DeFi Yield Looks Simple but Where Does It Come From?

--

DeFi Yield Looks Simple, but Where Does It Come From?

You open a DeFi dashboard, see a big APY, and click a simple deposit button, it all feels easy to compare and easy to trust. But a clean number isn’t the same as a clear business model, and that’s where many users get caught.

Because yield in DeFi often looks simpler than it is, the real source of return can stay hidden behind incentives, dilution, fees, or risk. If you can’t explain where that return comes from, there’s a real chance your capital is helping fund someone else’s gain, so let’s start with the illusion first.

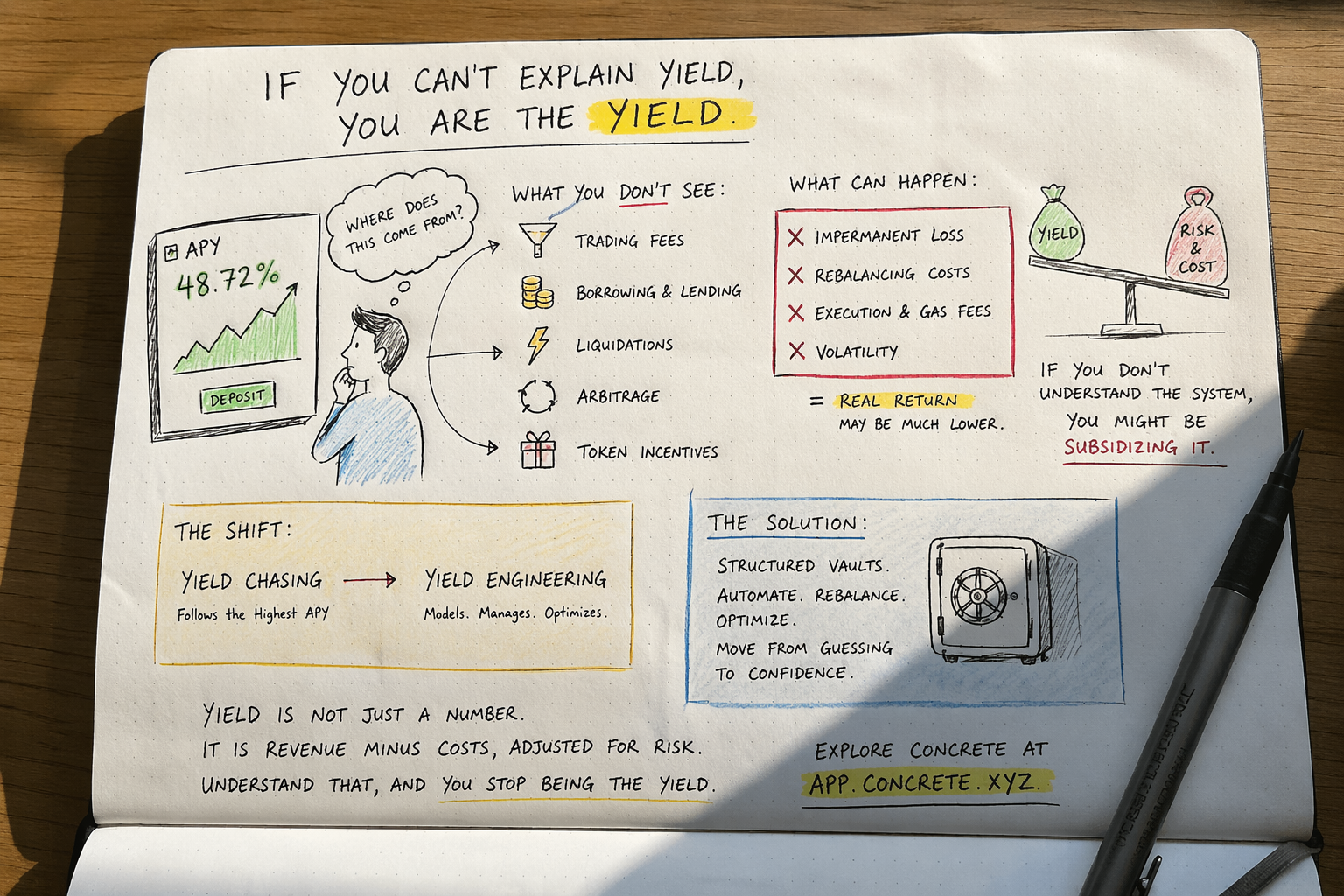

The dashboard shows the result, not the engine

A DeFi app usually shows you the output first. You see the APY, the chart, and the deposit button. What you often don’t see is the machinery underneath, the trades, loans, emissions, liquidations, and protocol links that make that number possible.

That matters because a dashboard is a display layer, not an explanation. It can make a messy system feel neat, stable, and easy to compare, even when the yield source changes by the hour.

Why high APYs feel more certain than they really are

A big APY looks precise because it’s wrapped in clean design. Real-time charts tick upward, calculators project compounding growth, and the number updates like a live score. As a result, your brain reads it as something measured and dependable, not something built on moving parts.

But APY is often just a snapshot. It may reflect today’s trading volume, today’s borrowing demand, today’s token rewards, or today’s market price. If any of those shift, the headline yield can drop fast.

