From Diffusion to Jumps: Lévy Model in Finance

Ibrahim Lanre Adedimeji7 min read·Just now

Ibrahim Lanre Adedimeji7 min read·Just now--

Financial markets do not always behave the way simple models suggest. Prices do not move smoothly all the time, and they do not follow the clean and continuous patterns assumed in the Black Scholes model. In reality, markets often experience sudden changes caused by things like earnings announcements, economic news, or liquidity issues. These events can lead to sharp and unexpected movements in prices.

This gap between theory and reality has been a major challenge in quantitative finance. While geometric Brownian motion is easy to work with mathematically, it does not capture important features seen in real market data, such as extreme movements, asymmetry, and sudden jumps. Because of this, models that rely only on continuous price changes tend to underestimate risk, especially during volatile periods.

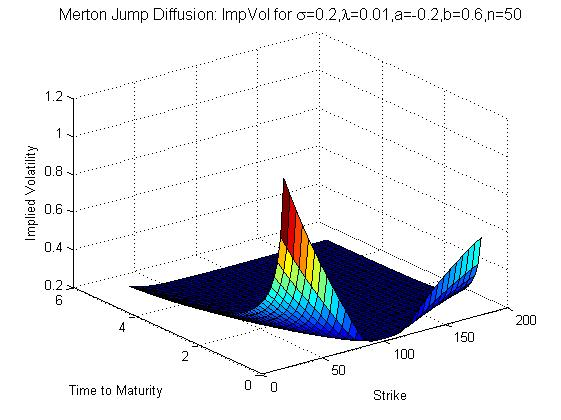

To improve on this, jump diffusion models were developed to include sudden changes in price. However, these models can still be limited when the behavior of jumps becomes more complicated or happens more frequently. This leads to a more general and flexible framework known as Lévy processes.

Lévy processes extend classical models by allowing a wider range of jump behavior. They can capture both rare large movements and many small fluctuations. By combining continuous movement with jumps, they offer a more realistic way to describe how asset prices evolve.

In this article, we will look at how Lévy jump models help us better understand financial markets. We will introduce the basic ideas behind these models and discuss how they are used in areas such as option pricing and risk management.

Mathematical foundations :

Lévy Processes: Introduction

A stochastic process X = (Xₜ)ₜ≥₀ is said to have càdlàg paths if almost all its

sample paths are càdlàg — that is, continuous from the right with limits from the

left (from the French: continu à droite, limites à gauche).

Definition: Lévy Process

A real-valued process L = (Lₜ)ₜ≥₀ defined on a probability space (Ω, ℱ, ℙ) is

called a Lévy process if it satisfies the following conditions:

(i) Initialization

L₀ = 0 ℙ-almost surely

(ii) Independence of Increments

For all 0 ≤ t₁ < t₂ < ··· < tₙ, the increments

Lₜₙ − Lₜₙ₋₁ , … , Lₜ₂ − Lₜ₁

are independent random variables.

(iii) Stationarity of Increments

For all s < t, the increment Lₜ − Lₛ has the same distribution as Lₜ₋ₛ:

Lₜ − Lₛ ᵈ= Lₜ₋ₛ

(iv) Continuity in Probability

For every ε > 0 and every s ≥ 0:

lim ℙ( |Lₜ − Lₛ| > ε ) = 0

t → s

(v) Càdlàg Paths

L has càdlàg sample path : almost surely, the map t ↦ Lₜ(ω) is right-continuous

and possesses left-hand limits at every t > 0:

Lₜ₋ := lim Lₛ exists for all t > 0, ℙ-a.s.

s↑t

Note on the Conditions

Conditions (ii) and (iii) are the structural heart of the definition. Together they

imply that the law of L is completely determined by the one-dimensional marginal L₁,

since for any t ≥ 0:

n

Lₜ ᵈ= Σ ( Lₖₜ/ₙ − L₍ₖ₋₁₎ₜ/ₙ )

k=1

where each summand is i.i.d. with the same law as Lₜ/ₙ. This makes Lₜ infinitely

divisible for each fixed t.

