Morpho just flipped AAVE in FDV. With zero revenue. Here’s why both valuations are wrong.

Sungku Kim5 min read·Just now

Sungku Kim5 min read·Just now--

“$AAVE generates $140M in protocol revenue. $Morpho generates $0 for token holders. Morpho’s FDV is higher. This is what that tells you about both protocols.”

Although the two protocols show an incomparable gap in terms of TVL (Total Value Locked) and actual protocol revenue, the future value (FDV) assigned by the market is completely flipped. At the foundation of this anomaly lie two massive ticking bombs: AAVE’s ‘governance collapse risk’ and Morpho’s ‘insider exit risk’.

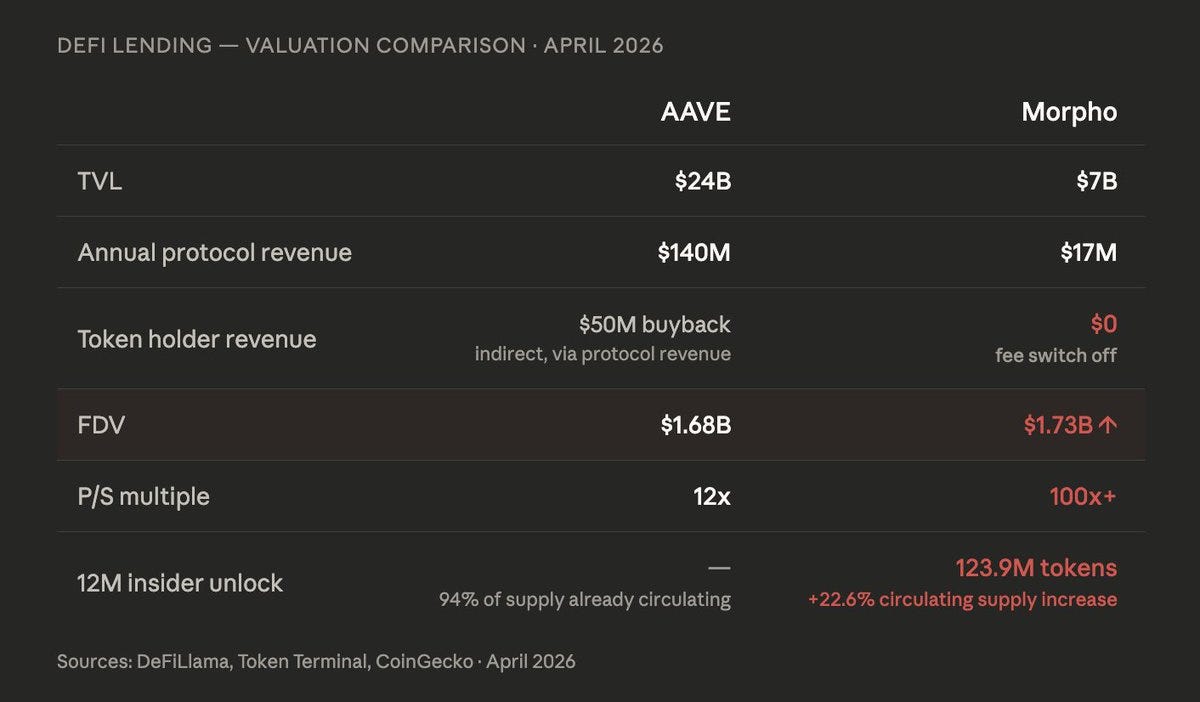

• The Valuation Inversion Phenomenon: The Contradiction of Numbers As of April 2026, AAVE is the overwhelming undisputed leader, generating massive protocol revenues of approximately $140 million annually based on a TVL of $24 billion. In contrast, Morpho’s TVL sits at $7 billion, and even assuming a 10% fee rate, its projected protocol revenue is only $17 million. Since its fee switch is turned off, the actual revenue for token holders is ‘0 (Zero)’.

However, looking at the Fully Diluted Valuation (FDV), while AAVE sits at around $1.68 billion, Morpho, with zero cash flow, exceeds $1.73 billion, overtaking AAVE. Translated to P/S multiples, AAVE trades at 12x, while Morpho exceeds 100x+. The cash-generating ability is extremely undervalued, while vague technological expectations are grossly overvalued.

• AAVE will win? No, Aave is losing. The reason AAVE is stuck in an extreme undervaluation territory compared to its revenue is not due to a deterioration of fundamentals, but rather a fatal internal self-inflicted wound.

