Pragya Kumari6 min read·Just now

Pragya Kumari6 min read·Just now--

Imagine this. You've just landed a freelance client in Germany.

They’re excited, you’re excited, and they ask for your bank details to send the first payment. You fire off your account number and sort code.

A week passes and then two. You follow up, they say the transfer went through, but the money is nowhere. It’s sitting in a limbo between two banking systems that couldn’t quite agree on who you are or where your money belongs.

This frustratingly, is a story that millions of people still live through every year. And most of this friction the delays, the failures, the ghost payments, could have been avoided with one thing. An IBAN.

What Exactly Is an IBAN?

IBAN stands for International Bank Account Number. But don’t let the bureaucratic name put you off the idea behind it is elegantly simple.

Think of it as a postal address for your money.

When you mail a letter, the postal system needs more than just a name on the envelope.

It needs a street, a city, a postcode, a country. Without that structure, your letter might end up in the wrong pile, the wrong sorting office, or not delivered at all. Traditional bank account numbers are like writing "John, Block 4" on an envelope and hoping for the best. They work fine locally, where everyone already knows the context. But send that internationally, and the system quietly falls apart.

IBAN was designed to fix exactly that. It creates a standardized, universally readable format for bank accounts one that carries all the information any bank anywhere in the world needs to route your money correctly, without confusion, without ambiguity.

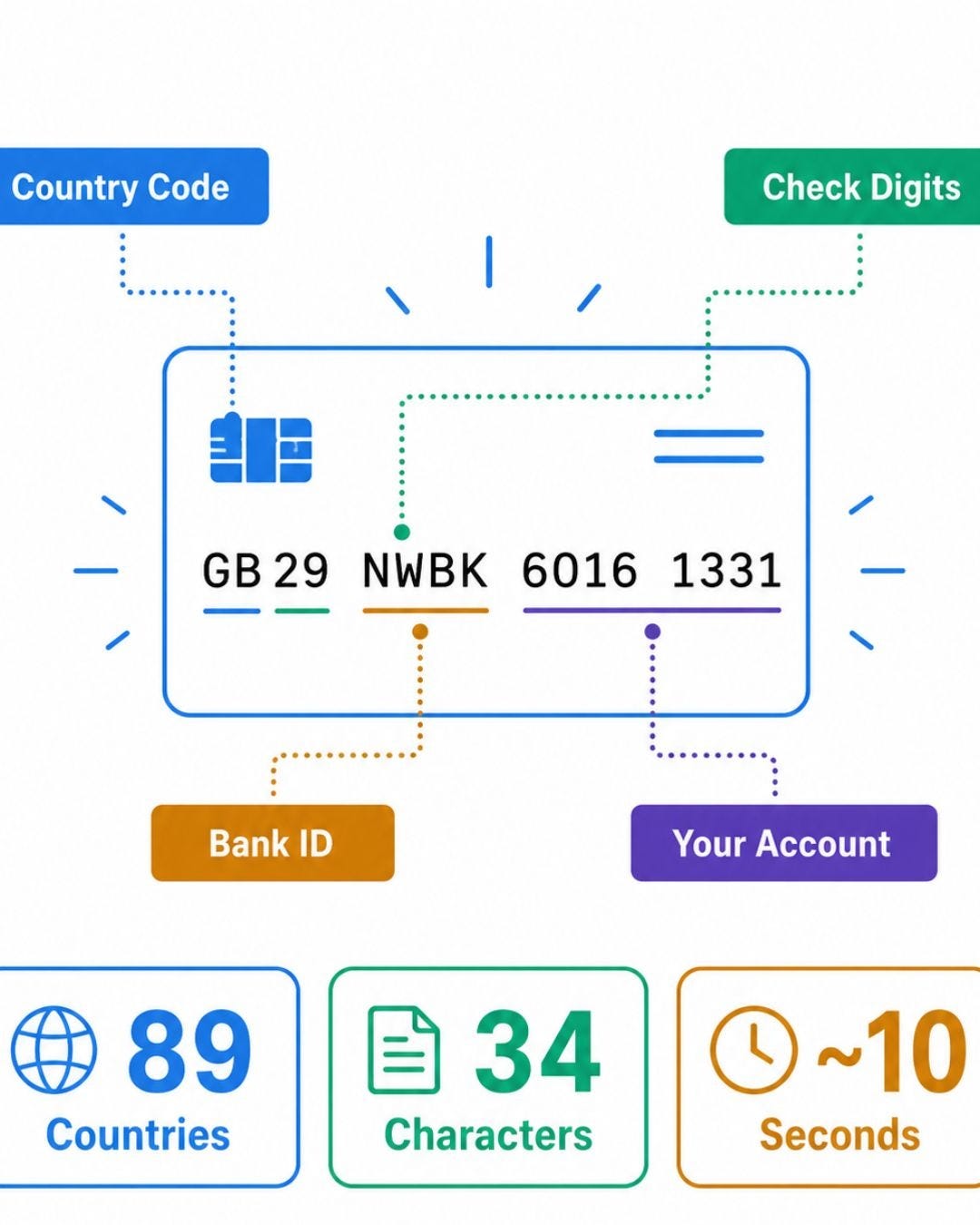

A typical IBAN say, a British one looks like this: GB29 NWBK 6016 1331 9268 19. Behind those characters is a precise logic.

