Japan Is Quietly Building Asia’s Web3 Financial Infrastructure

--

While dollar stablecoins dominate 80% of global crypto transactions, Japan is quietly building a parallel infrastructure — a yen-pegged stablecoin accessible to 100 million LINE users, backed by Sony Bank and Sumitomo Life. Here’s why this matters for Asia’s financial future.

USDT. USDC. Over 80% of global crypto transactions are settled in dollar-denominated stablecoins. The United States is extending its dollar dominance onto blockchain rails.

But quietly, from a different direction, something else is moving.

Japan.

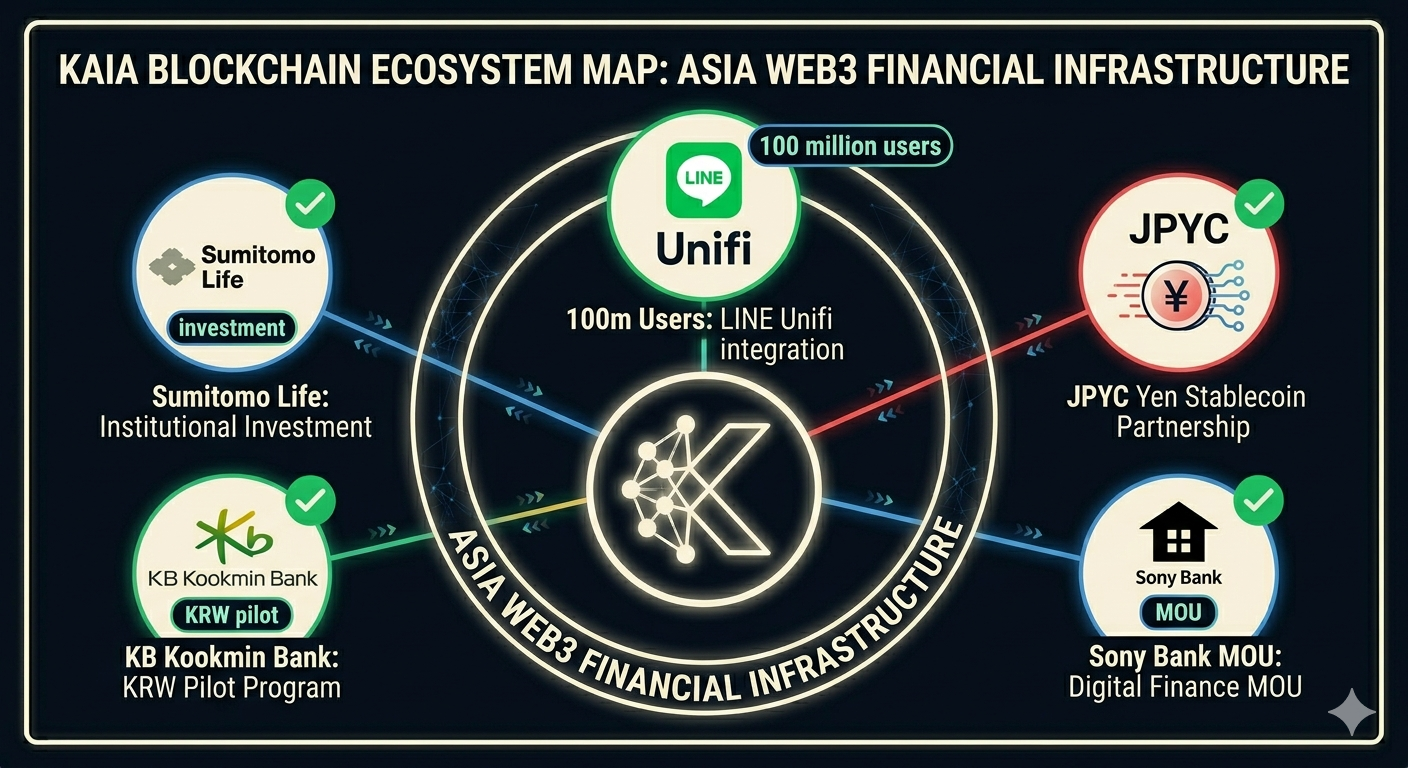

On May 22, 2026, LINE’s Web3 wallet Unifi officially added support for JPYC — Japan’s yen-pegged stablecoin. Inside the LINE app, used by over 100 million people in Japan, anyone can now pay and send money in yen, with no separate app to install.

This is not a simple technology update. Here’s why it matters.

JPYC — The Yen Stablecoin Recognized by the Japanese Government

JPYC is a stablecoin pegged 1:1 to the Japanese yen.

In August 2025, JPYC Inc. secured its Japanese Funds Transfer Service Provider license. By October 2025, it began formal issuance. This is a regulated stablecoin — recognized and approved by the Japanese government, with 100% backing in yen deposits and bonds, verified by Japan’s Financial Services Agency (FSA).

JPYC as of May 2026:

- Active accounts: 18,000 (7 months after launch)

- Unique wallet addresses: 137,000 (8x the number of accounts)

- Cumulative issuance: ¥2.5 billion+

- Total transaction volume: ¥35 billion+

- Operating chains: Ethereum, Polygon, Avalanche, Kaia

The 137,000 unique wallet addresses are significant.

There are 18,000 direct accounts — but 137,000 unique wallets. That 8x discrepancy means JPYC is actively circulating beyond JPYC Inc.’s own platform. A self-sustaining ecosystem is already forming.

LINE × Unifi — Where 100 Million People Meet Web3

LINE is not just a messaging app in Japan. It is daily infrastructure.

