Shared vs Dedicated Merchant Accounts: What’s the Real Difference

--

Introduction: The Strategic Importance of Shared vs Dedicated Merchant Accounts: What’s the Real Difference

In the modern digital economy, particularly for sectors categorized as ‘high-risk’ — such as iGaming, Forex, Cryptocurrency, IPTV, and Adult entertainment — the payment processing architecture is not just a utility; it is the heartbeat of the enterprise. For a platform like boxchrge.com, the goal is to provide transparency and resilience in a landscape often clouded by complexity. When we discuss Shared vs Dedicated Merchant Accounts: What’s the Real Difference, we are looking at the fundamental mechanics that determine whether a business can scale globally or if it will be stifled by sudden account terminations and frozen funds.

The High-Risk Landscape: Forex, Gaming, and Beyond

Merchants operating in the offshore space face a unique set of hurdles. Whether it is a Forex broker dealing with cross-border currency fluctuations or a gaming platform managing high-volume, low-ticket transactions, the pressure from Card Schemes (Visa and Mastercard) is relentless. Banks are increasingly risk-averse, meaning that a standard ‘one-size-fits-all’ approach to merchant accounts is no longer viable. Businesses dealing in peptides or IPTV must be even more vigilant, as regulatory shifts can happen overnight. The choice of processing infrastructure becomes a hedge against these external volatilities.

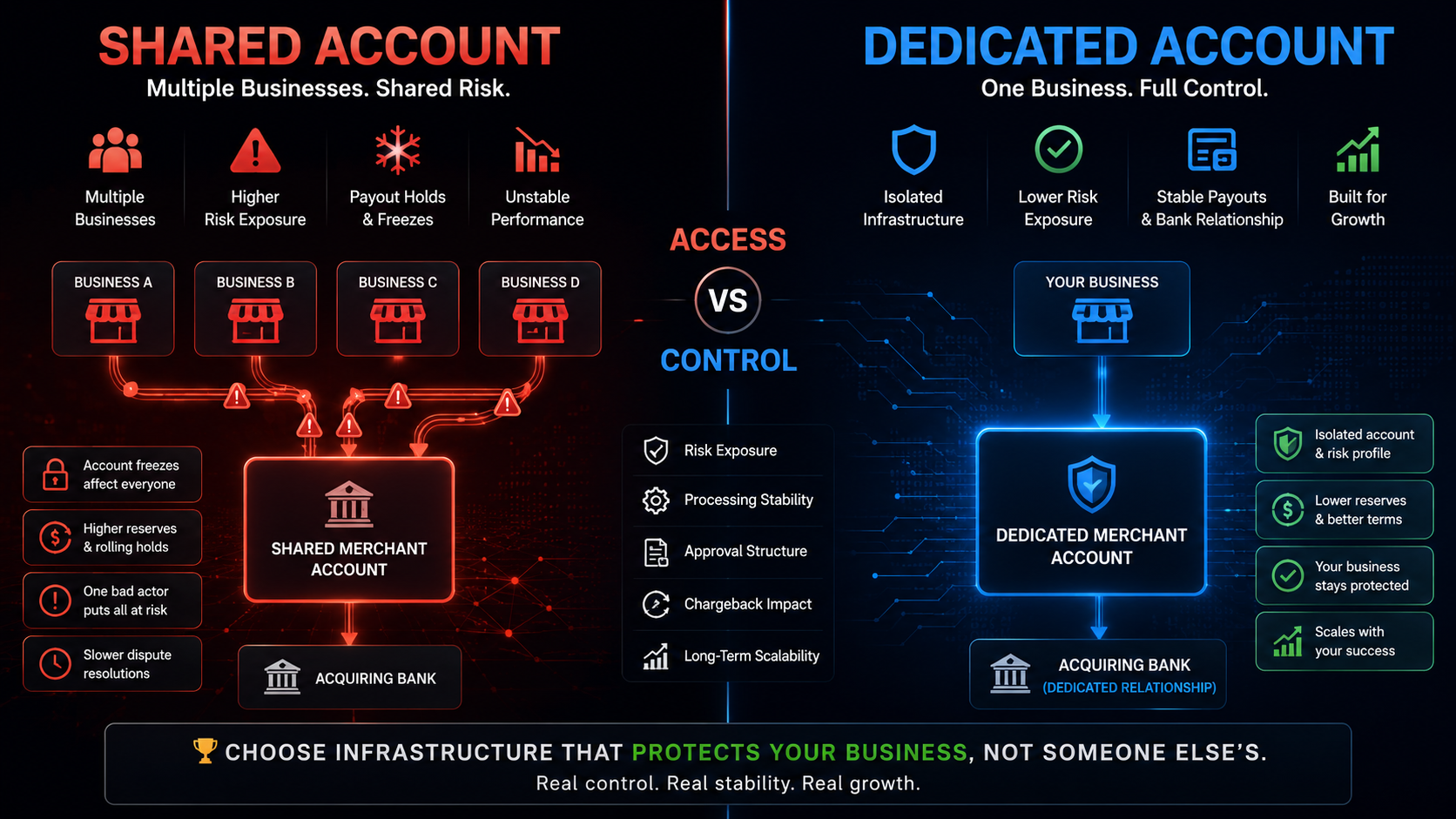

Analyzing the Mechanics of Shared vs Dedicated Merchant Accounts: What’s the Real Difference

A shared merchant account functions like a communal living space. It is easier to get into, but you have no control over your neighbors. An aggregator takes your volume and mixes it with a thousand other merchants. Conversely, a dedicated account is your own private estate. Every transaction is yours, and your reputation is the only one that matters. This distinction is vital when high-risk merchants seek long-term sustainability.

Technical Integration and Security Protocols

Implementing a robust payment structure requires a deep understanding of API integrations, PCI DSS compliance, and tokenization. For high-risk merchants, security is not just about preventing theft; it is about proving to the acquirer that you have a professional-grade risk management system in place. We examine the role of 3D Secure 2.0 and how it can be leveraged to shift liability while maintaining a smooth user experience for the customer.

Conclusion: The Path Forward with boxchrge.com