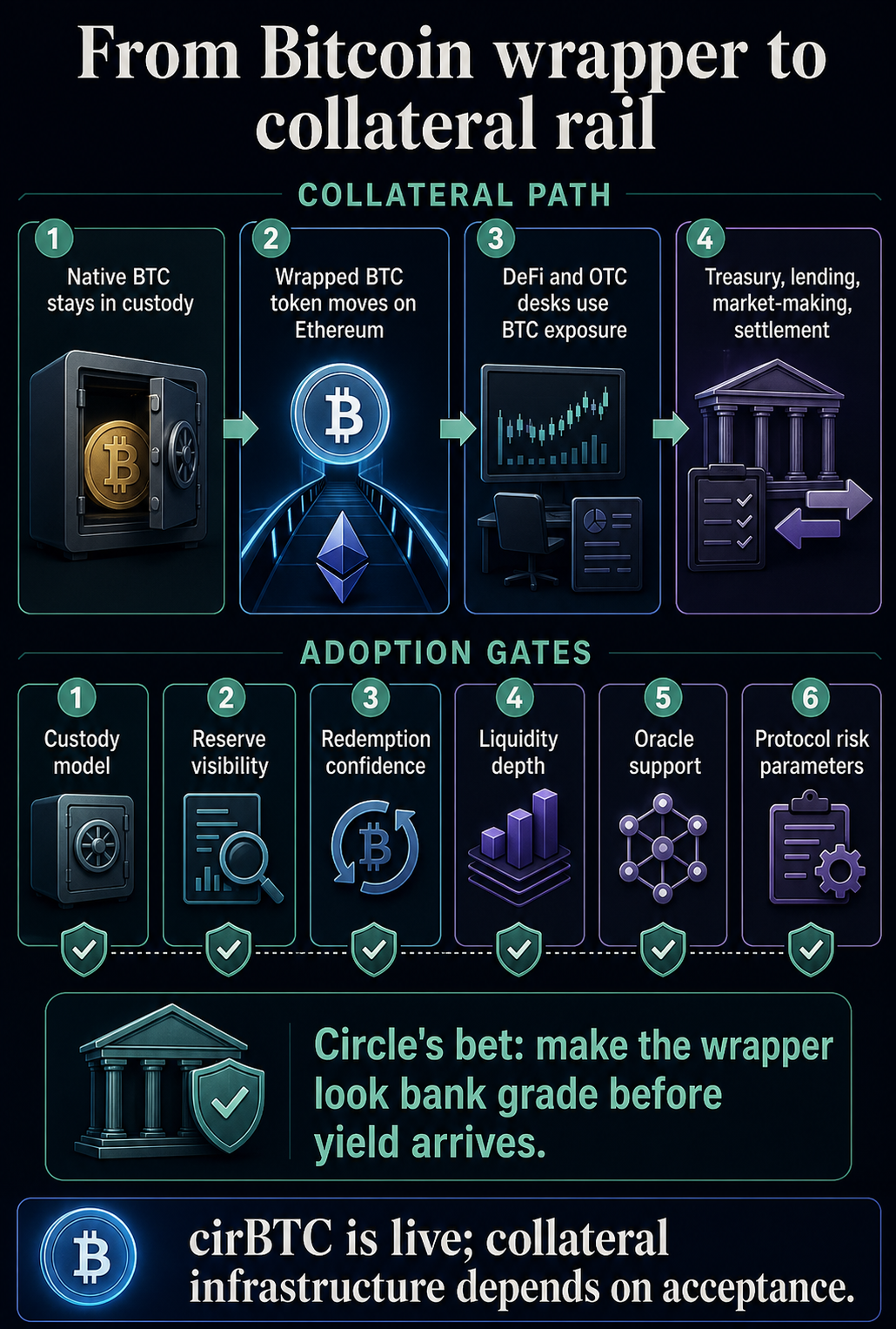

Circle has launched cirBTC on Ethereum, but the larger play is to make wrapped Bitcoin look like collateral infrastructure institutions can route through DeFi, OTC desks, lending markets, treasury systems, market makers, and settlement flows.

cirBTC is live on Ethereum and backed 1:1 by native BTC, according to Circle's launch materials. The company says the underlying Bitcoin is held through a Circle entity, segregated from corporate assets, and designed for onchain reserve visibility.

