Price, Risk, and Structure in Commodity Futures

--

Currency Markets and Agricultural Futures

A quantitative study of exchange rates, export competitiveness, and corn futures pricing

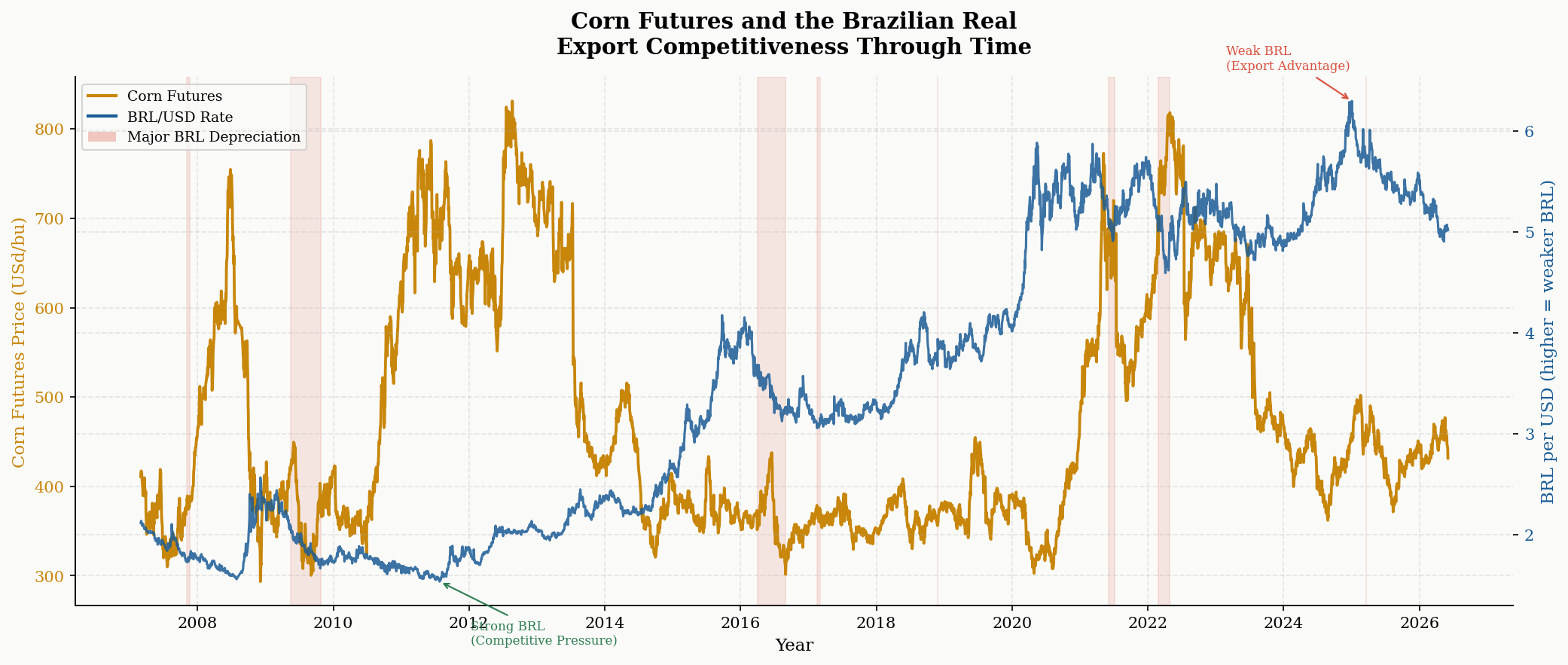

Brazil accounts for a significant share of global agricultural exports.

As a result, movements in the Brazilian Real can influence export competitiveness, production incentives, and ultimately the supply reaching international commodity markets.

This inspired my thesis: Do currency markets contain information about future agricultural futures returns?

To investigate this, I built a Python model examining the relationship between the Brazilian Real and corn futures.

The analysis focused on:

- long-run price relationships between BRL and corn futures

- lead-lag effects across 30, 60, 90, and 180-day horizons

- corn performance following major currency depreciations

- rolling correlations across different market environments

The underlying hypothesis was straightforward.

A weaker Real improves the competitiveness of Brazilian exports. Increased export competitiveness can influence global supply conditions and potentially affect agricultural futures pricing over subsequent months.

Several observations emerged from the study.

Periods of significant Real depreciation were frequently followed by changes in corn futures performance, although the relationship varied considerably across time.

Lead-lag analysis suggested that currency markets occasionally contained information before it became fully reflected in agricultural futures pricing.

However, the relationship was far from stable.

Rolling correlations showed extended periods where exchange rates and corn futures moved closely together, followed by periods where the relationship weakened or disappeared entirely.

This suggests that currency effects are conditional rather than structural.

Exchange rates matter, but they operate alongside a broader set of market drivers including weather, inventories, trade flows, and global demand conditions.

The results highlight an important feature of commodity markets.

Agricultural futures are not simply pricing crop production. They are also pricing the economics of global trade. Changes in exchange rates alter export competitiveness, influence producer behaviour, and affect how supply reaches international markets.

While currency markets alone do not determine agricultural futures returns, the evidence suggests they provide an additional layer of information about future market conditions.

For commodity traders, understanding that transmission mechanism may be just as important as understanding the crop itself.

Code and analysis available on GitHub.

https://github.com/sidchandra9087/Currency-rate-on-corn-futures