Member-only story

The 7% Floor: How a Corporate Finance Anomaly Reveals Tradeable Patterns in the DAX40

Javier Santiago Gastón de Iriarte Cabrera16 min read·Just now

Javier Santiago Gastón de Iriarte Cabrera16 min read·Just now--

A 2026 academic paper proves that DAX40 companies kept their cost of capital stubbornly high while interest rates collapsed to zero. Here is what that means for traders — and a complete MT5 Expert Advisor built around the finding.

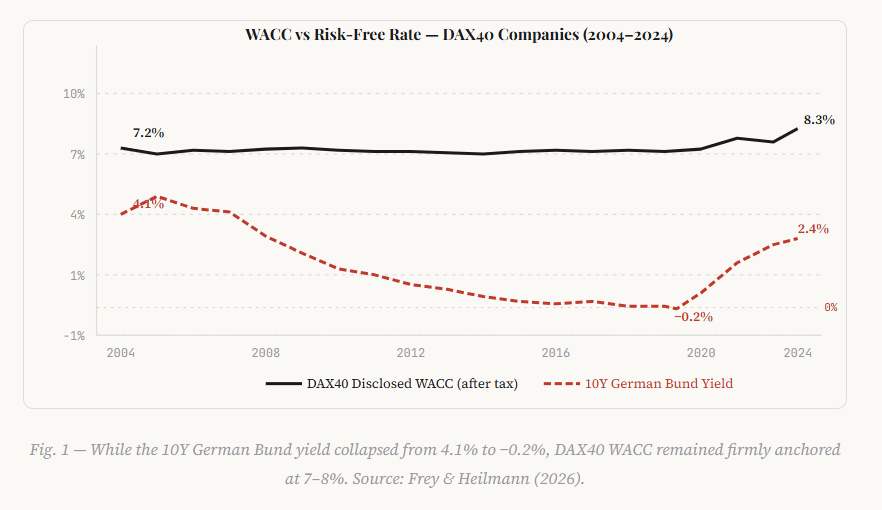

Based on: Frey & Heilmann (2026) · JRFM · DOI: 10.3390/jrfm19050326 | EA: WACC_Persistence_EA.mq5

The Anomaly That Shouldn’t Exist

Between 2004 and 2021, the yield on a 10-year German government bond fell from 4.1% to −0.2%. Basic financial theory — the kind taught in every MBA program — says that the cost of capital should follow. If the risk-free rate falls by 4 percentage points, so should the hurdle rates companies use to approve investments.

It didn’t happen. Not even close.

Across the DAX40 — Germany’s forty largest listed companies — the disclosed Weighted Average Cost of Capital (WACC) remained anchored between 7% and 8% throughout the entire period. Rates went negative. The WACC didn’t flinch.

“Shareholders say: I want my 8–9%. I don’t care what the risk-free rate is.”

— Senior Investor Relations Manager, DAX40 (Interview 3)

A 2026 paper by Simon Frey and Harro Heilmann at Hochschule Aalen set out to explain this. Part I ruled out every quantitative explanation: beta didn’t rise, market volatility didn’t rise significantly, earnings…