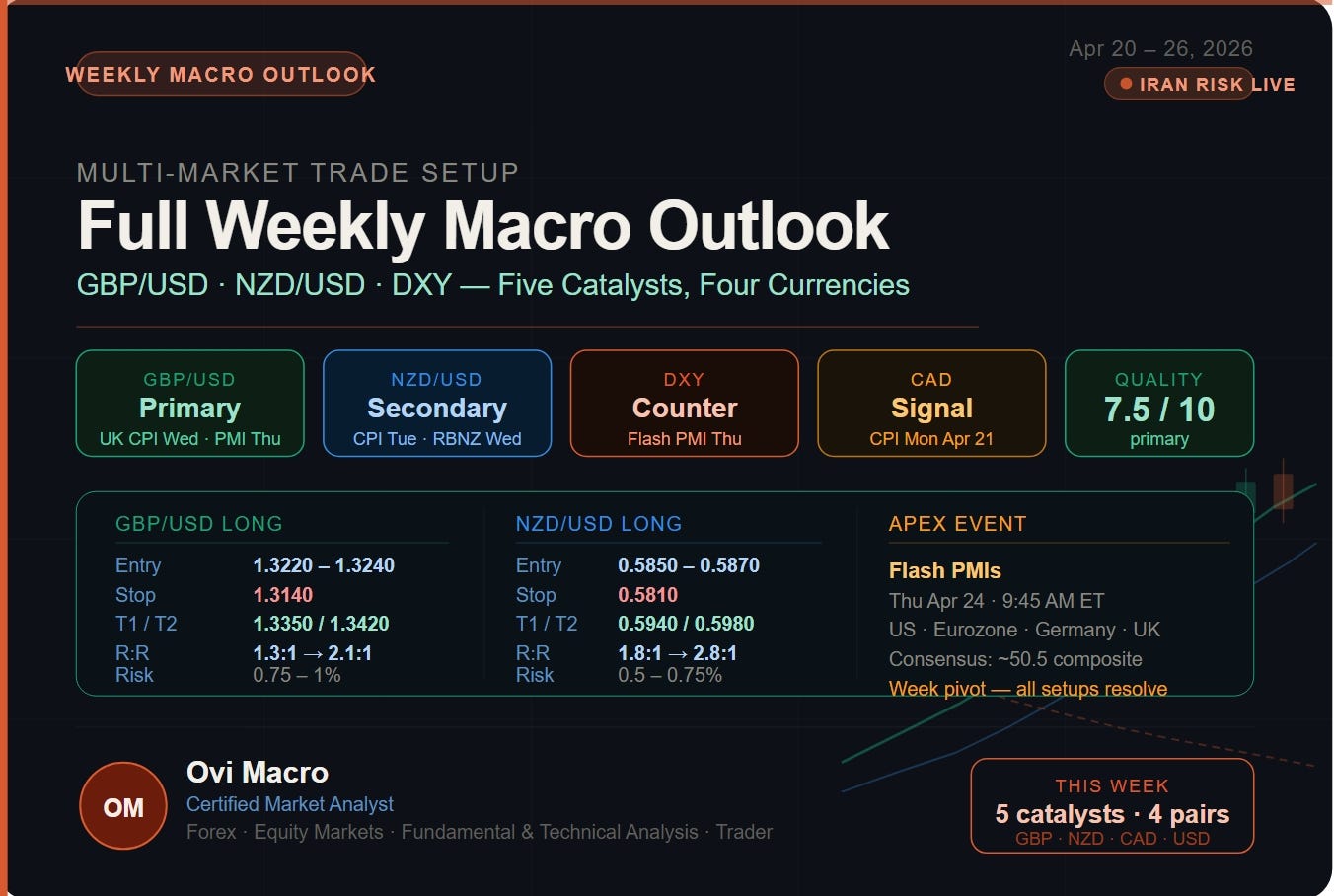

Multi-Market Trade Setup: Full Weekly Macro Outlook — Week of April 20, 2026

@OviMacro13 min read·Just now

@OviMacro13 min read·Just now--

Five catalysts. Four currencies. One geopolitical overlay tying all of them together. This is not a week where you watch one number and go home. Every day from Monday through Friday carries a market-moving release, and every single one is a test of the same underlying question: is the Iran-Strait of Hormuz energy shock creating real, lasting economic damage — or is it fading? The answer builds day by day and resolves Thursday morning at 9:45 AM ET when S&P Global drops flash PMIs for the US, Eurozone, Germany, and the UK simultaneously. Here is the complete game plan across every event, every pair, and every setup.

