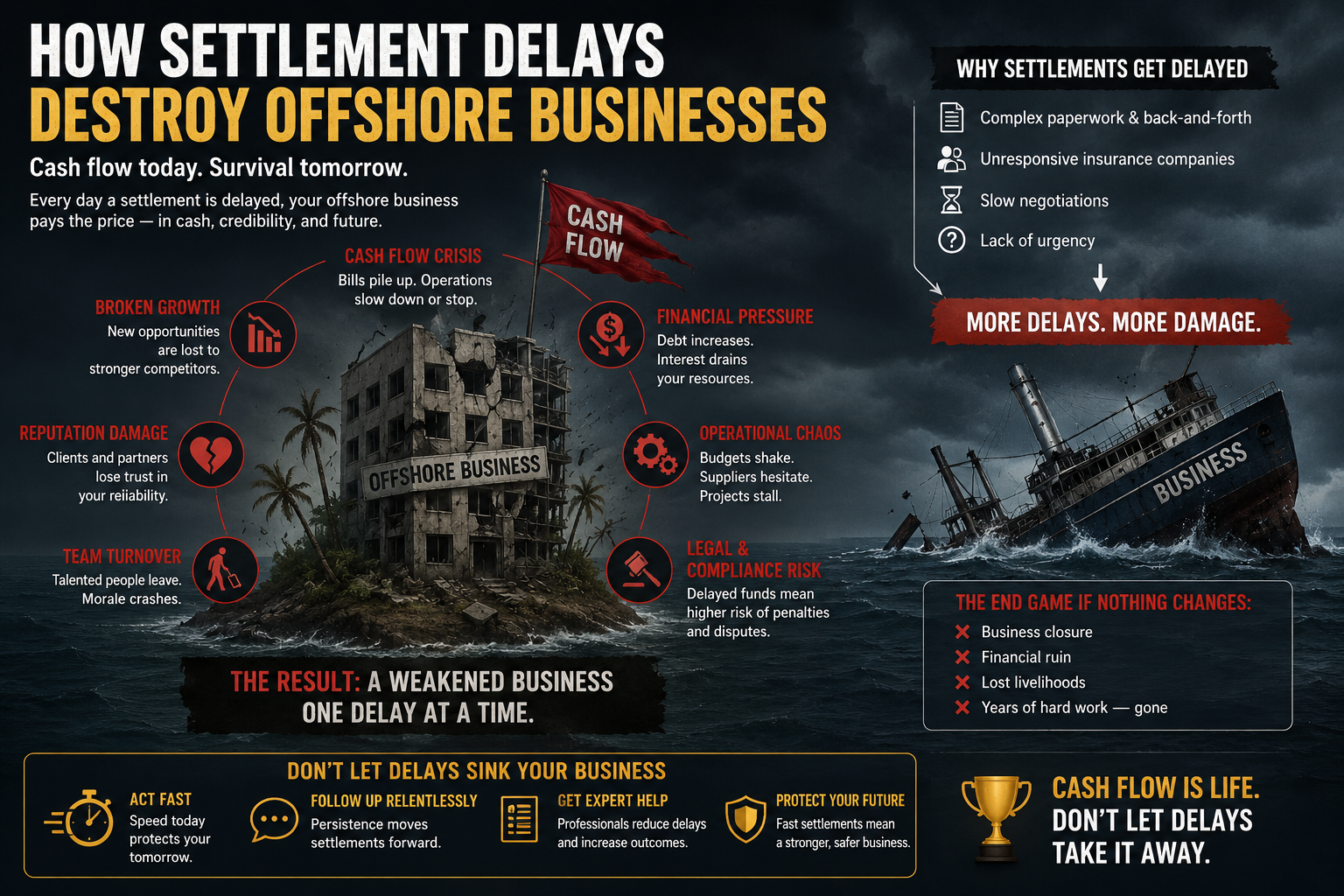

How Settlement Delays Destroy Offshore Businesses

--

Processing revenue you cannot access is not revenue. It is a loan you have made to your processor — one with no defined repayment schedule, no interest rate, and no enforcement mechanism available to you. Settlement delays in offshore processing are not an inconvenience. At scale, they are a business-ending structural problem.

Cash flow is the circulatory system of any business. Revenue generated but not accessible is, for operational purposes, identical to revenue not generated at all. You cannot pay payroll with a reserve balance sitting in an offshore processor’s custody account. You cannot fund marketing campaigns with settlement funds pending a clearing cycle that runs on a different continent. You cannot invest in product development with money that technically belongs to you but practically belongs to your processor until they decide to release it.

Settlement timing is one of the least-discussed and most operationally destructive features of offshore payment processing. Merchants who evaluate offshore arrangements primarily on rate comparisons and approval rate projections — treating settlement timing as a secondary detail to be managed after the main decisions are made — often discover, at meaningful processing volumes, that the settlement gap is the variable most directly determining whether the business can function day to day. Understanding the specific mechanisms that create settlement delays in offshore processing, and how those delays compound into existential operational problems, is the foundation for structuring offshore arrangements that actually support business operations rather than undermining them.

How Offshore Settlement Timelines Work

Domestic payment processing in mature markets has normalised settlement timelines of one to two business days. A transaction processed today settles to the merchant’s bank account by tomorrow or the day after. This speed is the product of direct, well-established relationships between domestic acquirers and domestic banking infrastructure — relationships built on decades of operational development, regulatory standardisation, and settlement infrastructure investment.

