Module 01: Quant Foundations — The Structural Skeleton

Joshua van Lynden6 min read·Just now

Joshua van Lynden6 min read·Just now--

In Module 00, we dismantled the myth of the “deterministic” brain. We accepted that the world is a non-linear, stochastic meat grinder where “being right” is secondary to “surviving the path.”

But once you accept that the world is chaotic, you face a new problem: How do you actually hold your capital? Most traders, even at the institutional level, build their portfolios on a foundation of sand. They use tools designed for a world of stability — a world that hasn’t existed since the invention of the ticker tape. They rely on “diversification” that is purely cosmetic.

If you want to manage an institutional mandate — or even a €100k personal account — you need a skeleton. You need a structure that doesn’t just look good on a backtest but remains standing when the market tries to tear it down.

Welcome to Module 01. We are throwing the traditional textbooks in the trash and introducing the HRP Framework.

1. The Correlation Trap: Diversification is a Paper Tiger

Modern Portfolio Theory (MPT) is the “standard model” of finance. It teaches you to build a portfolio using a correlation matrix. The logic is simple: find Asset A and Asset B that don’t move together, put them in a bucket, and you’ve “reduced risk.”

Mathematically, the correlation coefficient is defined as:

The textbook tells you that if (p) is low, you are safe. This is a lie.

In a true crisis, all correlations go to 1.0.

When the “fat tail” hits — whether it’s a geopolitical shock in the Strait of Hormuz or a sudden liquidity vacuum — everything sells off. Your “uncorrelated” basket of copper miners, silver explorers, and oil producers all head for the bottom at the same time. The “diversification” you counted on evaporates exactly when you need it most.

The problem with correlation matrices is that they are unstable. They are historical artifacts, not predictive truths. They assume the structure of the market is fixed. But the market is a living organism; its segments move, merge, and fracture. Relying on a static correlation matrix is like navigating a shifting desert using a map drawn ten years ago.

2. Hierarchical Risk Parity (HRP)

Correlation matrices can be fragile, especially when correlations shift abruptly during regime changes or crises. An alternative approach is Hierarchical Risk Parity (HRP), which is often seen as a major shift in portfolio construction.

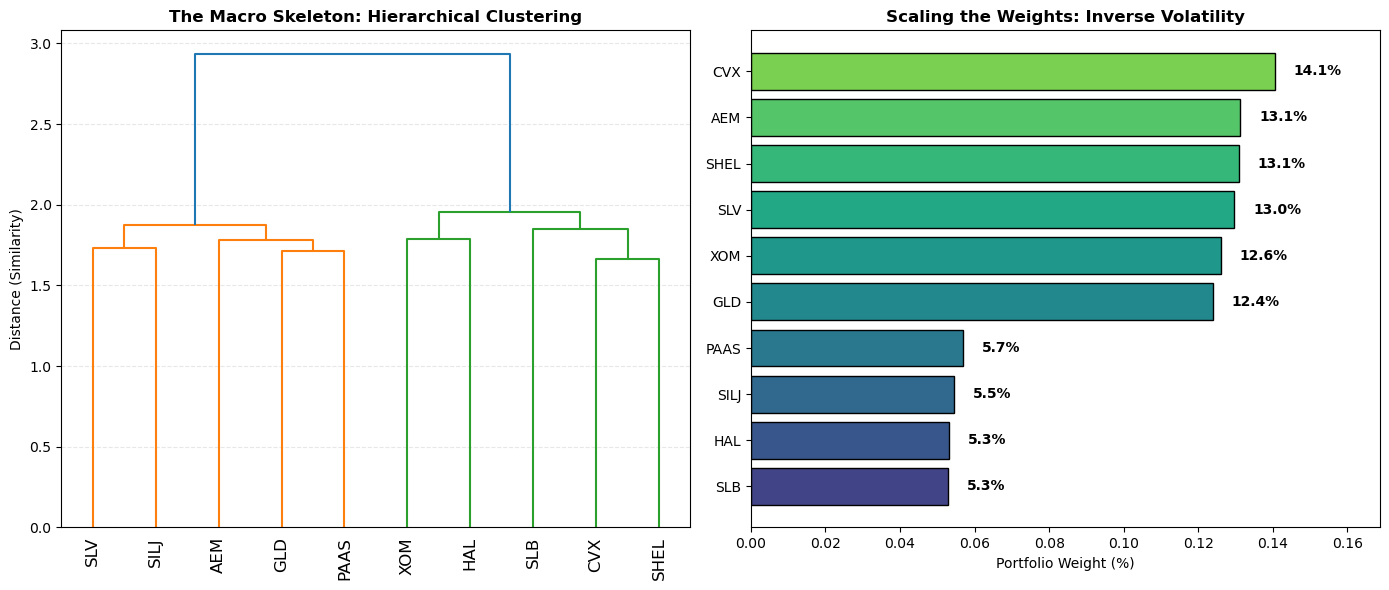

HRP, developed by Marcos López de Prado, avoids imposing a fixed structure on the market. Instead, it lets the data reveal its own “natural hierarchy.” Rather than working with a flat correlation matrix of, say, 50 tickers, HRP represents the market as a tree (a dendrogram) and uses clustering algorithms to group assets with similar behavior.

