Price, Risk, and Structure in Commodity Futures

Seasonality and Price Formation in Corn Futures

--

Corn futures are directly linked to a predictable physical production cycle. Unlike metals, where supply evolves slowly, agricultural markets follow clear seasonal phases driven by planting, growing conditions, and harvest. From a macroeconomic perspective this reflects a market where supply is time-dependent and highly exposed to exogenous shocks such as weather variability. As a result, futures prices are driven not only by current supply but by forward-looking expectations of production outcomes.

This makes corn an ideal market to study how real-world supply dynamics influence price formation in futures markets.

In this project, I built a Python model to examine whether seasonal production cycles lead to systematic differences in returns, volatility, and price behaviour in corn futures.

Research Question: Do seasonal supply cycles in agriculture create predictable patterns in corn futures prices, and are these effects clearly reflected in market behavior?

Methodology

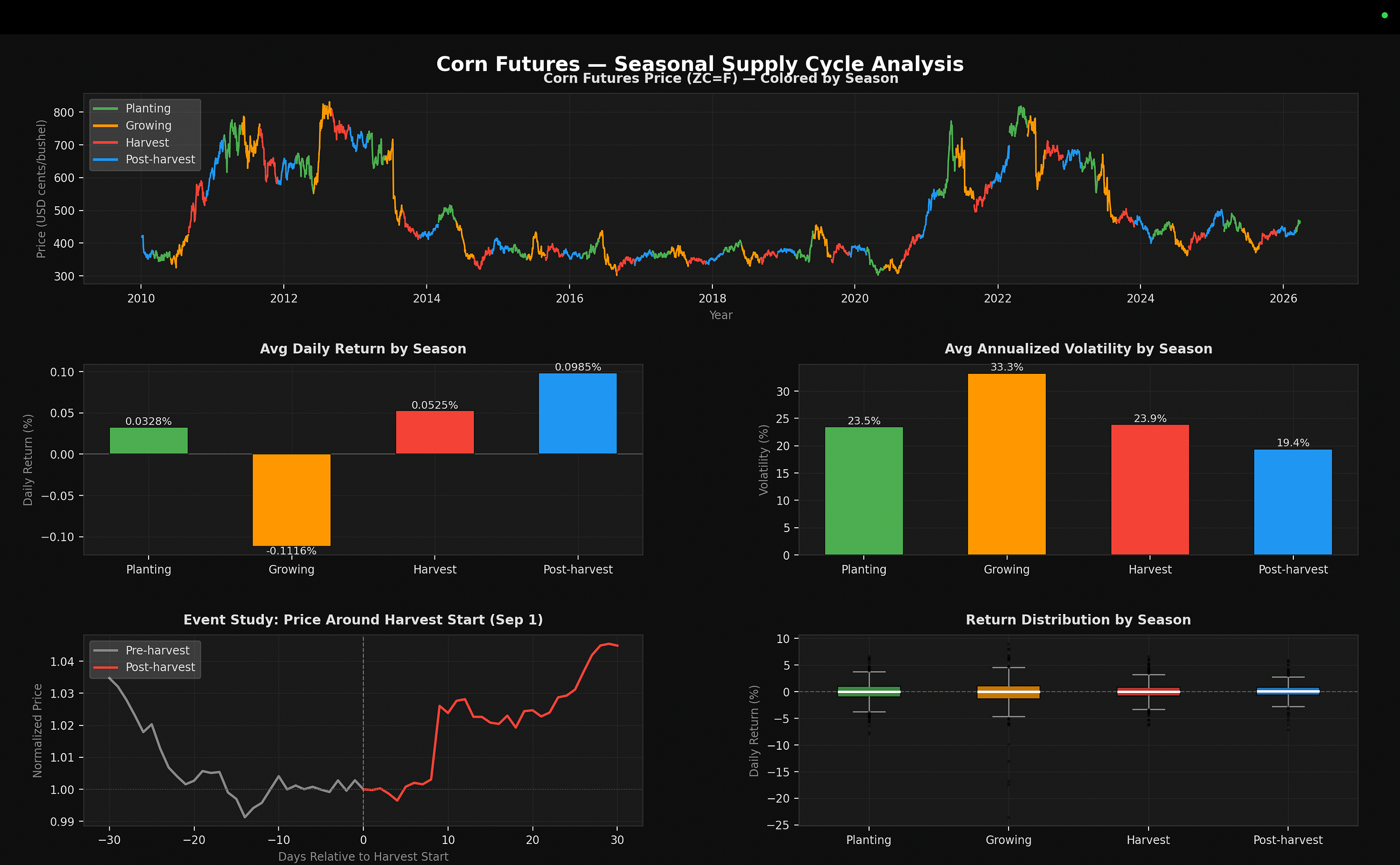

I used daily corn futures data over a multi-year period and divided each year into four distinct phases of the agricultural cycle:

- Planting (March–May)

- Growing (June–August)

- Harvest (September–November)

- Post-harvest (December–February)

Each trading day was assigned to one of these periods. For each season, I computed average returns, volatility, and distribution characteristics. I also analyzed price behavior around the start of harvest to observe how markets respond to the realization of supply. This structure allows the analysis to capture the transition from expectation-driven pricing to realized supply conditions, which is central to how futures markets function.

Results

The results show clear differences across the production cycle.

The growing season exhibits the weakest performance, with negative average returns and the highest volatility. This period corresponds to peak uncertainty, where weather conditions and yield expectations are still unresolved. This period reflects elevated uncertainty, where incomplete information about yields leads to wider price dispersion and increased volatility. In economic terms, this can be interpreted as a phase of high information asymmetry between market participants.

In contrast, the post-harvest period shows the strongest returns and the lowest volatility. Once supply is realized, uncertainty declines and price behavior stabilizes. Once supply is realized, uncertainty declines and prices begin to reflect actual market conditions rather than forecasts. This aligns with the process of price discovery, where markets incorporate new information and move toward equilibrium.

The harvest period itself shows moderate positive returns, suggesting that markets begin adjusting before supply is fully reflected in prices.

Planting season returns are positive but smaller in magnitude, with moderate volatility.

Key Insight

Periods of maximum uncertainty are associated with weaker returns and higher volatility, while periods of supply clarity show stronger and more stable price behavior.

This suggests that risk in agricultural futures is concentrated in the growing phase, while return opportunities tend to emerge after uncertainty is resolved.

My take

The results align with basic economic intuition.

During the growing season, markets price in a wide range of possible outcomes driven by weather and yield variability. This leads to increased volatility and less consistent directional movement. The supply curve is effectively uncertain and highly sensitive to external shocks, particularly weather conditions.

As the harvest approaches and supply becomes observable, uncertainty declines. The market transitions from pricing expectations to pricing realized supply, leading to more stable conditions and improved returns.

This pattern indicates that futures markets do not fully resolve uncertainty during the growing phase and instead adjust gradually as information becomes available. This suggests that risk in agricultural futures is not constant, but concentrated in periods where supply uncertainty is highest.

Conclusion

This study shows that seasonal production cycles play a meaningful role in shaping price behavior in corn futures.

Returns and volatility are not evenly distributed throughout the year. Instead, they follow a structure driven by uncertainty and supply realization.

Understanding this structure provides insight into how agricultural markets process information and highlights the importance of real-world production dynamics in futures pricing.

My code:https://github.com/sidchandra9087/corn-seasonality-futures-analysis/tree/main