① Product Graveyard: The founding company, Aave Labs, received massive DAO funding to launch numerous in-house products such as Lens Protocol and the Family wallet app, but all failed without significant results. In particular, the ‘Horizon Pool’, an institutional RWA market, showed a deformed structure by burning $5.25 million in incentive budgets to generate $210,000 in profit, earning the mockery of the ‘product graveyard’ from the community.

② Governance Civil War: In a situation where failures accumulated, Aave Labs demanded a massive upfront payment of $51 million (42% of the DAO treasury’s non-AAVE holdings) under the pretext of transferring front-end revenue to the DAO. During this process, they forced the proposal through with a ‘self-voting’ scheme mobilizing founder-related wallets, shattering the trust in governance.

③ Core Team Exodus: The core contributors, furious at this blatant privatization attempt, exploded. BGD Labs, who directly coded and advanced the AAVE V3 code over the past few years, ACI, who led the governance, and Chaos Labs, the risk management team defending against tens of billions of dollars in bad debt, threw in their resignations one after another like dominoes. This incident, where AAVE’s heart and brain simultaneously drained away, has heavily weighed down its valuation.

④ The “Deep Value” Illusion (Value Capture Failure): One might argue, “With a P/S multiple of just 12x, isn’t AAVE heavily undervalued for a blue-chip?” The answer is no. Currently, the AAVE token has a very weak link to actual protocol revenue. If you stake AAVE in the Safety Module, you bear slashing risks in exchange for stkAAVE rewards. However, these rewards are funded by token inflation, not protocol revenue. The $140M in protocol revenue simply piles up in the DAO Treasury (with only about $50M indirectly used for buybacks). Aavenomics V3 attempted to fix this, but the governance civil war derailed its execution. It closely resembles Uniswap: massive revenue, but an incomplete value capture mechanism for token holders. Despite the advantage of having 94% of its supply already circulating (essentially zero inflation risk), the integrity of governance in managing the treasury fairly was absolutely crucial — and the recent civil war shattered exactly that trust. Therefore, as long as token value capture remains broken, a 12x multiple is absolutely not a cheap price.

• So, Morpho’s Comeback Victory? No, A Severe Bubble and the Shadow of Pump and Dump Taking advantage of AAVE’s chaos, Morpho’s FDV has flipped, but behind the scenes lies a dark shadow of a massive ‘dumping on retail investors’.

① Upcoming Supply: The token supply scheduled to be unlocked and dumped by insiders, such as Venture Capitals (VCs) and the development team, over the next 12 months is approximately 123.9 million tokens. This is a brutal inflationary pressure that will cause the circulating supply to explode by 22.6% in a short period. (This starkly contrasts with AAVE, which has 94% circulating and essentially zero inflation risk).

② The Illusion of Apollo’s Purchase (A Drop in the Bucket): Recently, the major positive news that Apollo is buying 9% of the supply pumped the price, but this is a phased purchase over 48 months. Even if they accumulate the maximum amount every month, it can only defend about 18% of the pouring insider dumping supply, which is merely a drop in the bucket. Furthermore, this is highly likely to be an Over-The-Counter (OTC) trade at a discounted price, not a market purchase.

③ Paltry Fee Revenue: The projected DAO revenue generated in the Morpho ecosystem is only about $17 million annualized. This is paltry compared to AAVE’s overwhelming protocol revenue ($140 million).

④ Token Holder Revenue is 0: The most fatal point is that out of the projected $17 million in fees, the revenue returning to MORPHO token holders is ‘0 (Zero)’. This is because the fee switch is turned off. If the switch is turned on, it faces a Catch-22 situation where liquidity and curators, sensitive to interest rates, could fork the open-source code and leave.

⑤ Current Fair Valuation: Considering both the massive overhang risk and ‘zero’ cash flow, the current FDV of $1.73 billion (a P/S multiple exceeding 100x+) is a severe bubble.

• Conclusion: AAVE vs. Morpho, The Market’s Judgment Stand The valuation inversion phenomenon of the two protocols can be interpreted as follows: AAVE’s case honestly reflects ‘the actual deterioration of fundamentals due to a governance collapse’, while Morpho’s overvaluation is a mix of ‘substanceless expectations and a bubble for insider token exits’.

What AAVE Must Prove: The ‘execution ability’ of Aave Labs to fill the void left by top external experts like BGD Labs and Chaos Labs, and to safely operate the V4 architecture without a single hack or liquidation incident.

What Morpho Must Prove: Completing a ‘substantial Value Capture model’ that brings profit to token holders without liquidity flight, while simultaneously digesting the tens of millions of insider tokens pouring out every month.

After the blind worship of TVL and speculative narratives clear away, it is time to coldly observe how the market will price the structural limits of these two giants.