From 9 Days to 2: The GenAI Blueprint That Will Reshape Indian Lending

Irfan Shirur12 min read·Just now

Irfan Shirur12 min read·Just now--

Irfan Shirur | AI-Native Solution Architect | Building Agentic AI Solutions and platforms

A production-grade GenAI blueprint for the lending platform that should already exist.

Indian loan processing is broken in ways everyone tolerates: 9-day TAT, 60% First-Time-Right, ₹4,500 cost-per-file, and a fraud window that stays open until after disbursement.

The technology to fix this — agentic LLMs, multi-modal document AI, vector and graph databases — is mature, deployable, and affordable.

The banks that build a real platform in the next 18 months will define the next decade of Indian lending. The rest will buy a watered-down version in 2027 and wonder why their cost-per-file didn’t move.

A Story Most Bankers Will Recognize

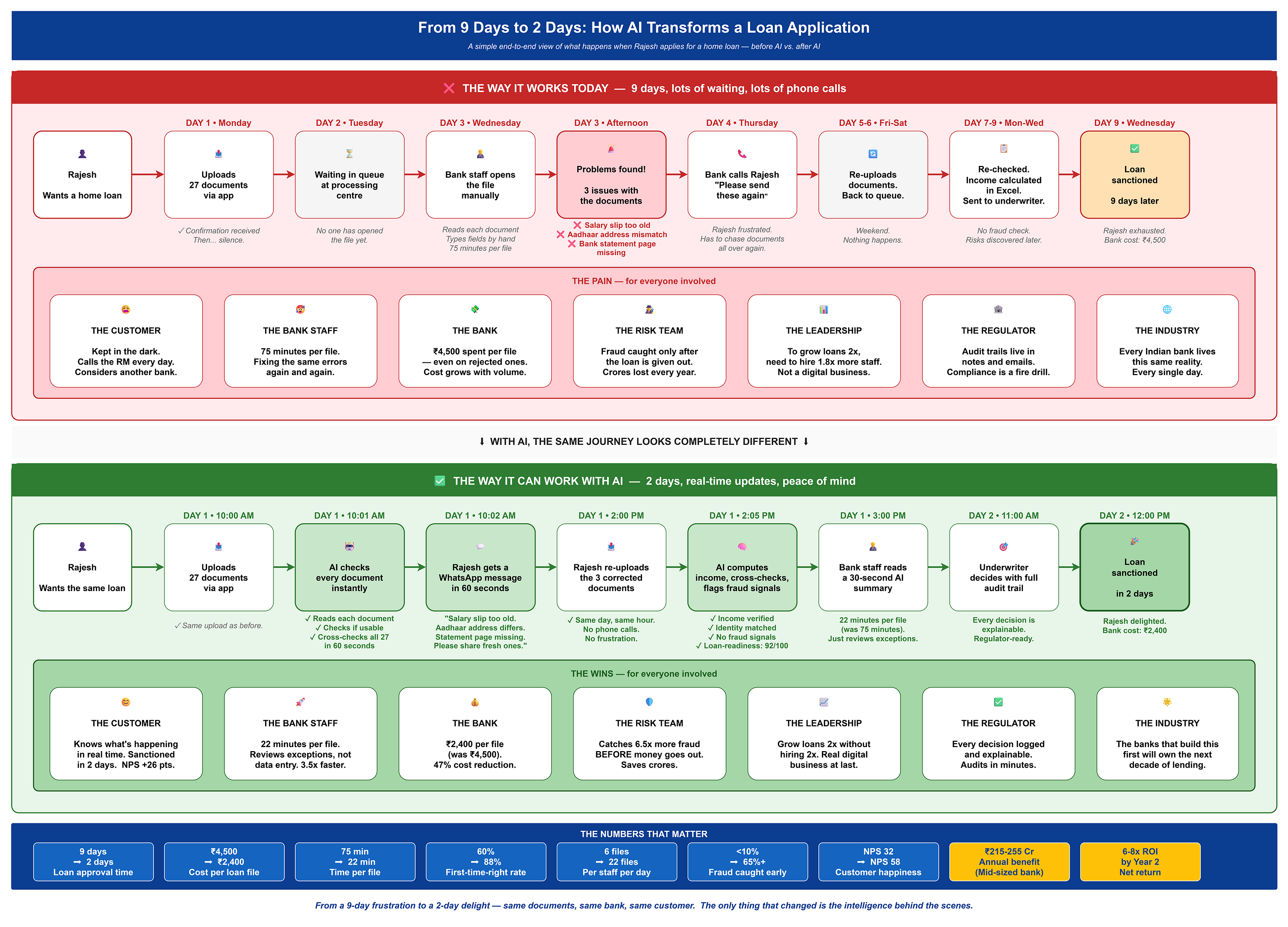

Rajesh applies for a home loan on a Monday morning. He uploads 27 documents through a slick mobile app. He gets a confirmation message. Then silence.

On Wednesday, a Central Processing Agent in Mumbai opens his file, types fields into the LOS by hand, and discovers his salary slip is from December (it’s now April), his Aadhaar address doesn’t match his utility bill, and page 4 of his bank statement is missing.

The bank calls him on Thursday. He sends the documents Friday. The CPA re-opens the file the following Tuesday. He gets sanctioned 11 days after he applied — *if* nothing else surfaces.

This is not an edge case. This is the median experience of a home loan in India in 2026.

The fix is not a better OCR tool. The fix is a fundamentally different kind of platform.

The 10 Failure Modes of Indian Loan Processing

Before the solution, the honest diagnosis. Every Indian bank lives some combination of these:

1. Document chaos at the front door. 25–40 documents per home loan, uploaded as blurry phone photos, screenshots of WhatsApp forwards, scanned PDFs from cybercafés, HEIC files from iPhones. No upfront intelligence. The file just lands in a queue.

