B3 registered the first guaranteed OTC flexible option tied to Hashdex's crypto-index ETF, HASH11, in a trade between Inter and XP.

B3's clearinghouse served as the central counterparty in the trade, placing a crypto ETF-linked exposure inside the same back-office machinery that handles counterparty risk, margining, clearing, and settlement.

That is the infrastructure layer that Wall Street is still asking US regulators to open to tokenized assets.

BlackRock submitted a response to the CFTC's tokenized-collateral initiative in 2025, arguing that tokenized money market funds and stablecoins should be eligible for use in both cleared and uncleared derivatives markets.

The most concrete version of this trade appeared offshore in April 2026, when Standard Chartered built a framework that allowed institutional OKX clients to post BlackRock's tokenized Treasury fund, BUIDL, as collateral while Standard Chartered retained custody of the assets.

HASH11 served as the underlying asset of the flexible option, a different structural role from the margin collateral position BlackRock is asking US regulators to open to tokenized assets.

Both moves center on how crypto-linked assets enter the machinery of clearing, settlement, and risk management.

| Market | Development | Asset role | Infrastructure layer | Why it matters |

|---|---|---|---|---|

| Brazil / B3 | Guaranteed OTC flexible option tied to HASH11 | Underlying asset | CCP, margining, clearing, settlement | Crypto ETF-linked exposure enters regulated derivatives plumbing |

| U.S. / BlackRock | Tokenized money market funds and stablecoins in derivatives markets | Collateral / margin | Cleared and uncleared derivatives collateral systems | Wall Street wants tokenized assets accepted in risk-management workflows |

| Offshore example | Standard Chartered / OKX / BUIDL collateral framework | Posted collateral | Custody + institutional collateral management | Shows the tokenized collateral model emerging outside U.S. rulemaking |

The HASH11 flexible option is customizable by maturity, strike, quantity, premium, and optional features such as barriers or limiters.

On May 6, B3 began accepting real estate investment funds as eligible collateral for CCP-guaranteed operations, bringing the eligible pool to roughly $146 billion. B3's collateral list already includes Brazilian exchange-traded ETF quotas under standard eligibility criteria.

Both decisions to expand eligible collateral and introduce HASH11 as a derivative underlier demonstrate how B3 is broadening the asset types that enter its regulated clearing and settlement framework.

Why Brazil earned this moment

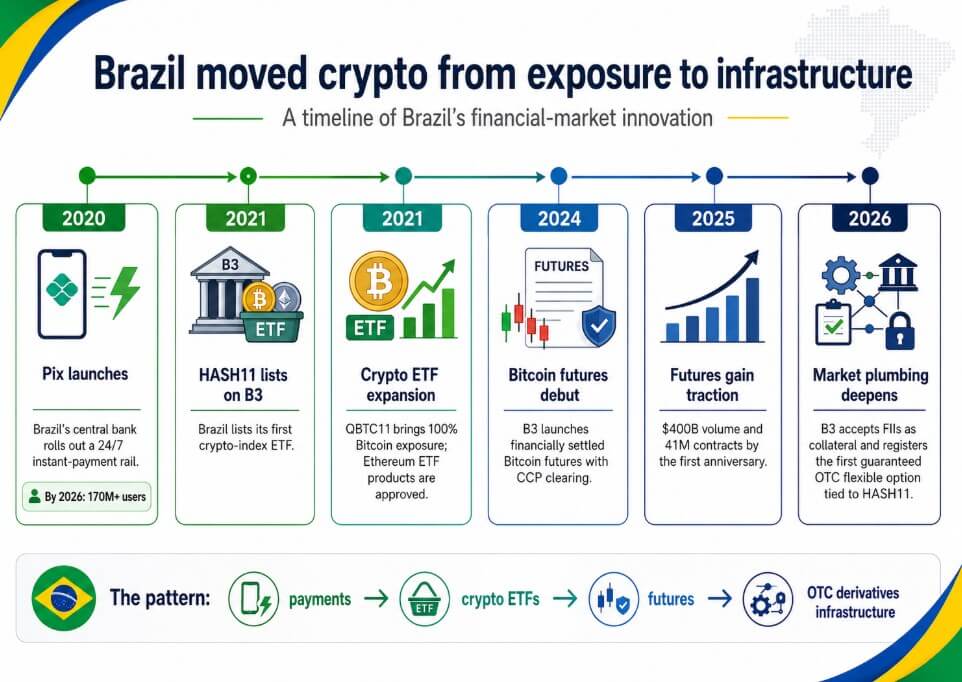

Brazil's ability to execute this trade rests on a financial system that has repeatedly adopted infrastructure-level innovations before larger markets finished debating them, with the clearest example being Pix.

Brazil's central bank launched the 24/7 instant-payment rail in 2020, and by 2024, Pix had processed more than $5 trillion and surpassed cash, debit cards, and credit cards as Brazil's leading payment method.

By 2026, the network had reached more than 170 million users across around 900 participating institutions, and Banco do Brasil had begun enabling Pix payments in Argentina.

The crypto ETF record followed the same arc, as Hashdex launched what Nasdaq described as the world's first crypto ETF on the Bermuda Stock Exchange in February 2021, and B3 listed HASH11 in April 2021 as Brazil's first crypto-index ETF.

QBTC11 began trading on B3 in June 2021 as the exchange's first ETF with 100% