RWA Built the Long Half. Where Is the Other Half?

--

Imagine a stock market where people can buy, hold, and sell, but no one can short.

It would still look like a market.

There would be tickers, wallets, funds, research notes, dashboards, fees, custody, compliance, and institutional decks.

But one function would be missing:

the ability to express "this is overvalued" with capital.

That missing function changes everything.

Without it, negative information arrives late. Optimistic narratives face less resistance. Prices may move, but they move inside a market where one side of belief is easier to finance than the other.

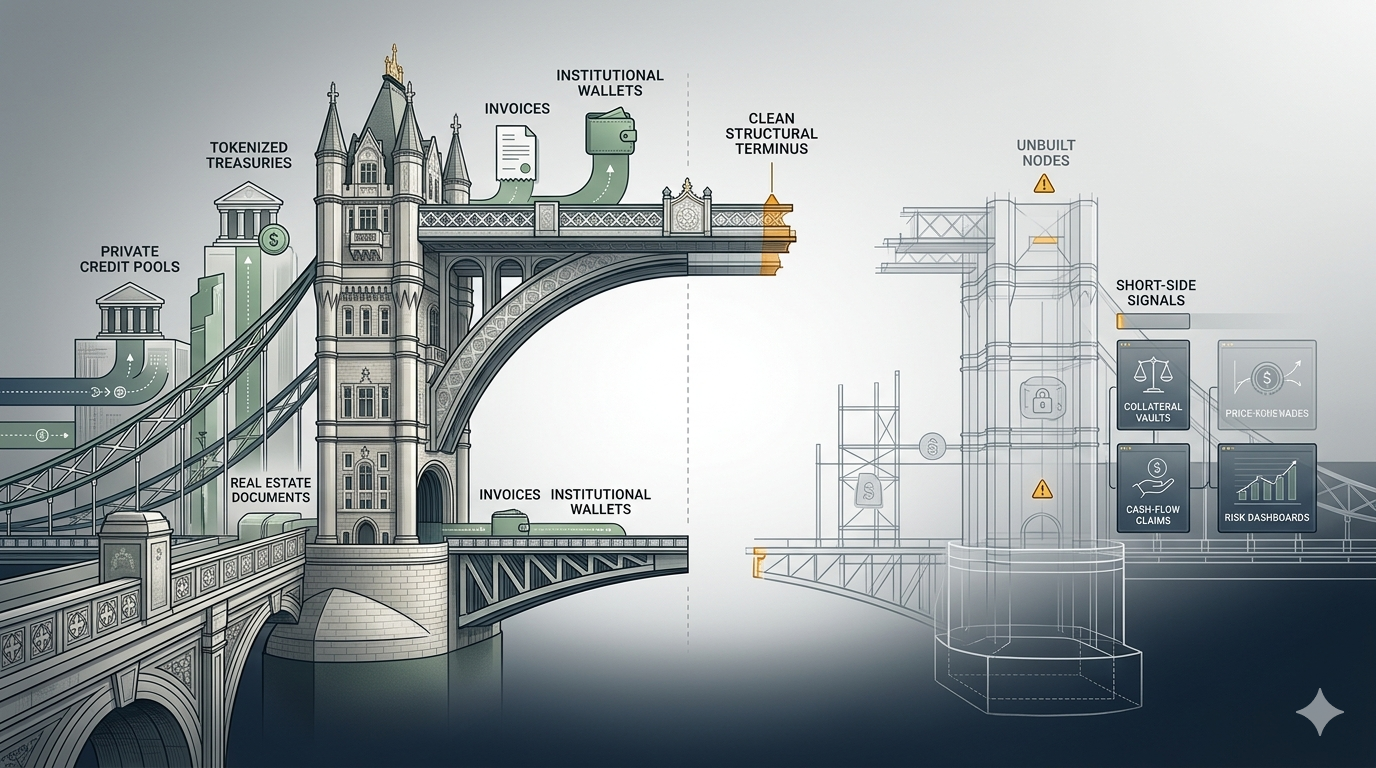

That is where the RWA market is today.

Not because RWA builders are doing something wrong.

Because they have been building the first half:

the long side.

Tokenized Treasuries, private credit, real-estate claims, invoices, funds, and other real-world assets are being brought on-chain. The infrastructure is real. The demand is real. The regulatory work is real.

But the other half of the market is still mostly absent.

Who gets to say no?

1. What RWA Has Already Built

The RWA sector has grown from a niche experiment into one of the most concrete parts of crypto finance.

The exact number depends on methodology. Some trackers include only non-stablecoin tokenized assets. Some include private credit. Some count tokenized treasuries separately. Stablecoins alone would dwarf many RWA categories, so they should not be casually mixed into the same number.

But the direction is clear.

Public trackers such as RWA.xyz and industry reports show tens of billions of dollars of real-world assets represented on-chain by 2025-2026. Tokenized U.S. Treasury products became one of the fastest-growing categories, with products such as BlackRock's BUIDL and Franklin Templeton's BENJI helping normalize institutional tokenized cash-management products. Private credit and asset-backed lending protocols such as Centrifuge, Maple Finance, and Goldfinch built earlier versions of on-chain private-credit infrastructure.

Different products have different legal structures.

Some are fund interests.

Some are notes.

Some are tokenized money-market or Treasury exposures.

Some are lending pools.

Some are securitized or asset-backed structures.

But their common economic direction is similar:

bring the long exposure on-chain.

The holder buys a token or participates in a pool.

The token gives access to yield, repayment, NAV, or asset-backed income.

The protocol or issuer handles onboarding, reporting, compliance, servicing, custody, and payments.

This solves real problems.

It can reduce operational friction.

It can make settlement faster.

It can create more transparent records of ownership and transfers.

It can make some private-market exposures easier to access for eligible investors.

It can put payment histories and pool states into a more inspectable format than traditional PDFs and email attachments.

These are not fake benefits.

RWA is not a narrative only.

It is real financial plumbing.

But after that plumbing is built, a deeper question remains:

Who verifies the price?

Not the payment.

Not the token balance.

The price.

2. Why RWA Is Structurally Long-Biased

This is not an accusation.

It is a business-model observation.

Most RWA protocols and issuers are built to help asset owners, borrowers, funds, or managers access capital. Their users want financing, distribution, lower friction, broader investor access, or better settlement infrastructure.

That means the first customer is usually the long side.

Borrowers want lenders.

Fund managers want allocators.

Treasury-product issuers want AUM.

Asset owners want liquidity.

RWA protocols are therefore naturally optimized for origination, onboarding, reporting, custody, compliance, and distribution.

They are not naturally optimized for adversarial negative expression.

A protocol helping a borrower raise capital is unlikely to make "short this borrower's cash flows" a central product feature.

A tokenized Treasury issuer paid on AUM is unlikely to design around shorting its own product.

A private-credit marketplace trying to attract originators is unlikely to lead its pitch with a tool that makes originators feel attacked.

This does not mean these protocols are dishonest.

It means they are doing what their position in the stack asks them to do.

They are issuance and distribution infrastructure.

Shorting is not issuance infrastructure.

It is price-discovery infrastructure.

Those layers can cooperate, but they are not the same layer.

This distinction matters because transparency alone is not enough.

RWA can make reported asset states more visible.

But visibility over reported states is not the same as adversarial price discovery.

If the only available market action is to buy, hold, redeem, or sell an existing long position, then negative information has fewer ways to become a price before distress arrives.

The market may be on-chain.

But the disagreement may still be off-chain.

3. Hipgnosis Was a Preview, Not a Perfect Analogy

The copyright market has already shown what happens when cash-flow assets become a one-sided story.

Hipgnosis Songs Fund was a listed vehicle, not an RWA protocol. It had a public share price. Investors could sell the stock, and sophisticated investors may have been able to short the equity. So it is not a perfect analogy.

But it is still useful.

Hipgnosis held music catalogs. The assets produced real royalties. The investment thesis was plausible: streaming growth, durable songs, uncorrelated cash flows, sync upside, cultural longevity.

