Finance gurus claim now is the best time to buy. I ran the data to find out if they’re right

With the U.S.-Iran tensions escalating, shouldn’t the price of oil rise? Many “finance gurus” preach this idea, believing that right now is the best time to buy, because tomorrow “it will be too late”. But is what they’re saying true and do any of them back their claims up with something more valuable than empty words? In today’s analysis, we will be analysing 40 years of market data to see if this claim is true.

The Methodology

All of the analysis was conducted in R, using WTI crude oil daily prices from FRED, going back to 1986. The logic of the analysis is picking major conflicts in the Middle East — 1990 Gulf War, 2003 Iraq War, 2019 Aramco Attack, 2024 Iran-Israel (All of these events directly affect oil supply) — then for each conflict I looked at a window of 60 trading days before and 90 trading days after, and indexed prices to 100 on the event date so all four conflicts are directly comparable. It is important to note that this analysis only covers 4 conflicts and is not a universal law. As always, all of the code is available here.

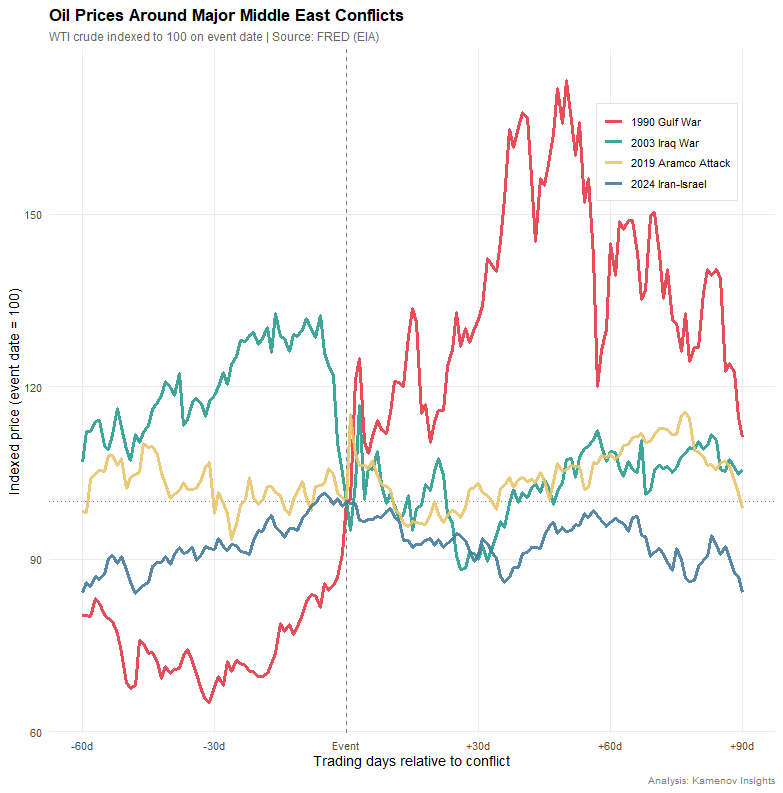

The Overview: 40 Years of Oil Shocks in One Chart

What we can see from the plot is that the biggest difference can be seen in the 1990 Gulf War, where oil was significantly cheaper in the 60 days prior to the event. When the conflict began the price skyrocketed, peaking around day +50.

The story changes for the next conflict in line — the 2003 Iraq War — where the trend is reversed. The price was elevated before the war started and when the invasion began the price started falling. This time investors were significantly more prepared, having done the needed due diligence on the situation around the Middle East.

And in the 2019 Aramco Attack markets did not budge, having a little spike right at the event but eventually price adjusted back to normal. It is fascinating seeing the market shrug off a drone strike that knocked out 5% of the global oil supply within days. And this trend of a indifferent market continued and in the 2024 Iran-Israel conflict it seemed like there was never a threat. Furthermore, oil became cheaper 90 days later, compared to the indexed price on the day of the attack.

