Decentralized Payment Routing: How the Paycrest Protocol Architecture Works

Paycrest6 min read·Just now

Paycrest6 min read·Just now--

Cross-border payments have long been one of the most frustrating experiences in global finance. Sending money from China to Nigeria, for example, still costs significant fees and can take T+n days. For the billions of dollars in annual remittances flowing into Africa and other emerging markets, that translates to real money lost to middlemen every single year.

Stablecoins changed the conversation. They have seconds finality, cost fractions of a cent on modern blockchains, and are seeing massive organic adoption globally. But there has always been a stubborn gap: converting stablecoins into local currency at the last mile. This is precisely the problem Paycrest is built to solve.

What Is Paycrest?

Paycrest is a decentralized payment routing protocol that connects applications and their users to a global network of fiat and stablecoin liquidity providers, enabling seamless conversion between stablecoins and local currencies without ever holding users’ funds.

Think of it like Uber, but for money. When you open Uber, you do not call a specific driver. You request a ride, and Uber’s platform routes your request to the most suitable driver based on location, availability, and price. The driver and passenger transact directly, while Uber acts only as the coordination layer.

Paycrest works the same way. When a user wants to convert USDC to Nigerian naira or Kenyan shillings, Paycrest does not process the transaction itself. Instead, it routes the payment order to the most suitable liquidity provider, a business set up to fulfill it, settle the fiat order, and Paycrest ensures both parties are protected without touching the funds using escrow smart contracts.

The result: stablecoin-to-fiat (off-ramp) and fiat-to-stablecoin (on-ramp) transactions that complete in under 30 seconds, with no custodial risk.

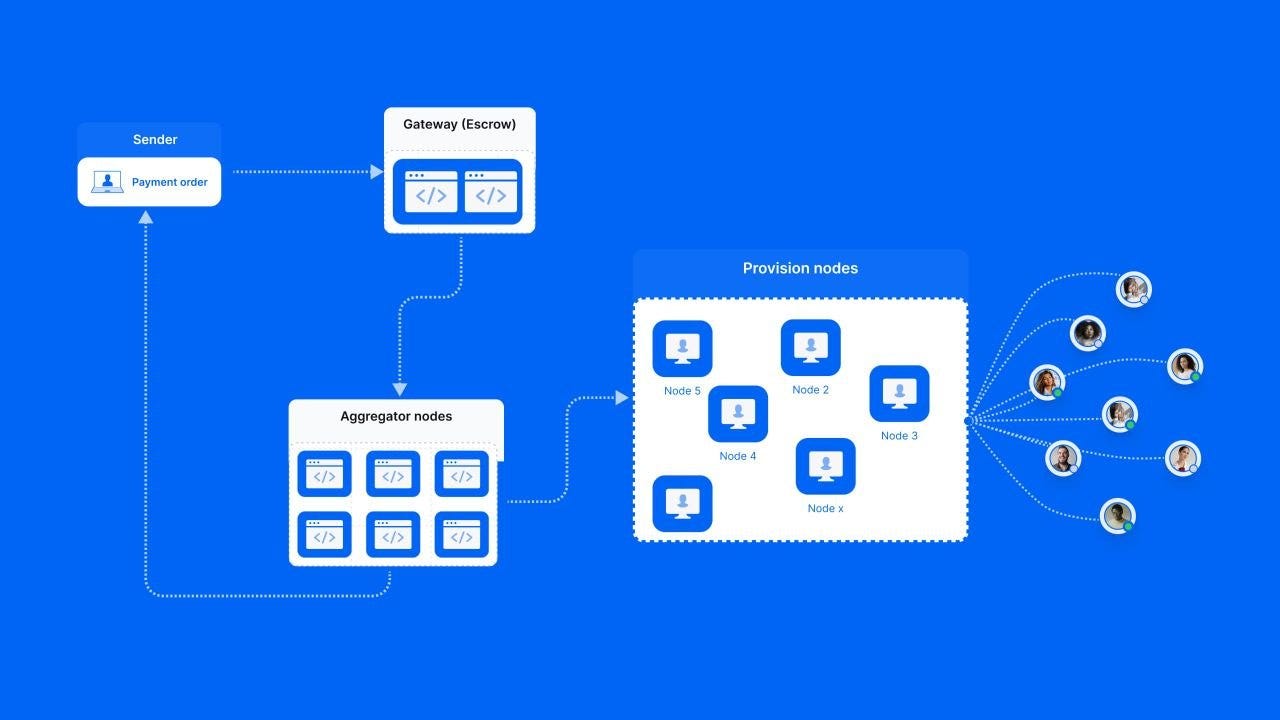

Paycrest Network Participants

Every transaction on the Paycrest network involves four roles. Understanding who does what is the foundation of building on the protocol.

Senders

Senders are the applications that integrate with Paycrest. These include wallets, fintech apps, DeFi protocols, or any business that needs to offer stablecoin on and off-ramps to users. Senders do not fulfill payments themselves. Instead, they create payment orders through the Paycrest API. Every sender must complete KYB (Know Your Business) verification before accessing the network.

Recipients

Recipients are the end users who receive funds (fiat or stablecoins). This could be a person in Lagos receiving naira in their bank account, a freelancer in Kenya receiving shillings in their M-Pesa wallet or a contract worker in Rwanda receiving USDC. Recipients do not interact with the protocol directly. They simply receive their funds.