Event calendar — week of April 20–24, 2026

Monday April 20 PBoC 1-year Loan Prime Rate decision (overnight GMT) — medium impact on CNH and risk appetite. CAD CPI March 2026 at 8:30 AM ET — previous 1.8% YoY, energy push expected to accelerate it toward 2.3–2.5%. These are the only two confirmed high-impact events Monday. NZD CPI Q1 2026 (overnight NZT, landing Sunday evening ET) — previous 3.1% Q4, still above the RBNZ’s 1–3% target ceiling.

Tuesday April 21 NZD CPI Q1 2026 (overnight NZT, prints as Tuesday in ET), GBP employment data at 2:00 AM ET — claimant count, unemployment rate (expected steady at 5.2%), and private sector wage growth (seen falling). This is the BoE’s primary domestic cost pressure gauge. US Retail Sales March (8:30 AM ET) — headline boosted by gasoline prices, control group (strips autos and energy) is what moves markets and previews Thursday’s PMI. This is the heaviest single day of the week — three high-impact releases across three currency pairs before the US afternoon session even opens.

Wednesday April 22 GBP CPI March 2026 at 2:00 AM ET — consensus 3.3% headline (prior 3.0%), core seen steady at 3.2%, services CPI at 4.2% in February. The Bank of England’s own staff estimates put March close to 3.5% driven entirely by energy pass-through from Brent. No other high-impact releases Wednesday.

Thursday April 23 US Initial Jobless Claims at 8:30 AM ET — medium impact, watch for any labour market softening adding to growth-scare narrative. Do not trade before PMIs. S&P Global Flash PMIs at 9:45 AM ET — US, Eurozone, Germany, UK simultaneously. This is the apex event of the week. US New Home Sales at 10:00 AM ET — low impact, rate-sensitivity context only.

Friday April 24 GBP Retail Sales March at 2:00 AM ET — consumer squeeze from energy prices, post-CPI confirmation read. CAD Retail Sales February at 8:30 AM ET (Statistics Canada confirmed release) — previous estimate +0.9%, BoC April 29 calibration. USD Durable Goods Orders (core ex-transport) at 8:30 AM ET — business investment signal. Japan CPI March overnight JST — consensus 1.5% headline, core returning to 2.0% BoJ target. UoM Consumer Sentiment revised at 10:00 AM ET — preliminary collapsed to a record low 47.6 in April; revised reading and inflation expectations confirm or deepen the soft-demand narrative heading into FOMC.

Upcoming next week (shape this week’s positioning): FOMC April 28–29 (hold near-certain, one cut priced for all of 2026), BoC April 29 (cut possible — CAD CPI Monday sets the tone), BoJ April 28, RBNZ next May 27.

Section 1: The geopolitical overlay and why it connects everything

Iran reimposed Strait of Hormuz restrictions on April 18. The US naval blockade of Iranian ports remains in force. Brent crude sits near $82–90/bbl after spiking above $110 earlier in the conflict and retreating on partial ceasefire hopes. Every central bank watching this week’s data is reading the same energy price chart and asking the same question their mandate demands: is this shock inflationary, deflationary, or both at once?

The answer is both — and that stagflationary tension is what makes every release this week tradeable in two directions. Energy prices are pushing headline CPI numbers up across the UK, Canada, and New Zealand simultaneously. At the same time, the same energy prices are crushing consumer purchasing power and business confidence, which shows up in retail sales, PMI sub-indices, and employment data. The market has to decide which force dominates — and this week’s data stack is the verdict.

The geopolitical risk is not background noise this week. It is the mechanism. Iran headlines that escalate — fresh Strait incidents, blockade tightening, oil spiking above $100 intraday — can override even perfectly clean data reactions without warning. Size every position conservatively and keep stops tight.

Section 2: How each event connects — the catalyst chain

Monday’s CAD CPI is the first piece. Canada’s February CPI printed 1.8% — the lowest in years — but the Bank of Canada explicitly flagged that gasoline prices from the Iran shock “will push up total inflation in the coming months.” A March print accelerating above 2.5% confirms energy pass-through is happening systematically across commodity-linked G10 currencies. This calibrates the NZD CPI expectation and amplifies the BoC April 29 positioning.

Tuesday NZD CPI (Q1, overnight) is the highest individual R:R catalyst of the week. Q4 2025 already printed 3.1% — above the RBNZ’s 1–3% ceiling — driven by electricity up 12.2% YoY, the direct consequence of global energy cost pass-through from the Iran conflict. If Q1 2026 matches or exceeds that level, the market is forced to reprice NZD higher because the next RBNZ meeting is May 27 and any cut language disappears entirely. The market currently prices near-zero chance of a hike; a hot Q1 CPI shifts that materially.