The product also sits inside Circle's existing stack. Circle is positioning cirBTC around Circle Mint, USDC workflows, Ethereum DeFi, and planned support for Arc and other chains.

This moves wrapped Bitcoin into an issue of trust. BTC itself does not move natively through Ethereum contracts, so any wrapped version asks users to trust a claim on Bitcoin held somewhere else.

For retail DeFi users, that can be a bridge decision. For institutions, it is a collateral decision: who holds the keys, how reserves are checked, what happens during redemption, and whether the operational process can survive internal risk review.

Circle is selling custody before yield

Circle's cirBTC pitch starts with the same basic promise as other wrapped Bitcoin products: one token for one BTC. The difference is the operating package around that promise.

Its materials say cirBTC is backed by native BTC, reserves are separated from corporate assets, and counterparties can verify reserves onchain. Circle also ties the product to the same institutional interface many firms already use for USDC issuance and redemption.

A desk that already moves USDC through Circle Mint could, in theory, add BTC collateral to the same account-and-settlement relationship instead of stitching together a separate custodian, wrapper, exchange, bridge, and DeFi access point.

The proof-of-reserve component supports that positioning. Proof of Reserve systems can help tokenized assets and DeFi protocols monitor backing data onchain and build safeguards around undercollateralization.

For cirBTC, the next live signal is the reserve feed or dashboard counterparties can use for the token itself.

That leaves counterparty trust in place. cirBTC still depends on custody, redemption, reserve controls, and user confidence in Circle's process.

The institutional pitch is that those assumptions can be packaged in a cleaner way, with the BTC claim, reserve visibility, and Circle account relationship pointing in the same direction.

The comparison is clearest against cbBTC and WBTC.

Coinbase's cbBTC is also a 1:1 BTC-backed wrapped asset, held in Coinbase custody and available across Base, Ethereum, Solana, and Arbitrum.

Coinbase also maintains a proof-of-reserves page, giving users a public reserve and supply reference for the product. Availability and terms can vary by jurisdiction.

WBTC remains the incumbent Bitcoin wrapper in Ethereum DeFi. Its own site presents WBTC as backed 1:1 by Bitcoin, with a public reserve dashboard and proof-of-reserve context.

Circle's opportunity sits in the trust bundle it can offer: the USDC issuer, Circle Mint, reserve transparency, Ethereum access, and future Arc support under one institutional brand.

| Product | Main trust promise | What is known now | Open test |

|---|---|---|---|

| cirBTC | Circle-backed BTC collateral for institutional workflows | Live on Ethereum, backed 1:1 by native BTC, with Circle stating reserve segregation and onchain visibility | Whether liquidity, protocol listings, and reserve feeds make it usable as collateral at scale |

| cbBTC | Coinbase custody and exchange-account workflows | Backed 1:1 by BTC held by Coinbase, with listed support across Base, Ethereum, Solana, and Arbitrum | Whether Circle can compete with Coinbase distribution and Base-native lending activity |

| WBTC | Incumbent DeFi collateral with public reserves | Backed 1:1 by BTC with a public reserve dashboard and proof-of-reserve context | Whether institutions prefer an incumbent DeFi asset or a Circle-controlled operating model |

The comparison shows why cirBTC is more than a token launch. Wrapped Bitcoin products increasingly compete on the legal and operational identity of the issuer, the visibility of reserves, and the pathways by which collateral enters lending markets.

Coinbase has already tied cbBTC to lending through Base. CryptoSlate reported that Coinbase and Morpho introduced Bitcoin-backed loans on Base, using cbBTC and USDC in a consumer-facing borrowing flow.

That comparison shows the distribution Circle has to challenge if cirBTC is to become more than another Ethereum asset.

