billion annually — just to break even. Current reality: OpenAI, the most successful AI company in the world, was running at around a $20 billion annual revenue run-rate, with over 90% of users on the free tier. Goldman Sachs called it plainly: “Too much spend, too little benefit.”

Wall #2: The Physical Grid.

Code is infinitely replicable. Electricity is not. The average time to connect a large data center to the power grid is four to ten years. No amount of capital buys past a decade-long permitting and construction queue. The chips are being manufactured. The buildings are rising. The power to run them at scale will take years to arrive.

Wall #3: The End of Free Data.

AI models were built on an implicit assumption: that the internet’s text, images, and media were free inputs. That assumption is now being legally dismantled. The New York Times versus OpenAI lawsuit is the most visible example, but one of dozens. The era of zero-cost training data is ending. When AI companies must license the content that powers their models, the “near-zero marginal cost” economics that justified much of the sector’s valuation breaks down.

What Comes After the Correction

I’m not predicting doom. AI is a structural shift of the first order. The question has never been “is this real?” — it’s “who captures the value, and when?”

After the dot-com crash, hundreds of companies with sky-high valuations disappeared. But Amazon, which fell 95% from its peak, became the most important retail and cloud infrastructure company in the world. Google built one of history’s most profitable businesses on the infrastructure that went bankrupt. The bubble’s collapse didn’t end the revolution. It cleared the noise.

Three things I think the next cycle rewards:

Avoid FOMO-driven infrastructure bets. The buildout is real, but you’re buying into a known capacity bubble at a price that assumes perfect execution.

Watch the application layer. The AI companies that matter in 2030 aren’t building the largest models — they’re solving specific, expensive business problems with measurable cost savings. Boring, specific, relentlessly useful.

Efficiency over scale. When energy is constrained and data is expensive, the advantage goes to companies doing more with less. Specialized models in narrow domains will outcompete expensive general-purpose behemoths.

The technology is real. The revolution will happen. But disruption doesn’t care about your entry price.

The AI Trap was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.