2. The CPA bottleneck. 45–90 minutes per file, manually. Quality varies by experience, training cycle, and frankly, the day of the week.

3. The “3rd day surprise.” Customer submits Day 1. CPA opens Day 3. Discovers problems. TAT explodes.

4. No cross-document intelligence. “Rajesh Kumar Sharma” / “Rajesh K Sharma” / “R. K. Sharma” / “Rajesh Kumar” across PAN, Aadhaar, salary slip, bank statement. Today, a human reconciles this in their head.

5. Income computation is a spreadsheet sport. Excel-driven. Inconsistent. Audit-unfriendly.

6. Fraud walks in through the front door. Photoshopped salary slips. Tampered bank statements. Recycled rent agreements. Most fraud is caught *after* disbursement.

7. Late-stage rejection wastes ₹3K–₹8K per file in CPA, RM, bureau, and valuation costs.

8. Customer experience is stuck in 2010. No real-time feedback. Just silence, then a phone call.

9. Audit trails live in CPA notes and tribal knowledge. RBI audits become fire drills.

10. The scale ceiling. 2x the loan book requires 1.8x the headcount. That’s not a digital business model — it’s an operations business in a digital costume.

7 Principles I’d Pin to Every Engineer’s Wall

If your team is building anything in this space, start here. Skip these and you’ll ship a demo, not a platform.

1. Don’t start with the LLM. Start with the workflow engine. The control plane is what makes this production-grade. The AI is the easy part.

2. Tokenize PII at ingest, not later. Retrofitting privacy is expensive and risky.

3. Every agent must have a confidence score and a fallback. No silent failures.

4. Log everything. Replay everything. Auditability is a build-time decision, not a runtime feature.

5. Configuration > code. The moment you hardcode a document type or a validation rule, you’ve killed multi-tenancy.

6. Treat documents as untrusted input. Prompt injection from a PDF is real.

7. Ship Phase 1 in 10 weeks or you’ve lost the room. Banks fund what they see working.

These principles are the difference between a system that survives 50,000 files a day and one that dies at the pilot.

