Tax Basics: Buying Physical Gold with Crypto in the United States

--

Paying for gold with Bitcoin or Ethereum feels simple — click checkout, send crypto, receive metal. But in the eyes of the IRS, something more complex is happening: you’re disposing of one capital asset and acquiring another. That disposal has tax consequences, and every crypto-native precious metals buyer in the U.S. should understand the basics.

This article is a plain-English overview, not tax advice. Always consult a qualified tax professional for your specific situation.

The Core Concept: Crypto Is Property

The IRS treats cryptocurrency as property, not currency. That means every time you spend crypto — whether for coffee, a car, or a gold coin — you’re executing a taxable disposal of property at fair market value.

In practice, this means:

- If your crypto has appreciated since you acquired it, the gain is taxable

- If it has depreciated, the loss may be deductible (subject to rules)

- The transaction is reportable even if no fiat dollars ever moved

The gold you receive is not taxable on receipt — you simply become the owner of new property with a cost basis equal to the fair market value of the crypto at the time of payment.

Long-Term vs. Short-Term

The holding period of your crypto before disposal matters:

- Held for one year or less: short-term capital gain, taxed as ordinary income

- Held for more than one year: long-term capital gain, taxed at preferential rates (0%, 15%, or 20% depending on income)

If you’re sitting on appreciated Bitcoin from several years ago, spending it on gold triggers long-term gains — which are generally taxed more favorably than short-term gains, but still taxed.