The way KakaoTalk is woven into Korean life, LINE is woven into Japanese life — messaging, shopping, payments, news, ride-hailing. Over 100 million users in Japan and 250 million globally use it every day.

LINE NEXT’s Unifi launched in February 2026 as a stablecoin-based wallet service. On May 22, 2026, JPYC support went live. To celebrate the launch, Unifi ran an early bird event with an 80,000 JPYC reward pool.

Unifi’s core features:

No separate app installation required. Users create a wallet directly through their LINE account. It is a self-custody model — users manage their own assets. No technical knowledge needed.

Open a wallet inside LINE. Send or receive value. Manage assets independently. No steps outside the app.

Why does this matter so much?

The biggest barrier to Web3 adoption has always been “it’s too complicated.” MetaMask installation. Seed phrase storage. Understanding gas fees. For most people, that wall was too high.

Inside LINE, you just use it. 100 million ordinary users now have the most realistic path to experiencing Web3 firsthand.

Kaia — The Blockchain Where LINE and Kakao Merged

The fact that JPYC is issued on the Kaia network is important.

Kaia is a Layer 1 blockchain formed from the merger of LINE’s Finschia and Kakao’s Klaytn — Asia’s two largest messenger ecosystems, combined onto a single blockchain.

Kaia is an EVM-compatible Layer 1 with fast transaction speeds and low fees. The JPYC integration strategically targets regions with growing yen-pegged stablecoin demand: South Korea, Indonesia, Thailand, and Taiwan.

And the Kaia story just got bigger. In May 2026, KB Kookmin Bank — South Korea’s largest bank — successfully completed a pilot of a Korean won stablecoin (KRW) for offline payments and global remittances on the Kaia network.

The combined user base of LINE and Kakao spans hundreds of millions of people across Asia. If those users transact in JPYC on Kaia, it means yen-denominated payment infrastructure is being laid across the entire region.

Sony Bank, Sumitomo Life, Metaplanet — Institutions Are Moving

JPYC’s Series B round — now fully closed at approximately ¥5 billion ($31.4 million) — drew participation from a notable group of institutional investors:

NCB Venture Capital, Tekmira Holdings, Metaplanet, Sumitomo Life Insurance (SUMISEI INNOVATION FUND), North Pacific Bank, Yokohama Capital, and others.

An MOU was signed with Sony Bank (not Sony’s entertainment arm, but Sony’s regulated banking subsidiary) for Web3 service collaboration through Sony Bank’s BlockBloom unit — exploring practical daily use cases in music, gaming, and digital payments.

The capital will primarily be used for system and application development, hiring talent for business expansion, advancing stablecoin payment infrastructure, and building M2M (machine-to-machine) payment scenarios for AI agents — the clearest signal yet of where JPYC is heading next.

How Is This Different from Dollar Stablecoins?

Let’s compare honestly.

Why dollar stablecoins grew:

The dollar is the world’s reserve currency. People in emerging markets hold dollar stablecoins to protect against their own currency’s inflation. Dollar is the default settlement unit in DeFi. The dollar is universally accepted.

The yen stablecoin’s opportunity:

The yen is not a global reserve currency. But Japan is the world’s third-largest economy. There is genuine yen-denominated payment demand in trade and tourism across South Korea, Southeast Asia, and Taiwan.

And there is one decisive difference:

Dollar stablecoins are being absorbed into the U.S. institutional structure through the GENIUS Act. JPYC was regulated and approved by the Japanese government before any of that — under Japan’s Payment Services Act, revised in 2023 to create a framework for fiat-backed stablecoins.

The legal stability is fundamentally different. Japan moved first.

AI Agents and M2M Payments — The Next Chapter

JPYC has explicitly identified M2M payment scenarios for AI agents as a core strategic direction — and its Series B capital is being directed there.

Why is this compelling?

A world is coming where AI agents buy and sell services from each other, settling automatically. If those settlements happen in yen rather than dollars, Japan could own a piece of the AI agent economy’s payment infrastructure.

Like Bittensor’s decentralized AI marketplace or Algorand’s x402 protocol, AI agent payments are likely to run on blockchain rails. JPYC is positioning to be one of those rails.

Balanced View — There Are Real Challenges

First, the yen’s global limitations.

Unlike the dollar, the yen is not a global reserve currency. JPYC can become meaningful payment infrastructure within Asia, but creating the kind of global demand that dollar stablecoins have generated is structurally more difficult.

Second, Kaia’s centralization risk.

Kaia is led by two large corporations — LINE and Kakao. Governance centralization concerns exist. Whether it qualifies as genuinely decentralized is a legitimate question.

Third, this is still early stage.

¥2.5 billion in cumulative issuance. 18,000 accounts. Impressive growth velocity — but compared to the dollar stablecoin market ($320 billion+), this remains extremely early.

Closing Thoughts

Just as dollar stablecoins became the default language of blockchain, the yen stablecoin is attempting to become the language of Asia.

LINE’s 100 million users. The Kaia blockchain — merging LINE and Kakao. Japanese government approval. Investment from Sony Bank, Sumitomo Life, and Metaplanet. KB Kookmin Bank completing a KRW stablecoin pilot on Kaia. And M2M payment infrastructure for AI agents as the next frontier.

The pieces are assembling.

Japan is quietly — but unmistakably — building Asia’s Web3 financial infrastructure. Not in dollars. In yen.

Crypto is not a trend. It is an inevitability.

History repeats itself. Only the prepared will capture the opportunity.