Payment Processing for Restricted Industries in 2026: The Definitive Guide for Every High-Risk Vertical

Harry Williams7 min read·1 hour ago

Harry Williams7 min read·1 hour ago--

By Kira Johansson · International Payments & Regulatory Compliance Analyst · April 2026 · 17 min read

There are over 50 business categories that mainstream payment processors classify as “restricted” or “prohibited.” These categories include some of the fastest-growing, most profitable, and most legally unambiguous industries in the global economy. Collectively, they represent hundreds of billions of dollars in annual revenue generated by millions of businesses that are systematically overcharged, underserved, and periodically cut off from the ability to accept credit card payments.

This guide covers every major restricted industry, explains why each faces payment processing challenges, quantifies the costs of traditional high-risk processing for each vertical, and presents the structural alternative that eliminates those costs.

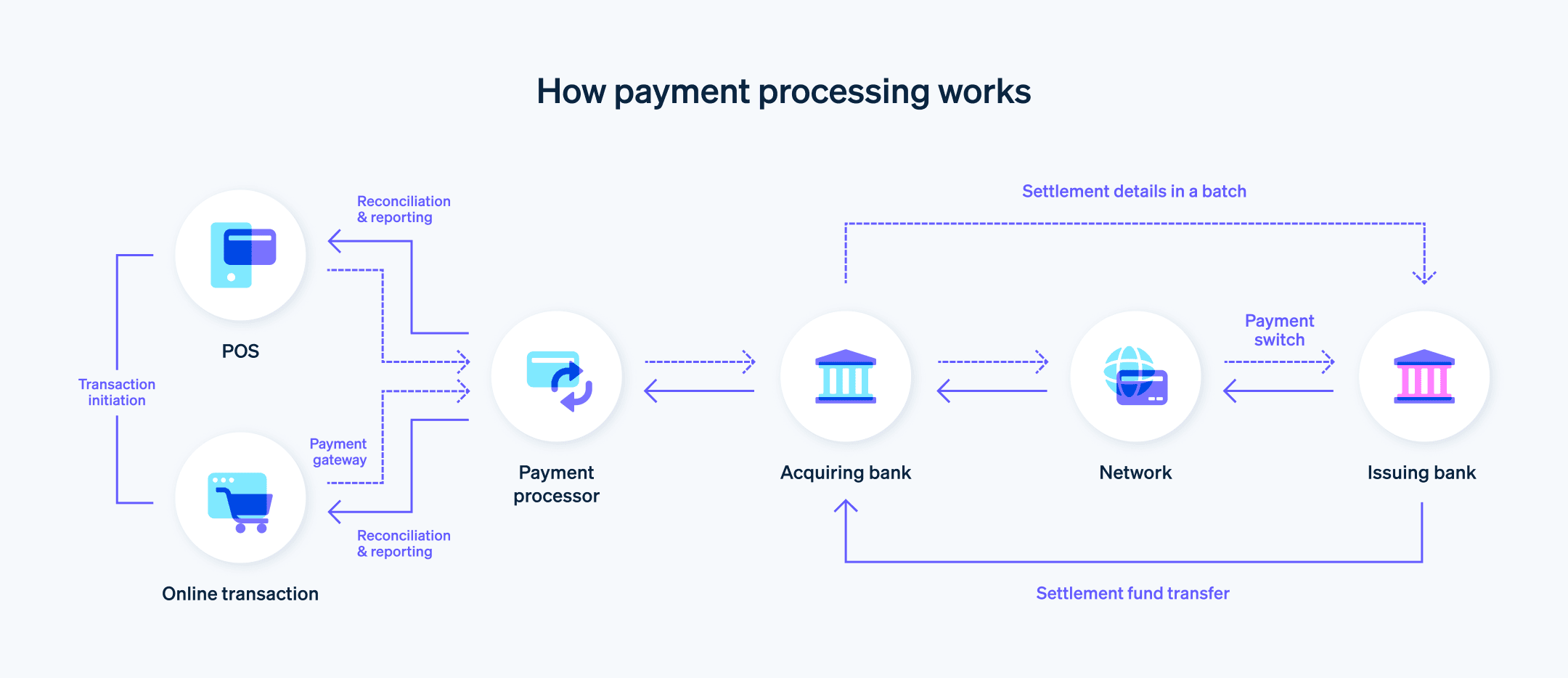

The Universal Problem

Every restricted industry faces the same set of payment processing challenges:

- Mainstream processor rejection. Major processors auto-reject applications from businesses with restricted MCCs.