The Solution: Three Non-Negotiables

🟢 Agentic, not monolithic. Specialized AI agents for specialized jobs, orchestrated by a control plane. A single “do-everything” LLM call is a prototype. Production decomposes the workflow.

🟢 Configurable, not hardcoded. Every document type, validation rule, and threshold is metadata-driven. New bank or new loan product = configuration, not code.

🟢 Human-in-the-loop by design. AI proposes, humans dispose. Every agent has a confidence score. Every score has a threshold. Every threshold has an escalation path.

Reference Architecture (At a Glance)

The platform is built as seven layers, each with one clear responsibility:

Channel Layer — One normalized intake API across mobile app, web, RM app, branch UI, WhatsApp. One contract, many fronts.

Ingestion & Pre-Processing — Format normalization, deskew, denoise, contrast enhancement, auto-rotate, page splitting, encryption. PII tokenization happens here, not later.

Orchestration & Control Plane — Workflow engine (Temporal or equivalent) drives per-file lifecycles. Each loan product has its own DAG. Retry, timeout, fallback, SLA tracking. This is the spine.

AI Agent Layer — 9 specialized agents, covered next.

Knowledge & Data Layer — Vector DB (fraud pattern similarity), Graph DB (entity relationships), Postgres (system of record), Object Store (raw + processed docs), Feature Store (ML feature consistency).

Integration Layer — REST + Kafka. Wraps LOS, CRM, bureau, DigiLocker, Account Aggregator, GSTN, Core Banking. Circuit breakers everywhere.

Governance & Observability (cross-cutting) — Model versioning, drift monitoring, explainability payloads, PII access logs. This is what passes the RBI audit.

— -

The 9 AI Agents — and Why Each Exists

This is where most “AI for banking” pitches stay vague. I’m going deep on the four hardest ones and brief on the rest.

Agent 1 — Classification | “What document is this?”

Multi-modal model (LayoutLMv3 or Donut) + lightweight LLM validator for ambiguous cases. Handles rotated, partial, multilingual documents. Output: {doc_type, confidence, alternative_candidates}.

Output: {doc_type, confidence, alternative_candidates}.Agent 2 — Extraction | “What does it say?” (deep dive)

Pure LLM extraction hallucinates. Pure OCR misses context. Pure regex breaks on format variation. The robust pattern is a 4-stage pipeline:

1. OCR — Tesseract for printed text, TrOCR/PaddleOCR for handwritten and Indic scripts. Outputs raw text + bounding boxes.

2. Layout Model — Understands spatial structure (where the “Net Salary” label sits relative to its value).

3. LLM with Structured Output — Function calling / JSON schema enforcement. Reasons over messy formats and emits a typed object.

4. Validation Pass — Regex + checksums (PAN format, Aadhaar Verhoeff check, IFSC structure).

Every extracted field carries a confidence score and a source bounding box. That bounding box is your audit trail when the regulator asks.

Agent 3 — Quality & Completeness | “Is it usable?”

Image quality models (BRISQUE, NIQE) + business rules (salary slip < 90 days, statement covers 6 continuous months) + page continuity checks. This single agent is what kills the “3rd day surprise.” It catches issues on minute 1.

Agent 4 — Cross-Validation | “Do all documents agree?”

Fuzzy name matching (Levenshtein + Soundex + Metaphone, tuned for Indian names), date normalization, semantic address matching via LLM, and entity resolution through the Graph DB.

Agent 5 — Fraud & Tampering | “Is this real?” (deep dive)

Defense in depth, not a single model:

1. Image forensics — Error Level Analysis (ELA), copy-move detection, font consistency, JPEG artifact analysis.

2. Metadata analysis — PDF creation tool, edit history, font embedding patterns. A “salary slip” created in Photoshop is suspicious.

3. Template similarity — Embed the document, search the vector DB for known fraud templates.

4. Cross-applicant patterns — Same rent agreement across 4 unrelated applicants? Graph DB query in milliseconds.

5. Statistical anomalies — Benford’s Law on financial documents, transaction-pattern entropy on bank statements.

This agent never auto-rejects. It flags. Humans decide. That distinction is what keeps the platform compliant.

