HYPE: When Unlocks Do Not Become Float

COSMODROME Research5 min read·Just now

COSMODROME Research5 min read·Just now--

The next question is no longer whether Hyperliquid is strong. The next question is whether HYPE’s price is being formed by a market with genuinely independent float.

Hyperliquid can be praised for many reasons.

High execution speed.

Deep liquidity.

Clean user experience.

For an active trader, it is one of the most efficient DEX environments in the market.

But for an institutional investor, that is not the first question.

The first question is different:

How independently is HYPE actually priced if its effective float may be materially narrower than a surface reading of its tokenomics suggests?

This article does not claim that manipulation has already been proven.

It makes a narrower and more serious point:

there is already enough evidence to question the full independence of HYPE’s price formation, because the formal supply schedule, the actual expansion of float, staking dynamics, and the surrounding supply narrative may be more closely linked than they appear on the surface.

For traders, it is execution. For institutions, it is price formation.

Markets naturally evaluate Hyperliquid through usability.

That is understandable.

Where speed, spreads, and order-book depth matter most, Hyperliquid looks strong.

But institutions are not buying convenience.

They are buying:

- exposure to the token

- dependence on supply behavior

- dependence on real rather than nominal float

- risk under large capital entry and exit

That shifts the question.

Not:

“How good is the product?”

But:

“How independently is the asset we are buying actually priced?”

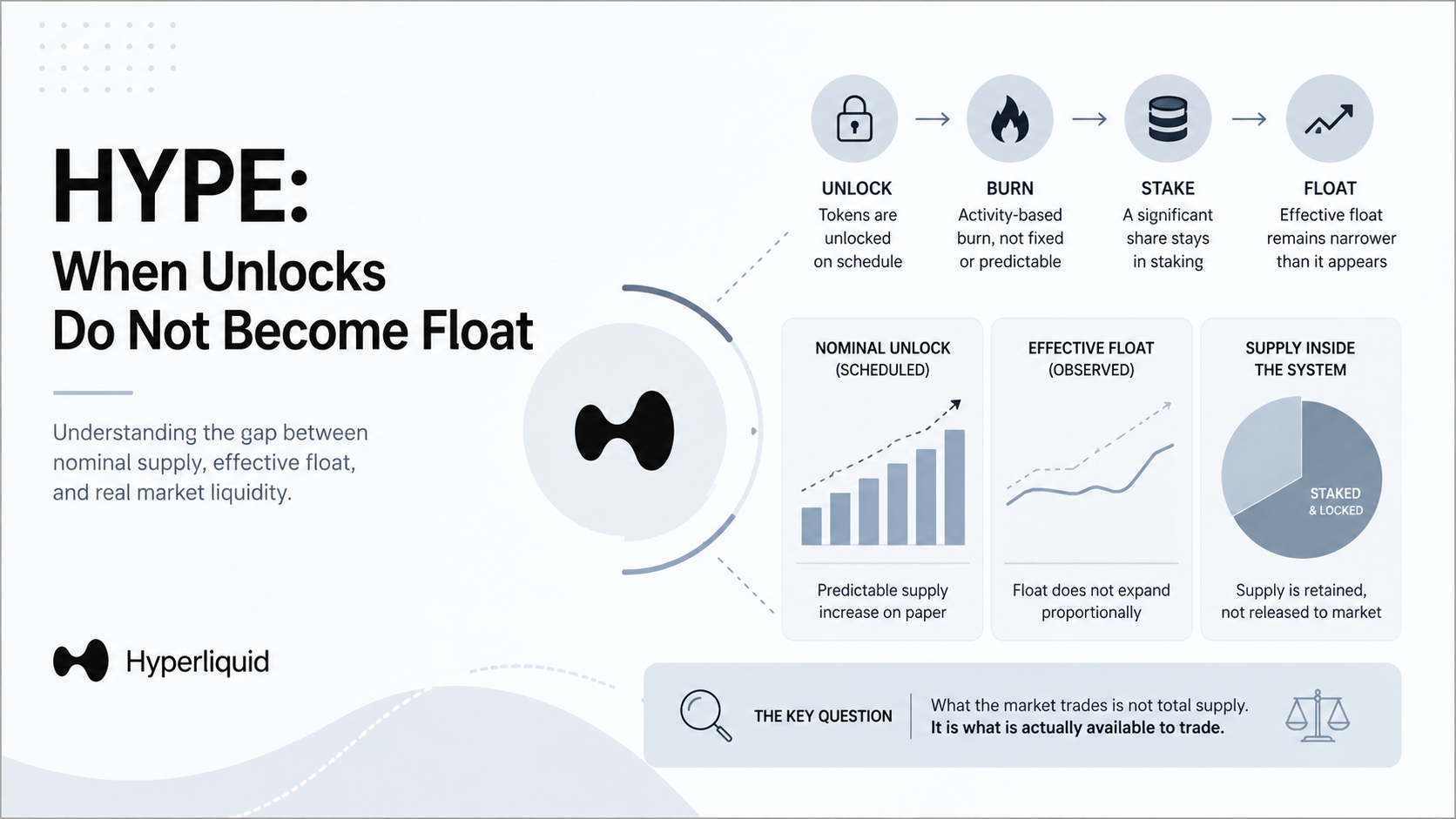

A formal schedule is not the same as market supply

On paper, HYPE has a defined unlock schedule.