- Elevated fees. Specialized high-risk processors charge 4–10% — double to triple the rates mainstream merchants pay.

- Rolling reserves. 5–15% of every transaction is withheld for 6–12 months.

- Fund freezes. Processors can freeze your entire balance during “reviews” triggered by chargeback spikes, volume increases, or arbitrary risk reassessments.

- Termination risk. The processor or its acquiring bank can exit your category at any time, leaving you without payment capability.

- Slow settlement. 3–7+ business days vs. 1–2 days for mainstream merchants.

The specifics vary by industry, but the pattern is identical. Let’s examine each vertical.

Industry-by-Industry Breakdown

Peptides and Research Chemicals

Market size: The global peptide therapeutics market is projected to exceed $80 billion by 2028.

Why restricted: Mainstream processors classify peptides alongside controlled pharmaceuticals under MCC codes that trigger automatic rejection. The processor’s compliance team doesn’t distinguish between a GMP-certified research peptide laboratory and an unlicensed pharmacy.

Traditional processing cost: 5–8% transaction fees + 10% rolling reserve. Application takes 2–4 weeks with frequent rejections. Account terminations are common when the acquiring bank periodically “re-evaluates” the category.

Real cost example: A peptide company processing $60,000/month at 6% with 10% reserve pays $3,600/month in fees and has $6,000/month locked in reserve. Annual cost: $43,200 in fees + $6,000/month perpetually withheld.

CBD, Hemp, and Cannabis Accessories

Market size: The global CBD market is projected to reach $47 billion by 2028.

Why restricted: Despite federal legality in the U.S. and legality across the EU, CBD is classified under MCCs that overlap with controlled substances. Processors worry about THC content variance, shifting state regulations, and FDA enforcement actions.

Traditional processing cost: 5–8% + 10% rolling reserve. Many processors require third-party lab certificates for every product SKU, creating ongoing compliance overhead.

Nutraceuticals, Supplements, and Nootropics

Market size: The global dietary supplements market exceeds $170 billion annually.

Why restricted: Health claims, product liability concerns, and overlap with pharmaceutical MCCs. Processors are particularly cautious about weight loss supplements, testosterone boosters, and cognitive enhancers.

Traditional processing cost: 4–7% + 8–10% rolling reserve. Product catalog reviews add 1–2 weeks to onboarding.

Online Gambling and Sports Betting

Market size: Global online gambling revenue exceeds $90 billion annually.

Why restricted: Regulatory complexity (varying legality by jurisdiction), high transaction volumes, elevated chargeback rates in the industry, and reputational sensitivity.

Traditional processing cost: 5–9% + 10–15% rolling reserve. Settlement delays of 5–7+ business days. Processors frequently exit the vertical with minimal notice.

Adult Content

Market size: Estimated $100 billion+ globally.

Why restricted: Visa and Mastercard compliance requirements implemented in 2020–2021 imposed content verification, review, and complaint resolution obligations. Many processors exited entirely rather than implement the required compliance infrastructure.

Traditional processing cost: 7–12% + 10–15% rolling reserve for the processors that remain. Individual creators face even higher barriers — most processors require a registered business entity.

Vaping and E-Cigarettes

Market size: The global e-cigarette market exceeds $30 billion annually.

Why restricted: Regulatory crackdowns (PACT Act, FDA enforcement, state-level flavor bans) caused mass deplatforming in 2019. Card networks pressured acquiring banks to reduce exposure to the category.

Traditional processing cost: 6–10% + 10–15% rolling reserve. Age verification requirements add compliance overhead.

Dating Sites and Matchmaking

Why restricted: Subscription-based billing models generate higher-than-average chargeback rates (customers forget they subscribed or find cancellation difficult). Auto-renewal disputes are common across the dating vertical.

Traditional processing cost: 4–7% + 8–12% rolling reserve. Processors monitor chargeback rates aggressively and terminate accounts that exceed thresholds.

Travel and Booking Services

Why restricted: Future-delivery risk (customer pays now, travels later). If the business fails between payment and delivery, the processor faces liability for all undelivered services. Post-COVID processor anxiety about travel company solvency persists.