Agent 6 — Income Computation | “What’s the real, sustainable income?” (deep dive)

For salaried applicants:

1. Extract net salary from each of 3 slips

2. Identify salary credits in bank statement (regex + amount range + employer name match)

3. Reconcile slip vs. credit (variance < 5% expected)

4. Smooth for one-offs (bonuses, arrears flagged separately)

5. Cross-check Form 16 annual ÷ 12

For self-employed applicants:

1. Parse 2 years of ITR

2. Extract gross receipts, net profit, depreciation add-backs

3. Reconcile with P&L and balance sheet

4. Cross-validate with GST returns

5. Compute normalized monthly income with year-on-year trend

Output: computed income + a worksheet where every number traces back to a source field. The worksheet is the audit trail.

Agent 7 — Summarization | “Tell the loan officer the story in 30 seconds.”

Grounded LLM call. Receives structured outputs from Agents 1–6 (not raw documents). Generates a summary where every claim cites the source field. No hallucination because nothing is generated from raw text.

Agent 8 — Risk & Readiness Scoring | “How loan-ready is this file?”

Weighted score (0–100): KYC completeness 20%, income verification 25%, freshness 10%, cross-validation 20%, fraud signal absence 25%. Routes files: 85+ fast-track, 65–84 standard CPA, 40–64 senior underwriter, <40 customer remediation.

Agent 9 — Customer Communication | “Close the loop in real time.” (deep dive)

Templated + LLM-personalized messages, vernacular-aware (Hindi, Tamil, Telugu, Kannada, Marathi, Bengali), delivered via WhatsApp Business API / SMS / app push.

Examples:

”Your March salary slip is unclear. Please re-upload.”

Page 4 of your bank statement is missing.”

”Your Aadhaar address (Bengaluru) differs from your utility bill (Mumbai). Please share the latest address proof.”

This is the agent customers feel. It is the single biggest NPS lever in the entire platform.

— — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — —

Tech Stack (Production-Grade Choices)

On-prem reality: Indian PSU banks will demand on-prem or sovereign cloud. Architecture must run on either. Llama 3 / Mistral via vLLM or TGI cover the on-prem case credibly.

— — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — -

Security, Compliance & What Keeps the CISO Awake

- Data residency — All data in India. RBI localization is non-negotiable.

- PII handling — Tokenize PAN, Aadhaar, account numbers at ingest. Detokenization is logged, role-gated, time-bound.

- DPDP Act readiness — Consent capture, purpose limitation, right-to-erasure built into the data layer.

- Model governance— Every model versioned, drift-monitored, with champion-challenger evals and rollback paths.

- Auditability— Every decision is reproducible. Same model versions on same inputs = same output.

- Adversarial robustness — Documents are *untrusted input*. Prompt injection from a PDF is real. Schema enforcement and prompt isolation are mandatory.

— — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — —

Build Roadmap

Phase 1 (Weeks 1–10) — Foundation + KYC. Ingestion, orchestration, observability. Agents 1, 2, 3, 4, 9. One LOS integration, one notification channel. Live ROI on KYC docs in Quarter 1.

Phase 2 (Weeks 11–22) — Income & Employment. Agents 5, 6, 7. Bank statements, salary slips, Form 16, GST. Account Aggregator integration. Full salaried home loan / personal loan automation.

Phase 3 (Weeks 23–36) — Complex & Self-Employed. Agent 8 at full fidelity. ITR, balance sheet, P&L, property and corporate documents. Coverage for 90%+ of loan products.

Phase 4 (Months 9–12) — Productize. Multi-tenancy hardening, configuration UI for new banks/products, white-labelling. Same platform sells to Bank A and Bank B with config, not code.

— — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — —

The ROI: What This Actually Does to a Bank’s P&L

This is the section most architects rush through and most CFOs stop on. Let me give it the space it deserves.

