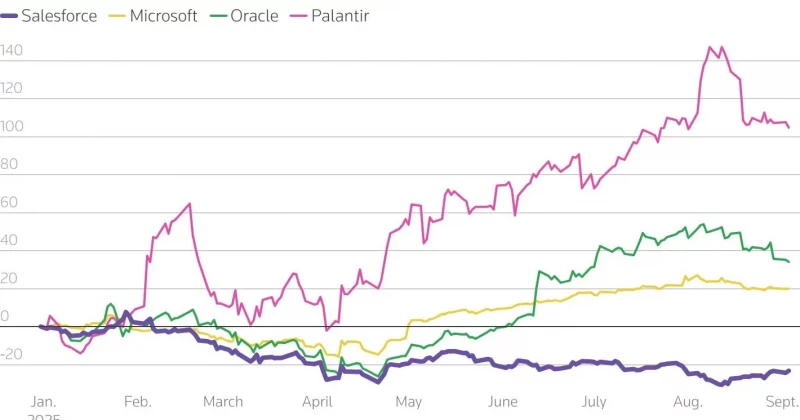

Salesforce shares sink on soft revenue outlook amid AI concerns

CRM stock dropped nearly 8% after the enterprise software giant delivered a disappointing revenue forecast, raising fresh questions about whether its AI bets are paying off.

Share

Add us on Google by Editorial Team May. 27, 2026Salesforce just reminded Wall Street that spending billions on AI doesn’t automatically translate into revenue growth. Shares of the enterprise software giant fell nearly 8% on September 4, 2025, after the company issued a soft revenue outlook for its third quarter of fiscal year 2026.

What happened and why investors bailed

The nearly 8% single-session decline came during the aftermath of Salesforce’s earnings release, where the revenue guidance fell short of what analysts were expecting.

Salesforce has been aggressively marketing its AI capabilities, particularly through its Agentforce platform for autonomous agents and its Einstein AI suite. The pitch to customers is compelling on paper: let AI handle more of the repetitive CRM work so your sales team can focus on closing deals.

AdvertisementBut investors are increasingly asking a pointed question. If autonomous AI agents can do much of what Salesforce’s traditional software does, why would enterprises keep paying premium subscription fees for legacy platforms?

The bigger picture: macro headwinds meet AI skepticism

This wasn’t Salesforce’s first rough encounter with Wall Street in 2025. Back in May, the company released its Q1 FY25 results to a decidedly mixed reception. Analysts noted that while the company beat some expectations, the broader macroeconomic environment was creating headwinds that made sustained growth harder to achieve.

By February 25, 2026, when Salesforce published its Q4 FY26 results, the company attempted to reset the narrative. Management projected FY27 revenue between $45.8 billion and $46.2 billion, representing a 10-11% annual increase. Part of that anticipated growth was attributed to contributions from Informatica, along with hopes for an organic recovery in the second half of FY27.

What this means for investors

Salesforce’s Agentforce and Einstein platforms represent genuine technological bets, but the monetization timeline remains unclear. The company is essentially asking shareholders to be patient while it builds out AI capabilities that may take several quarters to show up meaningfully in the top line.

For investors tracking this space, the key metrics to watch in coming quarters are Agentforce adoption rates, net revenue retention, and whether that projected $45.8-$46.2 billion FY27 revenue range holds up as guidance gets updated. The 10-11% growth target is respectable but not spectacular for a company commanding enterprise software valuations.

Disclosure: This article was edited by Editorial Team. For more information on how we create and review content, see our Editorial Policy.