Providers

Providers are the businesses that fulfill payment orders. They supply fiat liquidity in exchange for stablecoins for off-ramps, or supply stablecoins in exchange for fiat for on-ramps. They operate their own payment infrastructure, set their own rates, and connect to local Payment Service Providers or wallet services. Like drivers on Uber, providers compete on rates and availability to win orders.

Aggregators

Aggregators are the routing layers of the network. It monitors for new payment orders and matches them with the most suitable provider based on rate, availability, and the currency corridor. It is currently operated by Paycrest but is designed to become a fully decentralized, distributed and permissionless component over time.

The Architecture: Three Layers Working Together

Paycrest’s architecture is built on three core components that work together to make every payment secure, fast, and trustless.

The Gateway Contract: The Escrow Engine

The Gateway Contract are smart contracts deployed on-chain. It is the foundation of the protocol’s trustless model and ensures that neither senders nor providers need to trust each other.

When a sender creates a payment order, the stablecoins are locked inside the Gateway Contract. They are not sent to Paycrest and not sent to the provider. Instead, they remain in escrow on the blockchain until the settlement is confirmed. Only after the provider delivers fiat to the recipient’s bank account or mobile wallet are the escrowed stablecoins released to the provider.

This is how the non-custodial model works in practice. Paycrest never holds user funds. The smart contract holds the funds and executes automatically based on predefined rules rather than trust.

Aggregator Nodes: The Routing Intelligence

Aggregator nodes continuously monitor the Gateway Contract for new payment orders. As soon as a new order appears on-chain, the aggregator evaluates available providers based on factors such as offered rates, amount, supported currencies, psp reliability and fulfillment history. It then assigns the order to the most suitable provider.

This functions like the dispatch system in the Uber analogy. It does not select just any provider. It selects the most appropriate provider for the transaction.

Provision Nodes: The Fulfillment Layer

Provision nodes are operated by providers. Each node connects to local payment service providers such as banks, mobile money platforms, payment processors and stablecoin wallets. These nodes are responsible for executing the actual fiat and stablecoin payment to the recipient.

Once the payment is confirmed, the provision node reports back to the protocol. This triggers the on-chain settlement process, which releases the escrowed stablecoins to the provider. For on-ramp once the fiat is sent to the provider’s bank, the provider’s node signs a transaction and stablecoin is settled to the sender address.

How a Transaction Works: Step by Step

Let’s trace a complete off-ramp transaction where a user converts 100 USDT to Nigerian naira.

Step 1: Order Initiated

The sender application calls the Paycrest API to create a payment order, specifying the amount, token (USDT), recipient bank details, and currency (NGN). The API returns a deposit address, and the order is marked as “initiated”.

Step 2: Deposited

The user sends 100 USDT to the deposit address. The protocol detects the on-chain deposit, and the order status updates to “deposited”.

Step 3: Pending

The aggregator scans available providers and assigns the order to the most suitable option. The status becomes “pending”.

Step 4: Fulfilling

The assigned provider’s provision node begins disbursing naira to the recipient’s bank account through a local payment service provider. The status becomes “fulfilling”.

Step 5: Validated

The provider’s bank or payment service provider confirms successful fiat delivery. The status updates to “validated”.

Step 6: Settling

The Gateway Contract releases the escrowed USDT to the provider on-chain. The status becomes “settling”.

Step 7: Settled

The transaction is complete. The recipient has received naira, and the provider has received USDT. The entire process takes less than 30 seconds.

If the provider cannot fulfill an order for any reason, the contract automatically refunds the stablecoins to the sender for off-ramp transactions, or the PSP returns the fiat to the sender’s bank account for on-ramp transactions.

What Makes Paycrest Different

Several features set Paycrest apart from traditional payment integrations.

- Non-custodial by design: Funds are locked in a smart contract and are never held by any company. This eliminates counterparty risk and ensures that Paycrest cannot access or misuse your users’ money.

- Zero fees for Senders: The protocol does not charge fees to Senders. The aggregator fee of 0.5% is built into the provider’s exchange rate, allowing your application to offer truly fee-free on and off-ramps to end users, providing a meaningful competitive advantage.

- Multi-chain, multi-stablecoin: Paycrest supports USDT and USDC across Ethereum, Base, Arbitrum, Polygon, BNB Smart Chain, Celo, Lisk, and Scroll. This ensures you are not limited to a single stablecoin issuer or blockchain.

- Automatic refunds: If an order fails for any reason, the protocol automatically returns the funds. There is no manual dispute process required.

- Built for emerging markets: Paycrest is live across six corridors: Nigeria (NGN), Kenya (KES), Uganda (UGX), Tanzania (TZS), Malawi (MWK), and Ghana (GHS), with more markets coming. These are exactly the regions where traditional payment rails are slowest and most expensive.

Start Building

If you’re building a product that touches cross-border payments, remittances, payroll, or stablecoin on/off-ramps, Paycrest is the routing layer. The protocol is live, processing real volume, and settling the majority of Nigerian Naira orders in under 30 seconds.

To get started, explore the Sender API Integration Guide, review the API Reference, and join the community on Telegram for support and updates.

The last mile of stablecoin payments is no longer broken. It’s an API call away.