A Concrete Example — “Bank X” (Mid-Sized Indian Bank)

Baseline today:

- 50,000 home loan files / month

- 200 CPAs at ₹6L fully loaded annual cost

- ₹4,500 cost per file

- 9-day TAT, 60% FTR

- Annual processing cost: ~₹270 Cr

Steady state at Year 2:

The Annual Financial Impact

💰 Operational savings: ~₹105 Cr/year

💰 Fraud loss prevention: ~₹40–60 Cr/year

💰 Revenue uplift from faster TAT (lower drop-off): ~₹70–90 Cr/year

💰 Total annual benefit: ₹215–255 Cr

💸 Platform investment (build + run): ~₹25–35 Cr/year

✅ Net ROI: 6–8x by Year 2

Why Each C-Suite Persona Should Care

This is the part the architects forget and the CXOs need.

For the CFO— Cost-per-file becomes a governable metric, not an HR-driven one. Operational leverage finally arrives in lending. For the first time, the bank can grow loan volume without growing cost linearly.

For the COO— Scale 2x without hiring 2x. CPAs move from data entry to exception handling — higher value, lower attrition, better career path.

For the CRO (Risk) — Fraud window shrinks from 7 days to 7 minutes. Cross-document intelligence catches identity mismatches no human ever would. The risk function gets a sensor it never had.

For the CIO/CTO — One platform, many products (home, personal, MSME, auto, education). Configurable, multi-tenant, RBI-audit-ready out of the box. One build, multiple P&L lines.

For the CMO — NPS jumps because customers stop being kept in the dark. Real-time nudges turn a black-box process into a transparent one. Lending becomes a brand asset, not a brand liability.

For the Customer — From ”I uploaded my docs, now I wait” to ”I uploaded my docs, I know exactly what’s needed, and I’m sanctioned in 48 hours.”

Beyond the File-Level ROI: Five Platforms in One

Once the document intelligence layer exists, the same engine powers:

1. Pre-screening at lead stage— kill bad leads before bureau cost is spent

2. MSME and corporate lending — same agents, different document mix

3. Post-disbursement audit and continuous monitoring— compliance becomes a stream, not a project

4. Cross-sell readiness — instant pre-approval for existing customers

5. DIY customer journeys— true self-service with AI feedback in real time

One platform. Five revenue streams. Compounding ROI.

That is the difference between automating a process and building strategic capacity. The first reduces cost. The second changes what the bank is capable of.

— — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — —

The Uncomfortable Truth

Most Indian banks won’t build this.

They’ll buy a watered-down version from a vendor in 2027, plug it into one product line, and wonder why their cost-per-file barely moved. They’ll blame “AI hype.” The reality will be that they bought a tool when they needed a platform.

The 2–3 banks that build this now, properly, end-to-end, will own the next decade of Indian lending. They’ll undercut on price, win on TAT, and lock in customers who never go back to the 9-day experience.

The technology is ready. The cost curve is ready. The talent is ready.

The only question is which CEO calls the meeting.

— — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — —

The One-Line Pitch

An agentic, multi-modal, configuration-driven AI Document Intelligence Platform that compresses loan processing from days to minutes — and turns lending operations from a cost center into a competitive moat for Indian banks.

— — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — —

If you’re a CTO, Head of Lending, Chief Risk Officer, or architect thinking about this — I’d love to compare notes. The window is 18 months. After that, the moat belongs to whoever moved first.

What’s your bank waiting for?

— — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — —

If you found this useful, a clap and a follow help more than you’d think. I write about GenAI architecture, BFSI transformation, and what it actually takes to ship production AI systems.

#GenAI, #Banking Technology, #Indian Banking, #Document Intelligence, #Lending Transformation, #Agentic AI, #BFSI, #Digital Lending, #Solution Architecture

Above the ROI table:

Note: The numbers below are illustrative, based on industry benchmarks and professional experience — not from any specific bank’s audited data.

The views and architecture in this article are my own, not those of any

employer, client, or partner organization. The ROI numbers are illustrative,

based on publicly available industry benchmarks and my professional

experience — not from any specific bank’s audited data. Use them as a

directional reference, not a quote.