Related Reading

Related Reading

Coinbase's cbBTC launches seeking DeFi boom on Base and Ethereum

Coinbase said its Bitcoin Wrapper product cbBTC is supported across major DeFi protocols, including AAVE. Sep 12, 2024 · Oluwapelumi AdejumoArc gives cirBTC a bigger role

Circle's Arc ambitions give cirBTC a second layer of meaning.

Arc is being pitched as infrastructure for stablecoin finance, with USDC fees, settlement tooling, privacy controls, and institutional use cases around payments, foreign exchange, tokenized assets, and capital markets.

Circle has described Arc as a chain purpose-built for stablecoin finance, and CryptoSlate has previously reported how the network pushes Circle deeper into territory also occupied by Coinbase and Base.

Related Reading

Related Reading

Circle adds $3 billion Wall Street Arc token risking an uncomfortable rivalry with Coinbase

A longtime stablecoin partnership is entering a new phase as Circle seeks to own more of the infrastructure around USDC. May 12, 2026 · Oluwapelumi AdejumoIn that context, cirBTC could become the Bitcoin leg of a broader Circle stack. USDC provides the dollar asset. Circle Mint provides issuance and redemption access. Ethereum provides current DeFi reach.

Arc, if it develops as planned, could give Circle a venue where tokenized dollars, BTC collateral, and settlement workflows operate with fewer handoffs.

The record remains early. Circle says cirBTC is live on Ethereum and points to planned Arc and multichain support. Its launch materials stop short of showing broad DeFi protocol adoption, live Arc usage for cirBTC, or a supply figure that would show market depth.

A token can be fully backed and still fail to become preferred collateral.

Institutions and DeFi protocols still need liquidity, risk parameters, redemption confidence, oracle support, and a clear reason to add another BTC wrapper beside existing options.

Related Reading

Related Reading

Kraken moves Bitcoin to Chainlink as bridge fears spread across DeFi

Kraken is rebuilding how Bitcoin moves through DeFi after the KelpDAO shock. May 15, 2026 · Liam 'Akiba' WrightThe broader market context is already moving in that direction. CryptoSlate recently framed a Morgan Stanley and Galaxy arrangement as part of Bitcoin's next institutional test in lending collateral.

The cirBTC launch fits that same issue: Bitcoin can become useful collateral for institutions when the custody and risk controls around the token are strong enough to satisfy the people managing the real BTC.

Arc also gives the Coinbase comparison more weight. Coinbase can route cbBTC through Base and its own account system; Circle is trying to offer a parallel route built around USDC, Mint, and Arc.

The adoption contest centers on which issuer can turn custody relationships into liquidity.

Acceptance decides whether the wrapper becomes infrastructure

Circle has the right ingredients for a bank-grade wrapper: a known issuer, reserve language, onchain verification, institutional access, USDC proximity, and an Arc roadmap.

Collateral infrastructure comes later, when counterparties use those ingredients in production.

That means lenders need to accept the asset, market makers need to quote it, treasury teams need clean redemption, DeFi protocols need collateral parameters, and risk desks need confidence in the reserve process.

Users also need to move between BTC exposure and dollar liquidity without wondering where the real Bitcoin sits.

That is where cirBTC will face WBTC and cbBTC. WBTC has incumbent DeFi familiarity. Coinbase has distribution, custody, and Base workflows.

Circle has USDC, Mint, compliance credibility, and an ambition to own more of the settlement stack through Arc.

Circle can turn wrapped Bitcoin into institutional collateral infrastructure if cirBTC becomes the wrapper institutions choose because the custody, reserve, and redemption model lowers operational friction.

If liquidity stays elsewhere and Arc remains future context, cirBTC will still read as a product launch rather than infrastructure.

For now, Circle has changed the frame around wrapped BTC. The debate now centers on who institutions trust to hold the Bitcoin while the token moves through programmable finance.

The post Circle wants wrapped Bitcoin to look bank grade before institutions trust it as collateral appeared first on CryptoSlate.