Compounding tools add to the illusion. They show smooth future returns, but they rely on a quiet assumption: that the current rate stays in place. In DeFi, that assumption often breaks. A pool showing 40% today can show 12% next week if rewards slow, new deposits flood in, or token prices fall.

A precise number can still describe an unstable situation.

In other words, APY tells you what the dashboard is showing right now. It does not tell you what you’ll actually earn over time, and it doesn’t explain where that return comes from in the first place.

How simple deposit flows hide complex risks

The deposit flow feels almost too easy. Connect wallet, click deposit, approve, done. That smooth path can make the product feel low-risk, even when your funds are moving through several layers of risk at once.

For example, a simple vault might deposit your token into a lending market, borrow against it, loop that position for extra yield, and then pay you partly with reward tokens. On the front end, it looks like one balance and one APY. Under the hood, it may depend on borrow demand, collateral health, token incentives, and another protocol’s smart contracts.

A single click can hide risks like these:

- Lending risk, if borrowers fail or the market gets stressed.

- Liquidation risk, if leverage sits behind the strategy and prices move hard.

- Smart contract risk, if a bug or exploit hits any contract in the stack.

- Liquidity risk, if exits become costly or slow when many users leave at once.

- Token emission risk, if yield depends on reward tokens that lose value.

- Protocol dependency risk, if one app relies on another app to keep working.

Think of it like a car dashboard showing your speed. Useful, yes. But it doesn’t tell you if the engine is overheating. In DeFi, the clean interface often hides the parts that matter most.

Before you chase yield, ask where the money comes from

A simple rule can keep you out of bad setups: trace the cash flow. Before you look at the rate, look at the source. If you can name who is paying, why they are paying, and what happens if that demand fades, you already understand more than most depositors.

Think of DeFi yield like rent from a property. The number matters, but the tenant matters more. A return backed by real use is different from a return backed by token printing or a looped strategy that keeps feeding on itself.

Productive yield comes from real economic activity

The cleanest kind of yield comes from someone paying for something useful. In DeFi, that usually means a borrower pays interest to access capital, a trader pays fees to swap assets, or a user pays for a service that saves time, reduces risk, or improves execution.

For example, lending markets can generate yield when traders, funds, or other users borrow assets and pay interest. A DEX pool can generate yield when traders pay swap fees. Market makers may earn spreads because they stand ready to buy and sell, which helps the market function. In each case, the return has a visible source tied to actual demand.

That doesn’t make it risk-free. Borrow demand can dry up, trading volume can fall, and spreads can shrink when competition rises. Still, this type of yield has a stronger base because you can point to the engine. Money comes in because a user wants a real service, not just because a protocol wants deposits.

A quick gut check helps here:

- Can you explain who pays the yield?

- Can you explain why they pay it?

- Can you picture what service they get in return?

If those answers are clear, you’re looking at a more grounded form of yield.

The best yield stories start with customer demand, not just a high number on a screen.

Incentive yield often comes from token emissions and dilution

Now for the part that trips people up. Some protocols boost returns by issuing new tokens and handing them to depositors. On the dashboard, that reward can make the APY look strong. In practice, the protocol may be paying you with assets it created itself.

That can work for a while, especially when the token price holds up. Early users may earn well if demand for the token stays strong. However, the displayed yield can blur the difference between income and subsidy. If new tokens keep hitting the market, someone has to absorb that supply.

Here is the plain version: if a protocol prints tokens to reward depositors, the return may come from dilution. Existing holders carry part of that cost. Future buyers may carry the rest if they buy the token after rewards push supply higher. So the yield isn’t always coming from outside demand. Sometimes it’s coming from the system itself.

That doesn’t mean all token incentives are useless. They can help a protocol attract early liquidity or bootstrap activity. But they shouldn’t be confused with durable cash flow. If the rewards stop and the yield disappears, the source was never very strong to begin with.

A good way to frame it is simple. Ask whether the yield would still exist if the token reward went to zero. If the answer is no, you are mostly looking at an incentive program, not a self-supporting business model.

Recycled yield can come from leverage, looping, or accounting tricks

Some of the biggest yields come from money moving in circles. A strategy deposits an asset, borrows against it, redeposits the borrowed funds, and repeats the process. That can increase the reported return because each layer may collect more interest, more rewards, or both. But the system hasn’t created new value. It has mostly created more exposure.

This is where financial engineering can look like income. The numbers rise because the same base capital gets counted more than once. A vault may stack lending yield, token rewards, and auto-compounding on top of a looped position. On paper, the APY looks rich. Underneath, the structure may depend on stable prices, cheap borrowing, and liquid exits.

Here is the key difference:

Type of returnMain sourceWhat can go wrongProductive yieldBorrowers, traders, service usersDemand falls, fees shrink, defaults riseIncentive yieldNew token issuanceToken price drops, dilution grows, rewards endRecycled yieldBorrowing loops and stacked rewardsLiquidations, funding costs rise, unwind risk

So when you see a high number, ask whether cash is entering from outside users or just spinning inside the machine. If it is mostly the second, the yield may be more fragile than it looks. That doesn’t mean no one can profit. It means the return depends more on timing and market conditions than on steady cash flow.

Explore Concrete at app.concrete.xyz