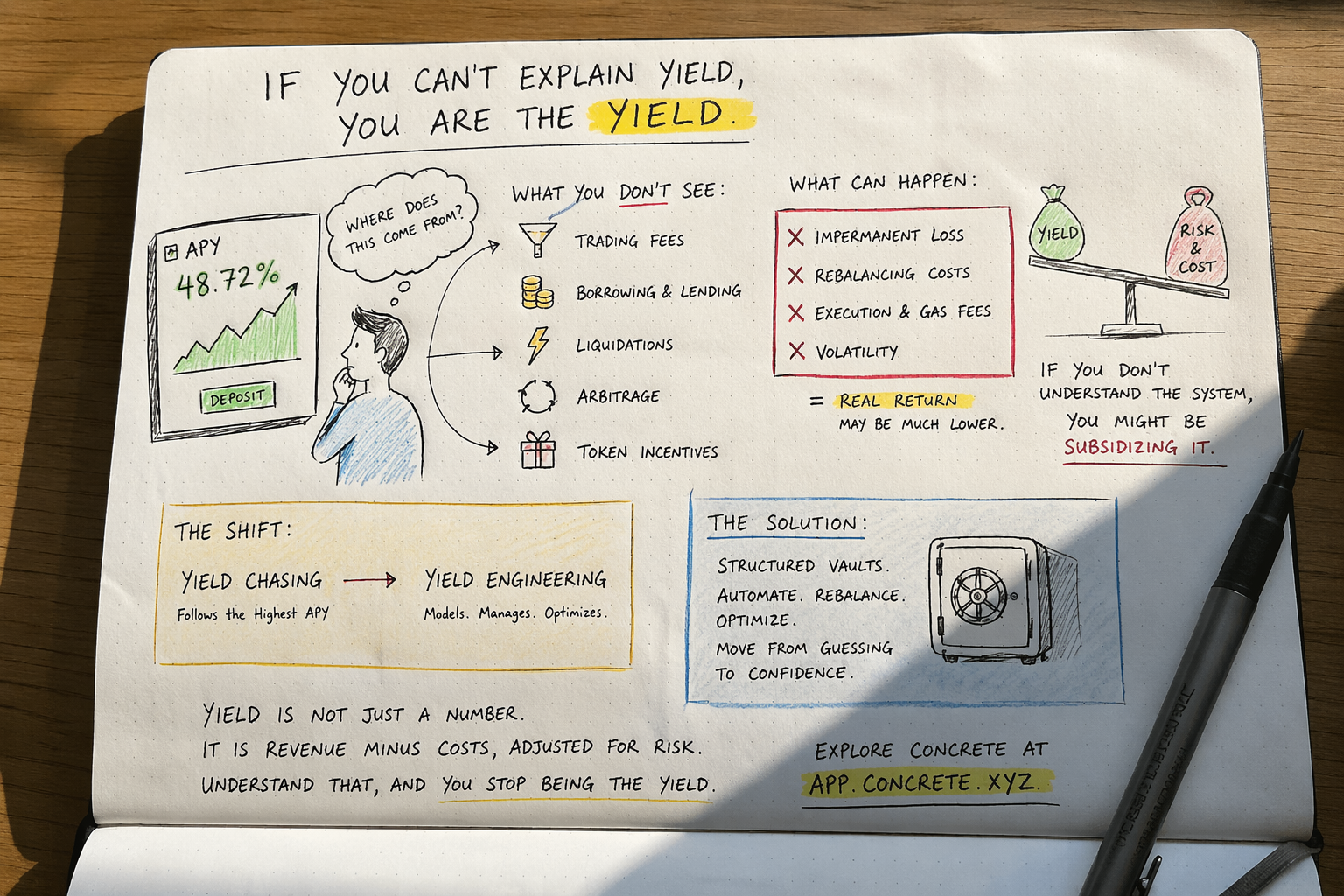

If You Can’t Explain Yield, You Are the Yield

Matrixclips7 min read·Just now

Matrixclips7 min read·Just now--

DeFi made yield visible. Every dashboard, every protocol, every vault screams numbers at you. 8.4% APY. 23.1% APR. +0.03% in the last hour. It looks transparent. It feels instant. Deposit → earn → compound. Done.