Tuesday’s UK employment data sets the context for Wednesday’s CPI. Falling wage growth alongside still-elevated unemployment means the BoE faces a genuine stagflationary bind — costs rising from energy, but no wage-price spiral risk. This is the setup that keeps the BoE stuck on hold while the US potentially loosens. That divergence is the GBP/USD long thesis.

Tuesday’s US Retail Sales control group is my pre-PMI read on US consumer health. A weak control group (flat or negative) confirms that American households are feeling the energy price squeeze — households spending less on discretionary items because fuel is eating their budget. This previews a soft PMI Thursday and directly supports the GBP/USD long. A strong control group above +0.4% signals resilience and raises the probability of a hot PMI beat.

Wednesday’s UK CPI is the primary entry trigger for the GBP/USD long. The BoE’s own staff estimate puts March CPI at approximately 3.5%. Consensus is 3.3% headline with services at 4.2%. A print at or above 3.3% — especially with services holding above 4.0% — confirms the BoE cannot cut and sets up the divergence trade against a potentially more dovish Fed. This is the London open trade.

Thursday’s Flash PMIs are where the week resolves. Every prior data point builds toward this number. Markets are pricing US composite around 50.5 — barely expansionary. A miss below 50 on services confirms demand destruction from the energy shock. A beat above 52 confirms stagflation resilience. The dollar, GBP/USD, NZD/USD, and equities all reprice simultaneously.

Friday’s GBP Retail Sales and CAD Retail Sales close the loop. After the CPI spike confirmed inflation, retail data tells us whether consumers are still spending or beginning to retrench. Weak GBP retail sales following hot CPI = full stagflationary read = BoE trapped = GBP supported. Weak CAD retail after hot CAD CPI = same picture for the BoC April 29 decision.

Section 3: Primary setup — GBP/USD long on UK CPI divergence + US PMI softness

Setup name: GBP/USD dual-catalyst divergence long

The core thesis is simple. The UK and US are diverging in the same stagflationary environment. UK CPI is spiking toward 3.5% driven by energy — the BoE cannot cut. US PMIs are expected at a barely-expansionary 50.5 — if they miss, the Fed’s cut odds rise. Pound up, dollar down — GBP/USD surges from both sides simultaneously.

GBP/USD closed Friday April 17 at approximately 1.3220. The pair has been supported above 1.3100 on BoE-hold expectations and US soft-data fears but has stalled below 1.3300 on residual safe-haven dollar demand from Iran. The setup has two sequential entry windows.

Entry rules: IF UK CPI Wednesday prints above 3.3% headline AND GBP/USD holds above 1.3180 through the London morning session, enter 50% of full position at the London open (approximately 3:00–4:00 AM ET Wednesday) in the 1.3220–1.3240 zone. IF US flash services/composite PMI Thursday prints below 50.5 AND GBP/USD breaks above 1.3300 on the 30-minute chart within two hours of the 9:45 AM ET release on expanding volume, add remaining 50% at 1.3305–1.3315 (breakout retest).

Stop Loss: 1.3140. Why here and not tighter: the 1.3140 level is below the April consolidation floor and below the immediate swing low from April 17. A 30-minute close below 1.3140 means either the dollar safe-haven bid is dominating completely — geopolitics are overriding data — or the UK CPI was a miss and the trade thesis is wrong. Either way the position exits.

Targets: T1 at 1.3350 — the April swing high and measured move of the range. At T1 take 50% profit, move stop to breakeven at 1.3240. T2 at 1.3420 — extension target last seen before the initial Iran shock pushed safe-haven flows into the dollar.

Risk/Reward: entry average approximately 1.3265 (blended across two tranches), stop 1.3140 = 125 pips risk. T1 at 1.3350 = 85 pips on first tranche. T2 at 1.3420 = 155 pips on second tranche. Full position R:R: 1.3:1 to T1, 2.1:1 to T2. Position sizing: 0.75–1% account risk. Time horizon: Wednesday through Friday, potentially carrying into early next week.

Counter-trade if UK CPI misses (prints below 3.0%) or US PMI beats (above 52): GBP/USD reverses below 1.3140. Short at 1.3130–1.3120, stop 1.3200, targets 1.3060 then 1.2980. R:R 1.0:1 to T1, 1.8:1 to T2. Risk 0.5% account.

