Federal Reserve reports slight rise in US bank loan delinquencies in 2025

Overall delinquency rates remain below the decade average, but commercial real estate and mortgage loans are flashing warning signs.

Share

Add us on Google by Editorial Team Jun. 3, 2026The Federal Reserve’s latest Supervision and Regulation Report paints a picture of US bank loan health that looks fine from a distance but gets more concerning the closer you zoom in. Total bank loan delinquency rates sat at approximately 1.5% during the first half of 2025, technically below the 10-year average of 1.7%.

Commercial real estate loans have been the standout troublemaker. CRE delinquency rates remain above their decade averages, with office properties in particular hovering near a 10% delinquency rate as of Q2 2025.

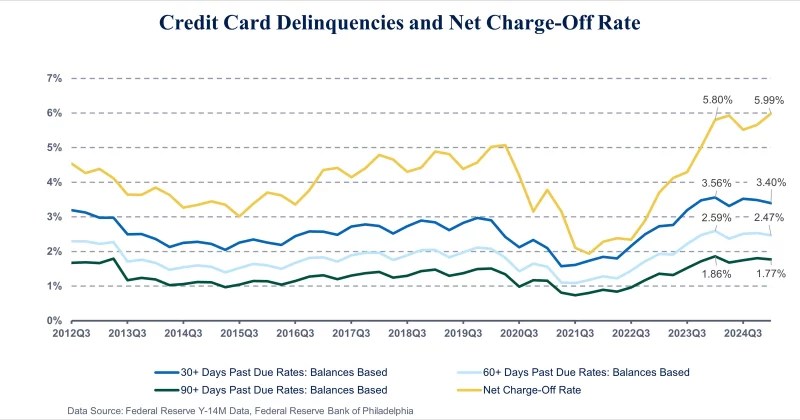

On the consumer side, the Fed’s December 2025 report noted that most major loan categories actually saw decreases in delinquency rates. Credit card and auto loan delinquencies held relatively stable.

AdvertisementThe aggregate household debt delinquency rate climbed to 4.8% of outstanding debt by Q4 2025, according to New York Fed data. That represents a 0.3 percentage point increase from Q3 2025. The rise was largely driven by serious delinquencies in mortgages and student loans.

Mortgage delinquency rates specifically rose to 4.26% in Q4 2025, an increase of 27 basis points quarter-over-quarter. Consumer loan delinquency rates, measured separately, showed 2.62% in Q4 2025 and 2.64% in Q1 2026, per FRED data.

After years of pandemic-era forbearance and payment pauses, student loan borrowers have been cycling back into active repayment, and that’s showing up in the delinquency data.

The banking system’s capital position remains solid by regulatory standards. Banks have generally maintained healthy reserves, which means the rising delinquencies aren’t threatening systemic stability.

The key variable to watch is whether the Q4 2025 uptick in household delinquencies stabilizes or accelerates through the first half of 2026. An acceleration, particularly if it spreads beyond mortgages and student loans into credit cards and auto loans, would signal something more systemic.

Disclosure: This article was edited by Editorial Team. For more information on how we create and review content, see our Editorial Policy.