The first two letters are the country code. The next two digits are check digits, used to automatically validate the number before any money moves. After that comes the bank identifier, the branch code, and finally the individual account number. It’s compact, structured, and every single part of it means something.

Why IBAN Exists And Why It Matters More Than Ever

IBAN wasn’t invented in a Silicon Valley garage. It was developed by the International Organization for Standardization and the European Committee for Banking Standards in the late 1990s, primarily to make payments within Europe faster and less error-prone. Europe adopted it broadly, the EU made it mandatory, and cross-border payments within the eurozone became dramatically smoother almost overnight.

But here’s what makes IBAN more relevant today than ever, the world has gone global in ways that nobody in 1997 fully anticipated.

The cross-border payments market which handles everything from your freelance invoice to multinational corporate treasury movements, was worth over $194 trillion in 2024, and forecasts suggest it could reach $320 trillion by 2032. Remote work, global e-commerce, the gig economy, diaspora remittances, international real estate and money moves across borders constantly now, and in volumes that would have seemed extraordinary a generation ago.

Yet despite this explosion in volume, international transfers have historically been slow, expensive, and surprisingly error-prone. A wrong digit here. A mismatched bank identifier there. A payment bouncing back after four days with a terse automated message and a handling fee.

IBAN tackles the error problem at its root: by standardizing how accounts are identified and building in automatic validation, it dramatically reduces the rate of failed payments before they even leave your bank.

How IBAN Actually Works

Here’s the elegant part most people never learn: IBAN doesn’t just store your account details, it validates them in real time.

Those two check digits in every IBAN aren’t decorative. They’re calculated using a specific mathematical algorithm called MOD-97. When your bank or a payment platform receives an IBAN, it can instantly run that calculation and know, before attempting the transfer, whether the number is structurally sound. It doesn’t guarantee the account exists but it immediately catches typos, transpositions, and copy-paste errors that would otherwise cause a failed transfer days later, costing everyone time and money.

The total length of an IBAN varies by country a UK IBAN is 22 characters, a German one is also 22, a Saudi Arabian one stretches to 24 but all of them follow the same logical order country code, check digits, then the domestic bank account details packed neatly behind them. Every country registered its own internal format, but all of them plug into the same global recognition system. Any bank, anywhere, can read any IBAN and know exactly what it’s looking at.

IBAN vs. The Old Way

Traditional Account Numbers Break Down Internationally

In the UK, a domestic payment needs an account number and a sort code. In India, you need an account number and an IFSC code. In the US, it’s an account number and a routing number.

In Germany, historically, it was a Kontonummer and a Bankleitzahl. Every country invented its own system, and none of them naturally speak the same language when money crosses a border.

When payments move between these systems without IBAN, banks rely on what’s called correspondent banking a slow, expensive chain of intermediary institutions, each adding a processing day and sometimes a fee.

Instructions get lost between systems. Formatting differences cause automatic rejections. The payment you sent on Monday might land on Friday, or come back to you with an unhelpful error code and no real explanation.

With IBAN, the receiving bank’s details are unambiguous. The structure tells any bank in the world exactly which country’s system to reference, which bank to contact, and which account to credit. No translation is needed, no guessing, no back-and-forth between compliance teams. The whole chain gets shorter, faster, and cleaner.

The Future: IBAN Is Evolving, Not Disappearing

Here’s the question that floats around fintech circles, with blockchain, stablecoins, and new instant payment rails all emerging, does IBAN eventually become obsolete?

The honest answer is probably not at least not for a long time, and perhaps never entirely. What’s far more likely is integration and evolution rather than replacement.

IBAN is already being layered into next-generation payment infrastructure.

The EU’s SEPA Instant system, which processes euro payments in under ten seconds across 36 countries, runs on IBANs as its core identifier. SWIFT’s Global Payments Innovation initiative, which has dramatically cut international wire transfer times from days to hours, still relies on IBANs at the centre. And virtual IBANs, digital account numbers issued by fintech companies rather than traditional banks are rapidly becoming one of the most powerful tools for globally operating businesses in 2025 and 2026.

They allow companies to collect payments internationally in local currencies, with all the structured routing of a real IBAN, without needing to open a physical bank account in every country they operate in.

Blockchain and real-time payment networks will keep pushing the boundaries of what’s possible. India’s UPI, Brazil’s Pix, and Singapore’s PayNow are beginning to connect internationally in pilot programs, imagining a future of truly instant global settlement. But even these systems need a way to identify accounts cleanly and unambiguously.

The thinking behind IBAN structured, validated, universally readable is precisely the model they’re building on.

The infrastructure of global finance is changing fast. The principle behind IBAN isn’t going anywhere.

Conclusion

The Invisible Systems that Run the World

Most of the things that make modern life work are invisible. The protocols that route your emails across continents in milliseconds.

IBAN is doing silent, diligent work in the background.

In a world where money needs to move as freely as ideas, IBAN is less a technicality and more a piece of fundamental global infrastructure. A small, invisible passport that your money carries on every international journey it takes.

You might never think about it again after today. But now, at least, you’ll know it’s there.

Enjoyed this? Follow for more plain-English explainers on the systems quietly shaping global finance.