Condition (iv) rules out fixed-time jumps — it does not, however, preclude

random-time jumps, which are a defining feature of Lévy processes. Condition (v) is

a regularity requirement on the paths: at any jump time τ, we have Lτ ≠ Lτ₋, and

the jump size is defined as:

ΔLτ := Lτ − Lτ₋

Example 1: Brownian Motion with Drift

The process

Xₜ = αBₜ + βt

is a Lévy process with continuous trajectories and characteristic triplet (β, α², 0).

Properties:

• Drift component: βt (deterministic, linear)

• Diffusion component: αBₜ (scaled Brownian motion)

• Jump measure: ν = 0 (no jumps — purely continuous paths)

• Characteristic triplet: (β, α², 0)

Conversely, any Lévy process with continuous trajectories is necessarily a

Brownian motion with drift — making this the unique continuous Lévy process

up to scaling and shifting.

Example 2 :Poisson Process

Let (τᵢ)ᵢ≥₁ be a sequence of independent exponential random variables with

parameter λ > 0, and define the partial sums

Tₙ = τ₁ + τ₂ + ··· + τₙ

The Poisson process N = (Nₜ)ₜ≥₀ is then defined by

Nₜ = Σ 1{t ≥ Tₙ}

n≥1

For any t > 0, the random variable Nₜ follows a Poisson distribution:

ℙ(Nₜ = k) = e^(−λt) · (λt)ᵏ / k! k = 0, 1, 2, …

Properties:

• Intensity: λ > 0

• Characteristic triplet: (0, 0, ν) where ν = λδ₁

• Jump measure: ν = λδ₁ (Dirac mass at 1, scaled by λ)

• Jump sizes: always exactly 1

• Paths: piecewise constant, jumping by +1 at each Tₙ

• Mean: 𝔼[Nₜ] = λt

• Variance: Var(Nₜ) = λt

Example 3: Compound Poisson Process

Let N be a Poisson process with intensity λ > 0, and let (Yᵢ)ᵢ≥₁ be a sequence

of i.i.d. random variables with common law μ, independent of N. The compound

Poisson process is defined by

Nₜ

Xₜ = Σ Yᵢ , with the convention Xₜ = 0 when Nₜ = 0

i=1

Interpretation: jumps arrive at the random times T₁, T₂, … of the Poisson

process, and each jump carries a random size Yᵢ drawn from μ.

Properties:

• Jump arrival rate: λ > 0 (Poisson intensity)

• Jump size distribution: μ (law of each Yᵢ)

• Characteristic triplet: (β̃, 0, ν) where ν = λμ and

β̃ = λ ∫ x 1{|x|≤1} μ(dx)

• Jump measure: ν = λμ (intensity × jump law)

• Paths: piecewise constant with jumps of random size

• Mean: 𝔼[Xₜ] = λt · 𝔼[Y₁] (if 𝔼[Y₁] < ∞)

• Variance: Var(Xₜ) = λt · 𝔼[Y₁²] (if 𝔼[Y₁²] < ∞)

• Moment generating fn: 𝔼[e^(uXₜ)] = exp( λt ∫ (e^(ux) − 1) μ(dx) )

Note: The Poisson process in Example 9.1.3 is the special case where

μ = δ₁ (all jumps have size exactly 1), recovering Xₜ = Nₜ.Real world Applications related to Risk:

Lévy Jump Processes in Risk Management

1. VALUE AT RISK (VaR) AND EXPECTED SHORTFALL (ES)

Under a Gaussian model, the α-level VaR is:

VaR_α = μ + σ · Φ⁻¹(α)

This severely underestimates tail risk because it assigns near-zero probability

to large sudden losses. Under a Lévy model, the return distribution inherits

heavy tails directly from the jump measure ν(dx), so:

ℙ( Xₜ < −VaR_α ) is materially larger than the Gaussian predicts

The jump measure ν(dx) contributes excess mass in the tails:

