Merchant Settlement Cycle Time Optimization: A Data-Driven Analysis of Fintech Payment Delays and Operational Efficiency

Ivy Lee3 min read·Just now

Ivy Lee3 min read·Just now--

1.0 Executive Summary

The Problem

- The average settlement cycle of a platform was 174 hours (about 7.5 days), which may affect operating cash flow and overall experience for merchants, especially small businesses.

The Insight

- After analyzing more than 2,900 transactions, I found that the main issue was not high-value transactions. Instead, many low-value transactions (below $500) were delayed due to lengthy manual Anti-Money Laundering (AML) reviews and month-end reconciliation backlog.

The Impact

- I simulated a 7-day (168-hour) Service-Level Agreement (SLA) limit for manual reviews using DAX in Power BI. The simulation reduced the overall average settlement time by more than 25 hours, showing how operational improvements could improve settlement efficiency.

2.0 Business Context & Objective

In digital payment platforms, the effectiveness of settlement is an important factor that affects merchant satisfaction and retention. This project uses a real world e-commerce dataset to study the causes of settlement delays and identify areas for operational improvement.

The objective of this project is to:

- analyze settlement cycle patterns,

- identify operational bottlenecks,

- and evaluate possible optimization strategies using data visualization and simulation techniques.

Tool Used

- Excel — Data Cleaning & Preparation

- Power BI — Data Visualization & Dashboard Development

- DAX — KPI Calculation & Scenario Simulation

3.0 Bottleneck Analysis

Insight 1: Month-End Settlement Congestion

Analysis

- The trend analysis shows that settlement delays increased significantly near the end of the month, reaching more than 330 hours around September 30.

Business Interpretation

- This may be caused by high transaction volumes during peak periods, leading to reconciliation backlog between the payment platform and banking partners.

Insight 2: Low-Value Transactions Experienced Unexpected Delays

Analysis

- The scatter plot shows that many extreme delays (more than 300 hours) came from low-value transactions rather than large transactions.

Business Interpretation

- This suggests that some low-value transactions may have triggered manual fraud or AML reviews, especially for new or smaller merchants. As a result, review resources were heavily used on transactions with lower business value.

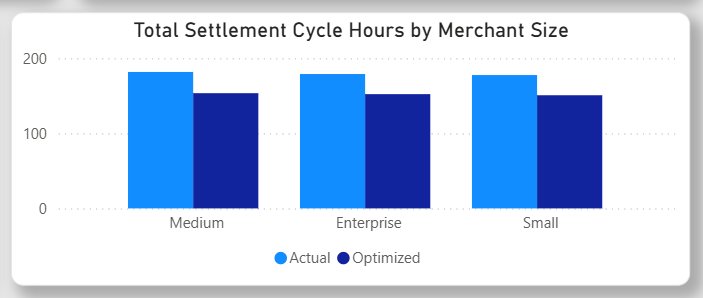

4.0 Optimization Simulation: 168-Hour SLA Limit

Proposed Solution

Using DAX, I created a simple simulation model to test the impact of introducing:

- AI-assisted risk scoring,

- and a maximum 168-hour SLA for manual reviews.

Results

The optimized scenario showed a noticeable reduction in settlement waiting time across all merchant groups.

The findings suggest that reducing extreme long-delay cases can improve overall settlement performance more effectively than increasing overall processing capacity.

5.0 Recommendations

Based on the analysis, several operational improvements are recommended:

Smart Routing & Micro-Batching

Distribute settlement processing more evenly during month-end periods to reduce reconciliation congestion.

Risk Rule Adjustment

Use AI-assisted risk scoring to automatically approve low-risk and low-value transactions, reducing manual review workload.

Tiered Settlement Services

Offer faster settlement options such as instant payout (T+0) or next-day settlement (T+1) services for trusted enterprise merchants as a premium feature.

References:

- A Guide to Intelligent Payment Routing

- Stripe Radar: Fraud Prevention Strategies to Protect Revenue

- Stripe Tiered Settlement Services

🔗Portfolio & Interaction

- Interactive Dashboard: Click to View

- Connect with me: LinkedIn / Email