FDIC reports US banking asset quality remains favorable despite margin pressure

The agency's Q4 2025 data shows past-due loans well below pre-pandemic levels, but cracks in commercial real estate and consumer credit deserve a closer look.

Share

Add us on Google by Editorial Team May. 27, 2026The US banking system closed out 2025 in solid shape, at least by the numbers. The FDIC’s latest Quarterly Banking Profile shows asset quality holding steady, profits climbing, and deposits growing for the sixth straight quarter.

The numbers behind the optimism

FDIC-insured institutions posted net income of $77.7 billion in Q4 2025, good for a return on assets of 1.24%. For the full year, the industry brought in $295.6 billion in net income, a 10.2% jump from 2024.

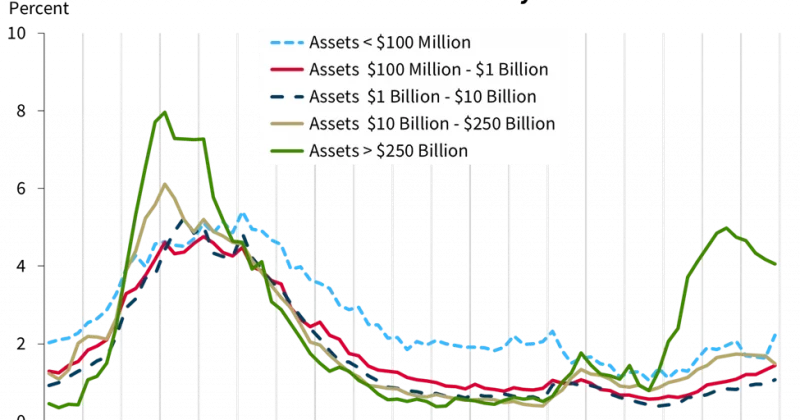

The past-due and nonaccrual rate, which tracks loans that are either late or no longer accruing interest, came in at 1.56%. For context, the pre-pandemic average was 1.94%. So the industry is sitting comfortably below the baseline that regulators typically consider “normal.”

AdvertisementDomestic deposits grew 1.8% during the quarter, extending a streak of six consecutive quarters of increases.

Unrealized losses on securities fell to $306.1 billion, the lowest level since Q1 2022.

Where the cracks are forming

Elevated delinquency rates showed up in non-owner-occupied commercial real estate, multifamily CRE, auto loans, and credit cards.

The net charge-off rate ticked up to 0.63%.

What this means for investors

The CRE delinquency story has been building for long enough that it’s no longer a forward-looking risk. It’s a present-tense reality that banks are actively managing.

Investors should keep a particularly close eye on CRE-heavy regional banks in upcoming earnings reports. The aggregate data looks fine. The question is whether that average is masking a bimodal distribution where some institutions are thriving while others are quietly absorbing losses that haven’t fully materialized yet.

Disclosure: This article was edited by Editorial Team. For more information on how we create and review content, see our Editorial Policy.