That said, even this hierarchy is not absolute — it is data-driven and can change over time. Still, it provides a useful and often more stable framework for understanding relationships between assets and allocating risk across them.

In practice, as a portfolio manager, I don’t rely purely on any single statistical structure. I start from existing market intuition and then optimize on top of it. The idea is to keep what is robust and discard what is noisy or unstable. I also incorporate more persistent “structural” features, such as volatility. Some relationships are fairly stable over long periods — for example, silver tends to be structurally more volatile than oil due to its market dynamics and liquidity profile.

When investing in equities, diversification also needs to account for differences across sectors and business models. Within energy, for instance, producers vary significantly in risk. A diversified integrated company like Chevron typically exhibits lower volatility than a more service-oriented and cyclical firm like Schlumberger, which is more exposed to drilling cycles and capital spending fluctuations.

So the goal is not to find a perfect statistical structure, but to combine stable economic intuition with adaptive data-driven tools like HRP, while being aware that both the hierarchy and correlations themselves evolve over time.

3. Scaling the Weights: Risk-Parity in Action

Once we have our clusters, how do we determine how much to buy? Most people weight their portfolio by “conviction” (how much they like a stock) or by market cap. Both are fundamentally flawed. Conviction is an emotion; market cap is a trailing indicator.

I prefer to use risk-parity to scale positions.

We define the weight of an asset based on its inverse volatility. The goal is to ensure that every position contributes the same amount of risk to the portfolio. If Asset A is twice as volatile as Asset B, you hold half as much of it.

But we apply this at two levels:

- Inter-Cluster (The Macro Skeleton): We scale the clusters themselves. If the “energy” cluster is currently showing massive variance, the HRP algorithm automatically reduces the “energy” weight to protect the total portfolio “skeleton.”

2. Intra-Cluster (The Subcluster): Within the “equities” or “commodity” bucket, we scale our individual stocks based on their risk profile. A volatile silver miner gets a smaller weight than a diversified major.

This isn’t about “optimizing” for the highest return on a screen. It’s about equalizing the pain. When one sector hits a “fat tail,” the structural integrity of the rest of the portfolio remains intact because that sector was never allowed to dominate the risk budget.

4. The Myth of Cross-Asset Hedging

There is a common belief in the “macro” world that you can hedge a commodity position with a different asset class. “I’m long copper, but I’m short the Aussie Dollar to hedge the China risk.”

While cross-asset diversification can reduce variance under “normal” market conditions, it breaks down exactly when it matters. During a regime shift, those historical relationships snap. The hedge that worked for three years suddenly becomes a second losing trade. As a practioner, I recognize that cross-asset hedging is often overstated. It gives you a false sense of security while eating away at your returns through “drag.”

The Solution: Explicit Hedging

Because correlations go to 1.0 during stress, we don’t rely on “clever” cross-asset pairs. We rely on explicit hedging using options.

If we are long a cluster of high-quality commodity producers, we don’t “hedge” by shorting something else. We buy puts. This is a clean, mathematical limit on our downside. We know exactly what our “max pain” is. We don’t have to guess if the AUD/USD correlation will hold; we have a contract that pays out if the market crashes.

We sacrifice a small amount of “theoretical upside” to pay for this insurance. Why? Because as we established in Module 00, survival is the ultimate alpha.

5. From Skeleton to Reality

Now that we have the skeleton — the quantitative structure — we are ready to put some flesh on the bones. We have the math of probability (Module 00) and the structure of the portfolio (Module 01).

But what are we actually trading? Why do these clusters exist?

Next week, we move to Module 02: The Physicals (Commodity-Logic). We leave the world of data and enter the world of mines, cost curves, and the “marginal unit of production.” We will reveal why the ultimate fundamental anchor isn’t an earnings report — it’s the cost of digging a hole in the ground.

Disclaimer: This article is for educational purposes only and reflects my personal (academic) views. It does not constitute investment advice. I am sharing the architecture, not the keys to the vault.