But markets do not trade schedules.

They trade supply.

Observed data suggests that post-cliff token claims have remained significantly below the formal monthly schedule.

This no longer looks like a one-time adjustment.

It appears to be a repeated behavioral pattern.

By itself, that does not imply wrongdoing.

But it changes the analytical frame.

Because once that happens, the market is no longer governed by the whitepaper schedule alone.

It becomes dependent on the behavior of a relatively small group of holders who effectively determine how much supply reaches the market at any given time.

The point is not that tokens are being sold less.

The point is more fundamental:

a formal schedule may exist, but actual market supply may be shaped not only by that schedule, but by discretionary holder behavior.

When an unlock does not become float

This is the central issue.

Markets often collapse several distinct concepts into one:

- unlocked supply

- circulating supply

- tradable liquidity

- effective float

But they are not the same.

A token can be unlocked.

It can be counted as circulating.

And still fail to translate into real market supply at the expected scale.

That appears to be the emerging pattern.

Unlocks occur,

but float does not expand proportionally.

At the same time:

- staking participation continues to grow

- a meaningful share of supply appears to remain within the system

- incremental sell-side pressure remains limited

This is not enough to conclude:

“price is manufactured.”

But it is enough to ask a more precise question:

what exactly is the market trading — a fully released asset, or a structurally constrained float?

A May signal: the pattern continues

Recent developments reinforce this observation.

A new unlock event in early May introduced nominal supply under the vesting schedule.

Yet market behavior did not reflect a proportional increase in tradable liquidity:

- no clear surge in sell-side pressure

- no meaningful expansion of float

- relatively stable price dynamics

This does not establish coordination.

But it matters for a different reason:

the pattern repeats.

And repetition shifts the discussion from anomaly to structure.

Unlock vs Burn: a balance that remains unclear

A common counterpoint is the presence of burn mechanisms.

Indeed, the system includes:

- fee-driven buybacks

- token burn flows

- a broader deflationary narrative

However, an important analytical gap remains.

Unlocks are:

- scheduled

- quantifiable

- structurally predictable

Burn is:

- activity-dependent

- variable in scale

- not fixed on a monthly basis

This leads to a simple but critical observation:

there is no clear evidence that ongoing burn consistently offsets the scale of nominal unlocks.

This is not an accusation.

It is a transparency question.

Because the market hears:

“supply is being reduced”

But does not receive a precise answer to:

“to what extent does that reduction balance new supply?”

Supply may remain inside the system

Another structural detail becomes relevant.

If unlocks do not translate into expanded liquidity,

then the question becomes:

where does that supply go?

Observed dynamics suggest that a meaningful share of unlocked tokens may not exit into open market circulation, but instead remain within the system.

At the same time:

- staking participation expands

- locked balances increase

- tradable supply does not expand proportionally

This does not imply intent.

But it establishes a structural reality:

unlocked supply does not necessarily become market supply.

Effective float may be narrower than it appears

If:

- unlocks do not expand float

- staking continues to grow

- supply remains retained

then a strong hypothesis emerges:

the market may be trading a materially narrower effective float than nominal supply figures suggest.

This is a critical shift.

Because price is not determined by how many tokens exist.

It is determined by how many tokens are actually available to trade.

The risk is not any one factor — it is their interaction

Each element alone is not unusual:

- low claims can reflect discipline

- staking is a standard mechanism

- burn is common

- narrative is part of markets

The issue emerges when these elements move together.

If within the same system we observe:

- constrained supply release

- continued staking growth

- value capture mechanisms

- reinforced scarcity narratives

then the question is no longer about any single signal.

It becomes:

how independently are supply, expectations, and price formation evolving?

What this means for institutional investors

Institutions do not rely on surface signals.

It is not enough to see:

- a strong product

- rising metrics

- yield

- scarcity narratives

They need to understand:

- the true breadth of float

- the dependence of supply on holder behavior

- who benefits from constrained liquidity

- how price behaves if that constraint changes

At this point, HYPE is no longer just the token of a strong venue.

It becomes something more complex:

an asset that may be priced as if it were freely discovered, while its effective float may remain structurally constrained.

This is not a retail concern.

It is a risk committee concern.

Conclusion

We have not proven manipulation.

But we have reached a more important question:

how independent is HYPE’s price formation if the market is receiving not a neutral flow of supply, but a behaviorally constrained version of it?

Because HYPE may indeed be priced by the market.

But its effective float may still be shaped by a much narrower circle.

Continuation follows

The next part will look at how retained supply and system dynamics interact over time — and what that may mean for where influence accumulates and how price formation responds under stress.