Tail probability = diffusion tail + ∫ ν(dx)

|x|>threshold

In practice, VaR and ES are computed as follows:

Step 1: Fit a Lévy model (VG, NIG, or CGMY) to historical log-returns

Step 2: Simulate N paths of Xₜ over the risk horizon T using the

calibrated triplet (β, σ², ν)

Step 3: Compute VaR as the empirical α-quantile of simulated losses:

VaR_α = −Q_α( X_T )

Step 4: Compute Expected Shortfall (CVaR) — the average loss beyond VaR:

ES_α = −𝔼[ X_T | X_T < −VaR_α ]

Because ν can place significant mass on large negative moves, ES under a Lévy

model is substantially larger than its Gaussian counterpart — giving a more

honest and conservative picture of true tail exposure.

2. CREDIT RISK: DEFAULT AS A JUMP EVENT

In structural credit models, a firm defaults when its asset value Vₜ crosses

a fixed debt barrier D from above. Under pure Brownian motion:

Vₜ = V₀ · exp(σBₜ + βt)

the crossing is always gradual — the process cannot gap below D — which forces

short-term credit spreads to collapse to zero. This flatly contradicts

observed market credit spreads on short-dated instruments.

Under a Lévy-driven asset value model:

Vₜ = V₀ · exp(Xₜ) where Xₜ has triplet (β, σ², ν)

the firm can jump below the barrier instantaneously. The default time is:

τ = inf{ t ≥ 0 : Vₜ ≤ D }

and the default probability over horizon T is:

ℙ( τ ≤ T ) = ℙ( min Vₜ ≤ D )

0≤t≤T

The jump measure ν directly controls the likelihood of sudden default. A

heavier ν on the negative side raises ℙ(τ ≤ T) at short maturities, producing:

• Positive and realistic short-term credit spreads

• Sudden default without prior financial distress

• Richer CDS term structure matching market quotes

This makes Lévy models essential for pricing credit default swaps (CDS),

collateralized loan obligations (CLOs), and distressed corporate bonds.

3. OPERATIONAL RISK AND RUIN THEORY

The aggregate loss process in insurance or operational risk is modeled

naturally as a compound Poisson process — a canonical Lévy process:

Nₜ

Lₜ = Σ Yᵢ

i=1

where:

Nₜ = number of loss events up to time t, Poisson with intensity λ

Yᵢ = size of the i-th loss, i.i.d. with law μ

ν = λμ (the Lévy measure of Lₜ)

The firm's surplus (capital reserve) process is:

Rₜ = u + ct − Lₜ

u = initial capital reserve

c = premium or revenue income rate

Lₜ = cumulative losses (compound Poisson)

Ruin occurs the moment the surplus turns negative. The ruin probability is:

ψ(u) = ℙ( Rₜ < 0 for some t ≥ 0 )

The Cramér-Lundberg theorem gives an exponential upper bound:

ψ(u) ≤ e^(−Ru)

where R > 0 is the adjustment coefficient — the positive root of the

Lundberg equation:

λ + cR = λ · 𝔼[ e^(RY) ]

Key risk management insight: the heavier the tail of μ (the jump size

distribution), the smaller R becomes, and the slower ψ(u) decays — meaning

the firm needs substantially more capital u to maintain ruin probability

below a regulatory threshold. This directly informs:

• Basel III operational risk capital charges

• Solvency II reserve requirements for insurers

• Internal capital adequacy assessments (ICAAP)Conclusion:

Lévy processes offer a more honest mathematical language for risk. By allowing jumps, they capture what Gaussian models routinely miss , sudden defaults, fat-tailed losses, and catastrophic operational events that arrive without warning. Across VaR and Expected Shortfall, credit risk, and ruin theory, the jump measure ν does the heavy lifting: it directly parameterizes how bad things can get and how fast they can get there. For any serious risk management framework, ignoring jumps is not a simplification it is a miscalculation.

!!!Happy Reading