Offshore settlement operates through a fundamentally different chain. The transaction is authorised in real time, but the settlement — the actual transfer of funds from the acquiring bank to the merchant’s account — passes through multiple steps that compound into material delays: the offshore acquiring bank’s internal settlement batch processing, currency conversion to the settlement currency, wire transfer initiation through the correspondent banking system, clearing through the correspondent network, and final posting to the merchant’s receiving account. Each step in this chain adds time. Typical offshore settlement timelines range from three to seven business days in well-structured arrangements. In less-structured or more geographically complex arrangements, weekly or biweekly settlement is common — and in some arrangements, settlement timing is effectively at the processor’s discretion.

For a business processing $200,000 per week, the difference between next-day settlement and weekly settlement is approximately $800,000 in outstanding receivables at any given time — funds that have been earned, that appear as revenue in transaction reports, but that are not available for operational deployment. This receivables gap is not a rounding error in working capital management. It is a structural cash flow constraint that grows proportionally with volume, meaning that the faster the business grows, the larger the inaccessible capital pool becomes relative to operational needs.

The Compounding Effect of Rolling Reserves on Settlement

Settlement delays are not the only offshore working capital drain — they compound with rolling reserve requirements that are standard in offshore arrangements. A 10% rolling 90-day reserve withheld from a business processing $500,000 per month means approximately $150,000 in reserve balance at any given time — capital that legally belongs to the merchant but is practically inaccessible for 90 days from each transaction date.

The interaction between settlement delays and rolling reserves creates a combined working capital gap that grows non-linearly as volume scales. A business processing $500,000 per month with a five-day settlement timeline and a 10% rolling 90-day reserve has approximately $330,000 in combined outstanding settlement and reserves at any given time. Scale that business to $1,000,000 per month and the combined outstanding amount approaches $700,000. This is capital that the business has earned, that its product delivered, and that its customers paid — but that is functionally unavailable to the business at the scale where access to capital matters most for growth investment.

The reserve component compounds the settlement delay problem in a second way: reserves withheld during a settlement delay period accumulate without the offsetting effect of reserves being released simultaneously. A business that is growing rapidly may find that the reserves building from new transactions are not offset by the release of reserves from older transactions, creating a period of net capital drain even as revenue is nominally growing. This dynamic — where apparent business growth produces worsening cash flow — has ended businesses that never understood the reserve-settlement interaction until it was too late to manage.

When Settlement Delays Become Settlement Failures

The operational burden of predictable settlement delays, while significant, is manageable with careful cash flow planning. What converts settlement delays from a planning challenge into a business crisis is when delays become failures — when expected settlement does not arrive on schedule and the merchant has no reliable information about when it will.

Settlement failures in offshore processing happen for several documented reasons. Correspondent banking disruptions — where the offshore acquiring bank’s relationship with its international clearing bank is interrupted — can strand funds between institutions for days or weeks while alternative settlement pathways are established. Compliance holds initiated by the offshore bank’s AML monitoring can freeze settlement for the duration of a review process with no defined timeline. And account termination events — when the offshore relationship is ended for any reason — typically result in all pending settlement being placed in a hold pending compliance clearance, a process that routinely takes weeks to months in offshore arrangements.

The pattern is consistent across merchant experiences: a business that has been operating normally, processing normally, and expecting normal settlement finds that a settlement due on Tuesday has not arrived. Inquiries to the ISO or processor produce vague references to ‘processing delays’ or ‘compliance review.’ Days become weeks. The merchant’s operating accounts run down. The processor eventually confirms that the funds are ‘under review’ with a timeline that remains undefined. The business cannot pay its obligations without access to its own revenue, and the offshore arrangement that was supposed to provide stable payment infrastructure has instead produced a capital trap with no defined exit.

Structuring for Settlement Resilience

Merchants who successfully operate with offshore processing build their business models around the reality of settlement timelines rather than against it. This means maintaining operating capital reserves sufficient to cover the maximum expected settlement gap — not the average gap, but the worst-case gap that would result from a two-to-four-week settlement delay during a high-volume period. It means establishing domestic payment processing capacity alongside offshore infrastructure so that domestic revenue provides near-term cash flow while offshore settlement processes on its longer timeline. And it means negotiating settlement terms explicitly in the merchant agreement — with defined maximum settlement periods and defined consequences for delays — rather than accepting the processor’s standard terms that typically give the bank extensive discretion over settlement timing.

Choosing offshore partners whose settlement infrastructure is demonstrably reliable — partners with verifiable correspondent banking relationships, documented settlement track records, and transparent communication about settlement status — is settlement resilience in the partner selection dimension. A processor that offers excellent rates but uncertain settlement timing is offering a worse deal than one with standard rates and reliable daily settlement. The cash flow modelling that demonstrates this is straightforward: the financing cost of carrying the additional receivables created by settlement delay, combined with the operational risk cost of settlement unpredictability, consistently exceeds the rate savings of a delayed-settlement arrangement at any meaningful processing volume.

Settlement timing is not a technical detail in offshore payment processing. It is the mechanism by which processing revenue becomes accessible capital — and in offshore arrangements, that mechanism is far less reliable, far slower, and far less protected than merchants typically plan for. The businesses that build offshore payment operations with settlement timing as a primary design consideration consistently outperform those that add settlement management as an afterthought when the delays have already become a crisis.

Model your settlement gap explicitly. Negotiate your settlement terms contractually. Maintain the capital buffer that covers the worst-case scenario. And choose offshore partners whose settlement reliability is verifiable rather than assumed. Settlement is not the most interesting dimension of payment processing — but in offshore operations, it is frequently the dimension whose failure destroys the business.