Section 4: Secondary setup — NZD/USD long on above-target Q1 CPI

Setup name: NZD/USD momentum long — above-ceiling CPI repricing

This is the cleanest R:R trade of the week because the market is severely underpricing the inflation risk. The RBNZ held at 2.25% on April 8 — already done — with the next meeting on May 27. Q4 CPI was already 3.1%, above the top of the RBNZ’s 1–3% band. If Q1 2026 matches or exceeds that, the hawkish repricing is immediate and sharp because no RBNZ meeting can relieve the pressure until May 27.

NZD/USD sits near 0.5860, rangebound between 0.5810 and 0.5900. The pair is offered because NZ’s growth outlook is soft — Q4 GDP rose only 0.25% quarter-on-quarter — but inflation is hot. That is a central bank’s nightmare. A hot Q1 CPI Monday removes any near-term cut expectation and forces NZD higher regardless of the growth picture.

Entry rules: IF NZD CPI Q1 2026 prints at or above 3.1% (Monday evening ET / Tuesday NZT overnight) AND NZD/USD holds above 0.5835 on the first Sydney open after the release, enter long at 0.5850–0.5870 on any pullback toward support. Do not chase the initial spike. Wait for a settled 15-minute or 30-minute candle in the entry zone.

Stop Loss: 0.5800. Why here: below 0.5800 means either the CPI missed badly (disinflation winning despite oil) or a major Iran risk-off event is driving broad USD strength that overrides everything. Both scenarios invalidate the setup entirely.

Targets: T1 at 0.5940 — resistance zone and measured move above the range. At T1 take 60% profit, move stop to breakeven at 0.5860. T2 at 0.5980 — extension target and psychologically significant level approaching 0.6000.

Risk/Reward: entry approximately 0.5860, stop 0.5800 = 60 pips risk. T1 at 0.5940 = 80 pips = 1.3:1. T2 at 0.5980 = 120 pips = 2.0:1. If holding through Thursday’s PMI soft scenario, USD weakness adds momentum toward T2. Position sizing: 0.5–0.75% account risk — slightly smaller than GBP trade given NZD’s vulnerability to sudden Iran-driven risk-off. Time horizon: Monday through Thursday.

Counter-trade if NZD CPI misses (below 2.8%): Short NZD/USD at 0.5790–0.5800, stop 0.5860, targets 0.5720 then 0.5660. This correlates with the broader soft-NZD / strong-USD risk-off scenario.

Section 5: Week-ahead execution plan — day by day

Monday April 20 — information day:

PBoC rate decision (overnight GMT) — I watch for any surprise liquidity injection or forward guidance that affects risk appetite at the Asian open.

No new GBP or USD directional bets Monday. Pre-set limit order alerts at GBP/USD 1.3180 and 1.3300, NZD/USD 0.5850 and 0.5900.

CAD CPI at 8:30 AM ET is my early calibration signal for the week. A print above 2.5% confirms energy pass-through is feeding through commodity-linked currencies uniformly — supporting the NZD CPI hot scenario and adding context for the BoC April 29 decision. I do not trade USD/CAD directly this week — BoC meets next week, not this week — but CAD CPI calibrates my confidence in the NZD trade.

Tuesday April 22 — NZD CPI + UK employment + US Retail Sales:

NZD CPI lands on Tuesday. Set an alarm. If Q1 prints at or above 3.1%, I’m ready to enter NZD/USD long at the Sydney open on a settled retest of 0.5850–0.5870. I do not chase the initial spike. A 15-minute close in the entry zone is the trigger.

GBP employment at 2:00 AM ET. I watch the wages component most closely. A fall in private sector wage growth alongside steady unemployment confirms the stagflationary setup heading into Wednesday’s CPI — that is the pattern that keeps the BoE on hold regardless of energy. Soft wages = BoE cannot hike even with 3.5% CPI = GBP initially offered, but the medium-term bias remains long because no cuts are coming either.

US Retail Sales control group at 8:30 AM ET. If the control group prints below +0.2%, I increase my conviction on Thursday’s soft PMI scenario and begin building the GBP/USD long position ahead of Wednesday’s UK CPI entry trigger. If the control group beats above +0.4%, I keep GBP/USD size smaller and wait for Wednesday’s CPI to do the work independently.

Wednesday April 23 — UK CPI, the primary entry:

2:00 AM ET. This is the most important trade execution window of the week. I watch the London open from 3:00 AM ET onward. If headline prints at or above 3.3% with services holding above 4.0%, I enter 50% of the GBP/USD long at 1.3220–1.3240. If the print is below 3.0%, I flip to the counter-trade and monitor for the short below 1.3140.