But visibility is not the same as understanding. DeFi shows you the output, not the engine. And in markets, not knowing how the engine works usually means you’re the fuel.

This week, let’s break the illusion. If you can’t explain where your yield comes from, you are the yield.

Start With the Illusion

Open any DeFi app right now. You’ll see it immediately:

- High APYs on dashboards in bold, often with three digits after the decimal for no reason.

- Simple deposit → earn flows that abstract away everything into one button.

- Minimal explanation of what happens after you click “Stake” or “Provide Liquidity.”

It’s designed to feel like a savings account with superpowers. Money goes in, bigger money comes out. The UX is clean because the complexity is hidden.

That’s the core tension: Yield looks simple on the surface, but the reality underneath is often much more complex. What you see is a marketing number. What you get is a net result after a chain of costs, risks, and value transfers you never agreed to out loud.

The Gap Between Displayed and Real Yield

The APY on your screen is almost never the APY in your wallet six months later. Here’s why:

Gross vs Net Return

Protocols quote gross yield. That’s before fees, slippage, gas, bridge costs, management fees, performance fees, and taxes. If a pool shows 40% APY and the strategy spends 15% on rebalancing, 5% on gas, and 8% on IL, your net is 12%. But you only find out by tracking it yourself.

Impermanent Loss

In AMMs, if the price of your assets diverges, the pool rebalances by selling winners and buying losers. You earn fees, but you can lose principal relative to just holding. A 50% APY can be wiped out by a 30% divergence. The dashboard rarely models this. It just shows “APY: 50%.”

Rebalancing Costs

Active strategies don’t hold positions forever. Every time a vault reweights, sells, buys, or migrates, it pays. Those costs come out of your yield. If the market is volatile, rebalancing can happen daily. The more the strategy trades, the more you pay.

Execution Friction

You’re not the only person in the pool. When a strategy enters or exits, it moves the market. Large deposits cause slippage. MEV bots sandwich transactions. You lose a few bps here and there, and it compounds negatively against you.

Volatility Impact

High APYs often come from volatile pairs. Your yield is paid in a token that’s dumping. 100% APY in a token down 60% YTD is a -20% return. But the dashboard still looks green.

Result

Displayed APY is a top-line number. Real yield is what’s left after the system takes its cut. Most users never do the subtraction, so they assume the top line is reality. That assumption is expensive.

Where Yield Actually Comes From

To judge a return, you have to source it. There are only a few real sources of yield in crypto. Everything else is just a transfer.

Trading Fees

AMM LPs earn a cut of every swap. This is real yield. Someone paid to trade, and you got a piece. It’s sustainable as long as volume exists. If volume dies, yield dies. No volume, no fees, no APY.

Lending Activity

Borrowers pay interest to lenders. You provide ETH, someone borrows it to short or farm, they pay you. This is real, but it depends on borrow demand. When markets are quiet, borrow rates collapse. When markets are frothy, rates spike.

Arbitrage

Strategies can capture price differences across venues. Perps vs spot. CEX vs DEX. This is real yield, but it’s capacity-constrained and skill-intensive. Once too much capital chases it, the edge disappears.

Liquidations

Some vaults earn liquidation bonuses. When over-leveraged positions get wiped, liquidators get paid. It’s real, but sporadic and risky. You’re monetizing someone else’s blow-up.

Incentives / Emissions

The big one. Protocols print tokens to bootstrap liquidity. You deposit, you earn their token. This isn’t yield. It’s user acquisition cost. It’s temporary, dilutive, and only valuable if someone else buys the token after you dump it.

The rule

Sustainable yield comes from economic activity. Temporary yield comes from token printers. If you can’t tell which one you’re earning, assume it’s the second. And if it’s the second, ask who’s buying. If you don’t know, it’s probably you.

The Hidden Value Transfer

Here’s where the title comes alive: If you don’t understand the system, you may be the one subsidizing it.

Markets are zero-sum before fees. For you to earn 20% without risk, someone else has to lose 20% + costs. So where’s the other side?

Providing liquidity without understanding risk

You LP into a volatile pool chasing 80% APY. A whale trades through your pool, you take the IL, they get execution. You earned fees. They got filled. Net, you paid them for the privilege.