Traditional processing cost: 4–6% + 10% rolling reserve. Reserves are often higher for businesses with long delivery timelines (cruises, packaged tours).

Telehealth and Online Pharmacies

Why restricted: Regulatory complexity across jurisdictions. Licensing requirements vary by state/country. Processors worry about unlicensed practice and controlled substance distribution.

Traditional processing cost: 5–8% + 10% rolling reserve. Extensive documentation required including medical/pharmacy licensing.

Firearms Accessories and Tactical Gear

Why restricted: Reputational sensitivity. Even legal accessories (holsters, optics, cleaning kits, tactical clothing) get classified under firearms MCCs that many processors refuse entirely.

Traditional processing cost: 4–7% + 8–10% rolling reserve. Many mainstream processors refuse the category outright regardless of the specific products sold.

Crypto-Adjacent Services

Why restricted: Any business serving the crypto industry — SaaS tools, analytics platforms, educational courses, mining equipment, consulting — gets classified as high-risk by association.

Traditional processing cost: 4–7% + 8–10% rolling reserve. Some processors refuse entirely.

Debt Services and Credit Repair

Why restricted: Industry history of consumer complaints, regulatory actions against bad actors, and high chargeback rates for the category overall.

Traditional processing cost: 5–8% + 10–12% rolling reserve.

The Universal Solution: NexaPay.one

Every industry listed above faces the same structural problem: dependency on processors that classify, judge, and penalize merchants based on their business category. The solution needs to be structural — not a better version of the same broken model, but a different model entirely.

NexaPay is a fiat-to-crypto payment gateway. Customers pay with Visa, Mastercard, Apple Pay, or Google Pay. The merchant receives USDC, USDT, or other cryptocurrency directly to their wallet. The gateway doesn’t classify merchants by industry, doesn’t require KYC, doesn’t impose rolling reserves, doesn’t freeze funds, and charges 1–3% for every merchant regardless of category.

Why NexaPay Works for Every Restricted Industry

No MCC classification = no category-based rejection. NexaPay doesn’t ask what you sell. There’s no application form with a business type dropdown. No product catalog review. No underwriting team debating whether your products fall within acceptable parameters. You enter your wallet address and you’re live.

No rolling reserve = full access to your revenue. Every dollar your customer pays (minus the 1–3% fee) is available to you within minutes. No 5–15% withheld for 6–12 months.

No fund freezes = no revenue at risk. The crypto goes to your wallet. There is nothing for anyone to freeze. The nightmare scenario of waking up to find $50,000 locked in a “review” is structurally impossible.

No acquiring bank dependency = no surprise deplatforming. When a traditional processor’s acquiring bank exits your industry, you lose processing capability. NexaPay’s model doesn’t depend on a single bank’s risk appetite for your specific category.

Same low fee for every industry = no high-risk surcharge. A peptide company pays the same 1–3% as an e-commerce store. A casino pays the same as a SaaS business. The fee is based on the transaction, not a risk classification.

Professional checkout = mainstream customer experience. Your customers see a standard card payment form. No crypto terminology. No QR codes. The checkout is clean, fast, and indistinguishable from any mainstream site. This matters for conversion rates across every vertical.

Instant settlement = operational advantage. Casino operators need deposit funds available immediately. Supplement companies need cash flow to restock inventory. Freelancers and service providers need to pay bills. Minutes, not days.

Cost Comparison Across Industries

Savings include fee differential only. Rolling reserve cash flow recovery is additional.

Getting Started

Regardless of your industry, the process is identical:

- Visit nexapay.one

- Enter your crypto wallet address (USDC or USDT for dollar stability)

- Choose integration: payment link (live in 1 minute), WooCommerce/Shopify plugin (15–30 minutes), or custom API

- Accept payments — your customers pay with cards, you receive crypto

No application. No documents. No underwriting. No waiting. No rejection.

Website: nexapay.one

Kira Johansson is an international payments and regulatory compliance analyst based in Stockholm, covering merchant acquiring, restricted industry infrastructure, and the global economics of payment processing. This article reflects independent editorial judgment.

Related searches: payment processing restricted industries, payment gateway for restricted business, payment processor for banned industries, payment processing for peptides, payment processing for CBD, payment processing for supplements, payment processing for gambling, payment processing for adult sites, payment processing for vaping, payment processing for dating sites, high risk industries payment solutions, restricted merchant account, hard to place merchant account, difficult to place payment processing