Then rates rose. Governance questions increased. Valuation assumptions came under pressure. In March 2024, the fund disclosed work by Shot Tower Capital indicating a 26.3% reduction versus prior operative NAV.

The issue was not that music royalties were fake.

They were real.

The issue was that valuing long-duration private cash flows is assumption-heavy.

Discount rates matter.

Growth assumptions matter.

Decay curves matter.

Fees, leverage, administration, and governance matter.

Hipgnosis at least had a public equity wrapper. Its stock price could fall. The market had a blunt way to say no.

Many private RWA-style assets will not have even that.

They may have a token balance.

They may have reporting.

They may have payments.

They may have redemptions, sometimes.

But they may not have a clean instrument for shorting the cash-flow expectation itself.

That is the gap.

On-chain representation makes the asset easier to observe.

It does not automatically create a negative price signal.

4. What CF Token Is, and Is Not

CF Token is not a competitor to RWA protocols.

It does not need to originate loans.

It does not need to tokenize the underlying asset.

It does not need to replace Centrifuge, Maple, Ondo, BlackRock BUIDL, Franklin Templeton, or any other RWA issuer.

It is not trying to take the borrower relationship.

It is not trying to become the asset manager.

It is not the long-side distribution layer.

CF Token is better understood as a price-discovery layer for cash-flow expectations.

RWA protocols represent and distribute long exposure.

CF Token lets someone take the other side of a specified cash-flow claim by posting collateral and issuing a tradable claim that pays according to verified realized cash-flow states.

The relationship is vertical, not horizontal:

CF Token layer:

negative cash-flow expectations, hedging, price discovery

RWA asset layer:

asset onboarding, cash-flow reporting, compliance, distribution

Base infrastructure:

chains, custody, identity, oracle rails, settlementThe CF Token layer depends on the RWA layer.

It needs reference assets, disclosures, evidence trails, identity, legal wrappers, and cash-flow reporting. The better RWA infrastructure becomes, the more feasible a cash-flow shorting layer becomes.

That is why CF Token should not be framed as anti-RWA.

It is pro-complete-market.

5. What the Short Side Gives RWA

From the RWA perspective, a cash-flow shorting layer may sound threatening.

It should not.

It can make the market more credible.

Independent valuation pressure

If a private-credit pool has a CF Token referencing its coupon performance, and that token trades at a discount to face value, the signal is useful.

It does not prove the pool is bad.

It says the market is pricing weaker cash-flow performance than the issuer's story suggests.

That signal helps investors ask better questions.

It helps protocols monitor risk.

It helps allocators compare reported performance with market-implied expectations.

Without that layer, RWA markets may have reporting but little adversarial valuation.

More comfortable institutional allocation

This is the counterintuitive part:

a shorting mechanism can increase long capital.

Institutions often avoid exposures they cannot hedge, exit, or stress-test. If a fund can buy an RWA asset and also hedge part of the cash-flow risk, the long allocation may become easier to approve.

The hedge does not need to be perfect.

Even partial protection can matter for risk committees.

Traditional markets already understand this. Futures, swaps, CDS, options, and short-selling mechanisms do not only exist because people want to bet against assets. They exist because institutions hold assets and need tools to manage risk.

RWA markets will face the same demand as they mature.

No hedge means smaller balance sheets.

Some hedge can mean larger, more durable participation.

Better information production

When negative information cannot be traded, it often stays private.

A credit analyst sees deterioration but cannot act.

An LP distrusts marks but cannot hedge.

An industry insider knows cash flows are weaker than reported but has no instrument.

A market with no short side wastes that information.

A CF Token layer gives negative information a price channel.

Not every short will be right.

But the existence of shorts means someone has a reason to search for the weak assumption before the crisis.

That search improves the market.

6. Why RWA Protocols May Not Build This Themselves

If the short side benefits the market, why will RWA protocols not build it directly?

There are good reasons.

Customer conflict

Many RWA protocols depend on asset originators, borrowers, managers, and issuers.

Those parties want capital.