A Simple Example

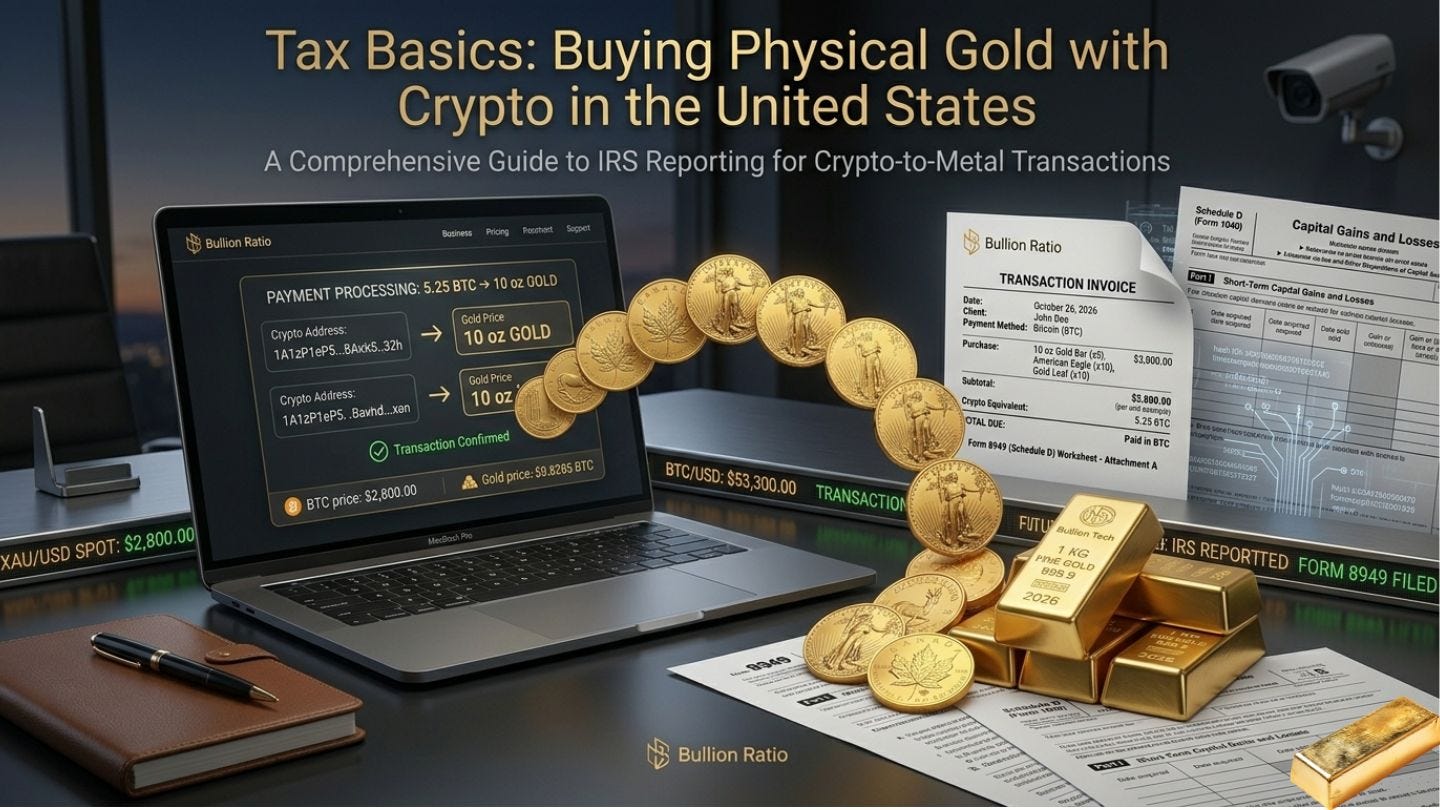

Suppose you bought 0.5 BTC for $15,000 in early 2022. In 2026, when BTC is at $80,000, you use that 0.5 BTC ($40,000) to buy a 16-ounce gold purchase.

The tax picture:

- Your cost basis in the BTC was $15,000

- You disposed of it at a fair market value of $40,000

- You have a long-term capital gain of $25,000

- Your new cost basis in the gold is $40,000

The gain is reportable on Form 8949 and Schedule D in the year of disposal. Future sales of the gold will be measured against the $40,000 cost basis.

What About Losses?

If your crypto has decreased in value since you acquired it, spending it on gold can actually generate a deductible capital loss — subject to the same long-term / short-term rules. This is one reason some investors prefer to spend their lower-basis lots first and save appreciated lots for later. Tax lot selection matters.

Stablecoins and Taxes

Stablecoins like USDC and Tether are also treated as property for tax purposes, but because their value is pegged to the dollar, gains and losses are usually near zero. Spending stablecoins on gold typically generates minimal taxable events, which is one reason some investors prefer them for metals purchases.

Privacy Coins and Reporting Obligations

Using Monero or other privacy coins to buy gold does not exempt you from U.S. tax reporting obligations. Your legal duty to report capital gains is the same regardless of whether the transaction is on a transparent chain or a private one. The privacy feature protects you from third parties, not from the IRS.

This is a critical distinction. Privacy is a feature. Tax compliance is a legal obligation. They’re not mutually exclusive, but they’re not the same thing either.

Gold’s Tax Treatment

Physical gold held for investment is treated by the IRS as a “collectible.” This means:

- Long-term capital gains on physical gold are taxed at up to 28% — higher than the 20% maximum on stocks or crypto

- Short-term gains are taxed as ordinary income, same as other assets

- Losses are deductible subject to standard rules

This higher collectible rate applies when you eventually sell the gold for gain — not when you buy it.

Record Keeping

The single most important thing a crypto-to-gold buyer can do is keep clean records. For every transaction:

- Date of crypto acquisition (original purchase)

- Cost basis (what you paid for it)

- Date of disposal (when you bought gold)

- Fair market value at disposal

- Description and quantity of gold received

- Dealer and purchase invoice

Modern crypto tax software (CoinTracker, Koinly, TokenTax, etc.) can automate much of this if your wallets are connected.

Buying Smart

Veldt Gold issues clear invoices for every crypto-funded order — which makes tax record-keeping straightforward. Every order also ships with free insured delivery, so your transaction record and your physical gold arrive in a single, documented package.

The Bottom Line

Buying physical gold with cryptocurrency is a completely legal, increasingly common strategy — but it’s not tax-free. Every crypto disposal is a reportable event in the United States, whether you trade it for dollars, gold, or anything else of value.

The good news: the rules are clear, the paperwork is manageable, and crypto-native buyers who understand the basics can execute this strategy with confidence. When in doubt, talk to a tax professional who understands both cryptocurrency and collectibles taxation.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or tax advice. Consult a qualified professional before making investment decisions.