Earning incentives while absorbing downside

A new chain launches with 300% APY on stable LPs. You move in. The yield is paid in a token with 10M daily emissions and 100k daily buy pressure. You’re earning tokens while the protocol sells the story. When emissions end, the token crashes, and your “yield” was just you buying bags with extra steps.

Participating without modeling outcomes

You see “Delta Neutral Vault” and assume safe. You don’t check how it hedges, how often it rebalances, or what happens in a gap down. Funding flips negative, the hedge costs money, the vault lags, and you’re down 8% while the APY still says 15%.

You weren’t investing. You were the counterparty. The system used your capital to function, and it paid you just enough to keep you there.

Why Outcomes Differ

Two people can use the exact same protocol and get wildly different results. The system is the same. The understanding isn’t.

Some users optimize for APY

They sort by “highest return,” deposit, and check back in a month. They’re exposed to every risk we listed above with no hedges, no thesis, and no exit plan. They are exit liquidity for people who do the work.

Others analyze structure, cost, and risk

They ask: What’s the gross vs net? How often does it rebalance? What’s the IL under 2x price move? Who pays me, and why? They size positions based on answers. They pass on 80% APY if the math doesn’t work and take 6% if it does.

Institutions model before deploying capital

Funds don’t YOLO into farms. They model expected value, stress test volatility, simulate fees, and compare net Sharpe ratios. They treat DeFi like a portfolio of businesses, not a casino. That’s why they can run the same strategy and outperform retail by 3x.

Same system, different outcomes. The difference is understanding. Yield isn’t found. It’s engineered.

The Shift: From Yield Chasing → Yield Engineering

The first wave of DeFi was about access. Anyone could earn. The cost was that no one knew what they were earning.

The next wave is about precision. Users and protocols are moving from chasing the biggest number to engineering the best risk-adjusted outcome.

Yield engineering means

- Modeling expected outcomes: Not “what’s the APY,” but “what’s the distribution of returns if ETH +30%, -30%, or sideways?”

- Managing risk: Setting bounds on IL, drawdown, and correlation. Using hedges where it makes sense.

- Optimizing over time:Rebalancing based on volatility regimes, not just compounding blindly.

- Focusing on net returns:Obsessing over the number that hits your wallet, not the number on the homepage.

This is how TradFi has always worked. A bond desk doesn’t buy bonds because the coupon is high. They buy because yield minus expected default minus rate risk minus cost = acceptable. DeFi is just catching up.

Concrete Vault Infrastructure

So how do you actually do this without a quant team? That’s where infrastructure matters.

Concrete Vaults are built for engineered yield. They remove the manual work and guesswork that causes most of the value leakage above.

Concrete Vaults can:

- Automate allocation: Route capital to strategies based on real-time conditions, not static APY rankings. If borrow demand drops, it moves. If fees dry up, it exits.

- Manage strategies: Handle the complexity of multi-leg positions. Delta-neutral, leveraged looping, cross-chain—executed programmatically so you don’t have to.

- Rebalance positions:Adjust exposure when volatility, liquidity, or rates change. You avoid being stuck in a position that made sense last month but not today.

- Reduce manual errors: No more mis-clicks, no more forgotten approvals, no more 3am liquidations because you didn’t check health factor.

This allows users to move from guessing → structured exposure. You’re no longer picking farms. You’re setting risk parameters and letting the vault execute a plan. The APY you see is closer to the APY you get, because the costs are modeled upfront.

Explore Concrete at http://app.concrete.xyz

The Core Insight

We need to rewrite how we think about yield. It’s not a number on a website. It’s a formula:

Yield = Revenue – Cost – Risk

Revenue: Fees, interest, arb, liquidations. Real economic activity.

Minus Cost: Gas, rebalancing, management fees, slippage, MEV, bridge fees.

Adjusted for Risk: IL, volatility, smart contract risk, depeg risk, regime risk.

Only after all three are accounted for do you have “yield.” Everything else is marketing.

Understanding that changes how you approach DeFi entirely. You stop asking “What’s the APY?” and start asking “Who pays me, why, and what could go wrong?” You stop being the product and start being the operator.

Because in markets, there’s always someone on the other side of the trade. If you can’t explain yield, you are the yield.

Explore Concrete at http://app.concrete.xyz and start engineering instead of chasing.