The rest of Wednesday is position management. No other high-impact data. I watch oil price action — any Brent spike above $95 intraday on fresh Iran headlines is a warning that geopolitics are overriding data and I reduce exposure.

Thursday April 24 — the week’s verdict:

8:30 AM ET: US Jobless Claims. Watch for any labour market softening that adds to the growth-scare narrative. Do not trade. Monitor 2-year Treasury yields and oil in real time as leading indicators of how the PMI is about to land.

9:45 AM ET: Flash PMIs release. I read the US services and composite numbers first, then UK composite, then Eurozone.

Soft US composite below 50.5: Add the remaining 50% of the GBP/USD long at 1.3305–1.3315 if price breaks above 1.3300 on a 30-minute close. NZD/USD long already running — tighten stop to breakeven at 0.5860.

Hot US composite above 52: GBP/USD long thesis is under pressure. Exit half the position immediately on a 30-minute close back below 1.3240. Watch for counter-trade triggers.

Afternoon: Manage positions. Watch Iran news flow — any Strait escalation overrides data interpretation.

Friday April 25 — closing the loop:

GBP Retail Sales at 2:00 AM ET. If sales are weak following Wednesday’s hot CPI, this is the stagflationary confirmation — BoE trapped, consumer hurting. GBP/USD long holds toward T2. If retail is surprisingly strong, consider taking T1 profit early.

CAD Retail Sales at 8:30 AM ET. Weak print increases probability of BoC cutting April 29 — CAD-negative. If I have any USD/CAD exposure it gets relevant here, but my primary trades are not CAD this week.

US Durable Goods and UoM Sentiment at 8:30/10:00 AM ET. These confirm or deepen the Thursday PMI narrative. Weak durable goods plus a revised UoM Sentiment staying near record low 47.6 = soft-demand thesis locked in = GBP/USD holds toward T2.

Section 6: Invalidation — when I’m completely wrong

Three conditions kill every setup simultaneously:

A major Strait of Hormuz escalation — confirmed vessel seizure, military strike on a tanker, or formal blockade tightening — that sends Brent above $100 intraday. In this scenario risk-off dominates everything. USD and JPY strengthen on safe-haven flows. GBP/USD and NZD/USD both fall regardless of what the data said. I stand aside entirely and wait for the first 24-hour period of oil stability before re-evaluating.

UK CPI prints below 3.0% and US PMI beats above 52 simultaneously. Pound weak, dollar strong — GBP/USD breaks below 1.3100 and the entire week’s thesis inverts into the counter-trade framework.

NZD Q1 CPI prints below 2.8% and global risk-off deepens. Disinflation is winning despite the energy shock in New Zealand. RBNZ cuts are back on the table. NZD/USD short is the active trade, not the long.

If any of the above happens, my alternative action is to stand aside for 24 hours, let the volatility settle, and re-enter only on confirmed price structure. I do not revenge-trade into a geopolitical escalation.

Conclusion

Bottom line: Five catalysts, four currencies, one geopolitical overlay. My primary trade is GBP/USD long — entry 1.3220–1.3240 on Wednesday UK CPI, scaled to 1.3305 on Thursday soft PMI, stop 1.3140, T1 1.3350 (1.3:1 R:R), T2 1.3420 (2.1:1 R:R), risk 0.75–1% account. My secondary trade is NZD/USD long — entry 0.5850–0.5870 on Tuesday Q1 CPI beat, stop 0.5800, T1 0.5940 (1.3:1), T2 0.5980 (2.0:1), risk 0.5–0.75% account. Both setups share the same macro thesis: the Iran energy shock is keeping inflation elevated in energy-importing economies while simultaneously threatening growth, which punishes the dollar and rewards currencies whose central banks have less room to cut. Friday closes the loop with GBP and CAD retail sales confirming or denying whether the stagflationary squeeze has reached the consumer.

Iran keeps every tail risk live. Size conservatively, respect the stops, and trade the confirmation — never the anticipation.

Primary setup quality (GBP/USD): 7.5/10. Sequential dual-catalyst structure and genuine macro divergence. Live Iran headlines are the only structural limitation.

Secondary setup quality (NZD/USD): 7/10. Best R:R of the week. Growth softness in NZ is the counterweight.

This is my complete game plan. Markets evolve — I’ll update if key levels are invalidated before Thursday. Trade your own plan.