Peak Price

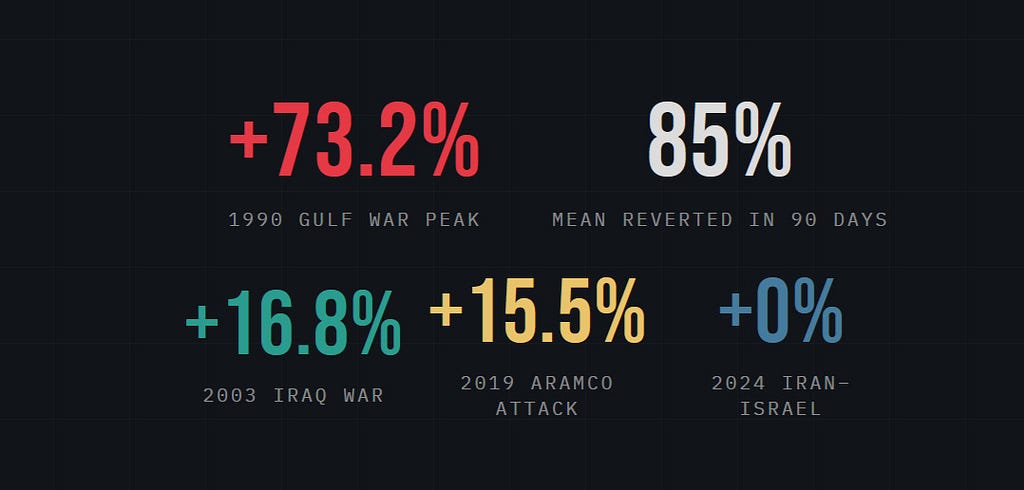

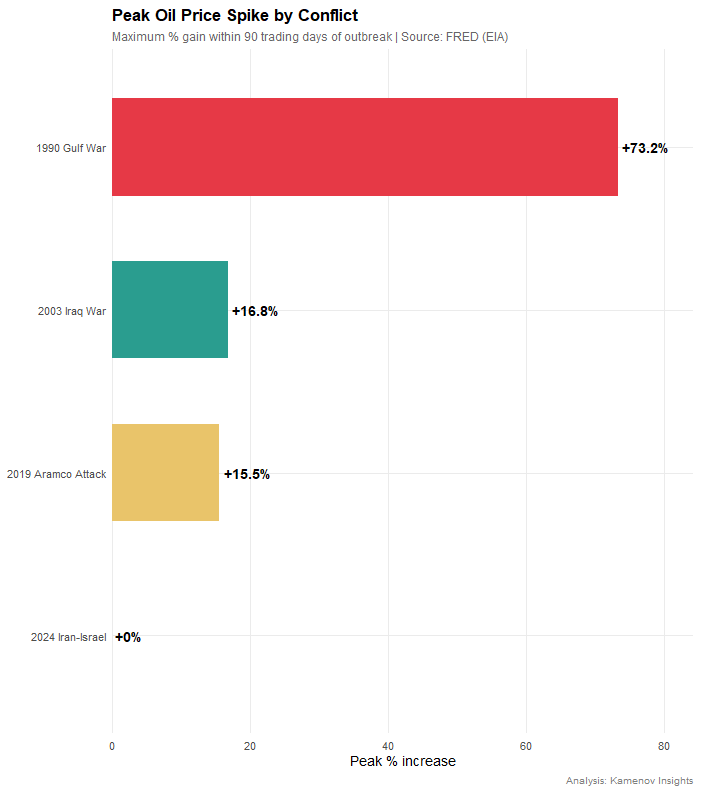

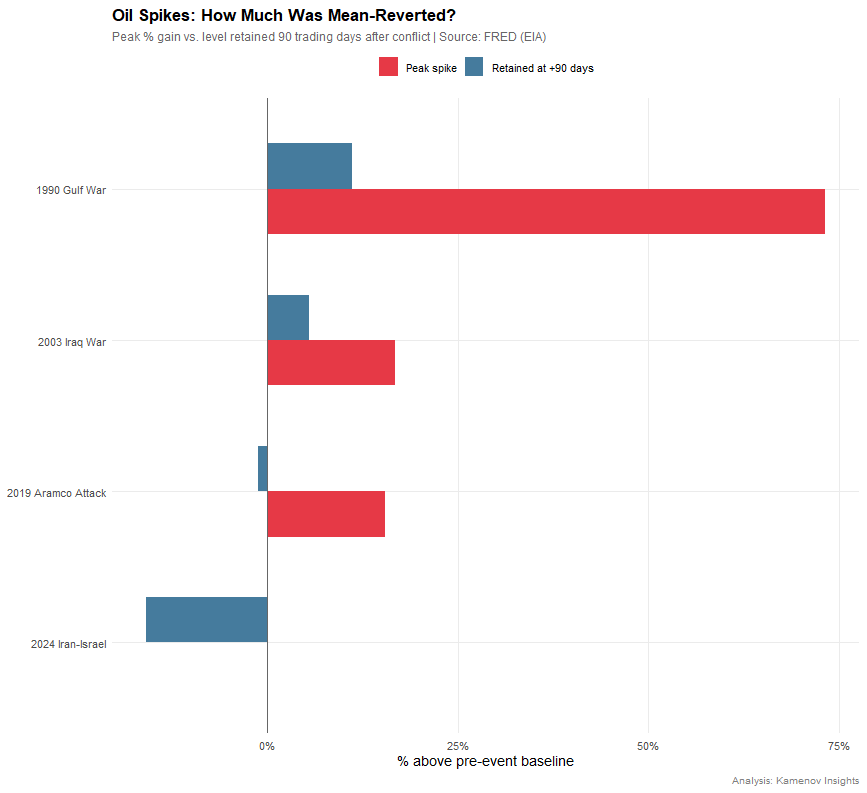

This chart confirms what we saw on the other one — by far the 1990 Gulf War has the largest spike (+73.2%). Oil surged by nearly three-quarters within the next 90 trading days. And as the previous chart shows, every subsequent conflict tells a different story. The 2003 Iraq war has a +16.8% peak– a fraction of 1990’s spike. It is important to note that every peak in this chart is calculated from post-event prices only. For most conflicts this captures the true peak — but 2003 is the exception — the real peak was reached in the pre-event window.

The 2019 Aramco Attack has an interesting reaction — having a peak of +15.5%, almost identical to 2003 despite being a completely different event. This attack was a surprise drone strike, versus the month-long anticipated invasion of 2003. Surprise events typically sustain elevated prices longer — markets lack information and keep uncertainty priced in — yet the Aramco spike unwound just as fast as the anticipated 2003 invasion. The likely reason was that Saudi Arabia restored full production within weeks, removing the supply uncertainty for investors.

And in the 2024 Iran-Israel conflict the bar is nonexistent. Markets saw a direct missile attack on Israel from Iran and didn’t move oil price by a single meaningful percentage point!

The gap between 1990 (+73.2%) and 2024 (+0%) is huge and we can see a clear downward trend forming — with each conflict producing a weaker reaction compared to the previous one. But as we will discuss further down the blog, the market of the 1990 was fundamentally different compared to today’s modern markets.

But what is the point of these gains if they are just a onetime thing — how many of them actually lasted?

How Long Did the Bull Run Last?

As previously stated, the 1990 Gulf War peaked at +73.2%. But the actual sustained gain was far smaller, of these +73.2% only +11.1% was retained at day +90. That means that roughly 85% of the entire spike was given back within 90 trading days.

And this time the next conflict is actually the better performing one. From the +16.8% the 2003 Iraq War managed to retain +5.5% — here only 68% of the value was given back. But the case is not the same for the next event. The 2019 Aramco Attack spiked at +15.5% but it managed to retain almost nothing — after the 90 trading days the market had absorbed everything. And this declining trend did not stop at the next conflict. In the 2024 Iran-Israel conflict the blue bar is to the left of zero — meaning oil was actually cheaper 90 days later than before the attack.

Even in the one case where oil spiked massively (1990), 85% of that gain evaporated within the next 90 trading days, and for every other conflict virtually nothing was retained. So, we know prices spiked, and we know these spikes didn’t last. But there is a deeper question — were markets surprised in the first place?

Markets Price in Risk Before the First Shot?

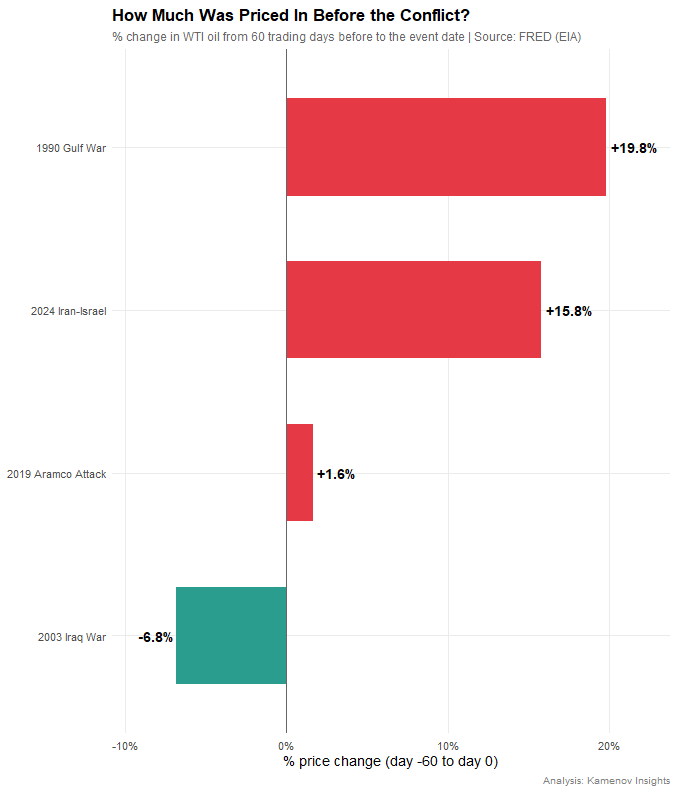

Before the 1990 Gulf war oil was already rising in the 60 days before the invasion (+19.8%), there was for sure some pre-conflict nervousness, but the market wasn’t prepared for what the reality was, hence the massive +73% spike afterwards. The 2019 Aramco Attack shows the opposite — oil was flat beforehand simply because nobody could have anticipated a surprise drone strike.

Here the order of the events is a little changed — the next conflict is the 2024 Iran-Israel, for which investors anticipated a huge rise in oil — pricing in +15.8% before the event, but after the strikes occurred nothing happened. The price flattened and it even declined — oil became cheaper than before the conflict.

The most interesting finding is the 2003 Iraq War, where investors had fully priced in the war during the buildup and by the time the troops crossed the border there was nothing to price in, as a result traders started selling immediately.

As you can see, modern markets do not wait for the guns to fire. Most of the time the risk is priced in weeks in advance and by the time the event occurs the opportunity is gone. But truly how fast are modern markets?

The Speed of The Modern Market

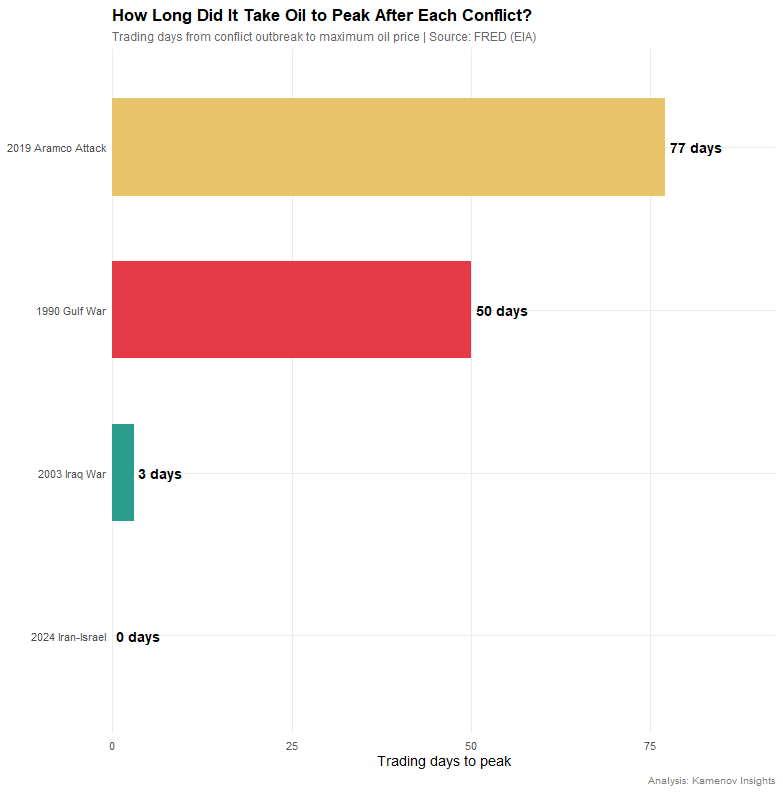

The 2019 Aramco attack was the slowest of the four — taking 77 days to reach its peak price. This attack was a surprise, and investors anticipated more surprises along the way (the Houthi threat of follow-on strikes), which explains its huge timeline. But eventually the market reassessed the geopolitical risk and the price started adjusting. The case is the same for the 1990 Gulf war; Iraq’s invasion of Kuwait caught most of the world off guard. That’s the reason it took the market 50 days to reach peak price, because markets lacked the information and tools to forecast what would come next. That uncertainty kept the price at those high levels for weeks.

And as we continue down the road, the market is starting to get smarter and smarter. The 2003 Iraq War was fully anticipated — only taking 3 days to reach peak price, traders had nearly nothing to price in, so the post-event peak lasted just 3 days before the selloff began. And now the closest event to the present — the 2024 Iran-Israel — peaked right on the event day itself and fell every single day after. Modern markets process geopolitical information almost instantaneously and all of that uncertainty keeping the price up is gone.

So, were the “Finance Gurus” Right?

From everything we saw in the analysis, the data does not support their thesis. Middle East conflicts no longer reliably move oil prices in any sustained way. Modern markets have gotten very good at processing information and overall being better informed about the world around us. Furthermore, US shale oil reduced dependence on Middle Eastern supply, and strategic reserves exist as a buffer just for this reason. These structural shifts also explain why the 1990 stands as such an outlier — it occurred in a pre-internet market with no US shale supply ceiling and no strategic reserve culture. Based on the data, we can argue that for the current U.S.-Iran situation, oil price moves will be short-lived and likely already priced in.

However, modern markets are not perfect. The 2019 Aramco Attack is a reminder of that — despite occurring in an era of sophisticated trading and instant information, it still took 77 days to reach its peak, the longest of all four conflicts. Oil prices are not only affected by the Middle East, but they are also affected by OPEC production decisions, USD strength, and global demand. Past patterns do not guarantee future behaviour, and a conflict surprising and large enough to cause a genuine, sustained supply disruption could still move markets significantly.

If this analysis has helped you, make sure to follow me, so you do not miss out on future ones.

Oil Markets Don’t Fear War Anymore — Data Proves it was originally published in DataDrivenInvestor on Medium, where people are continuing the conversation by highlighting and responding to this story.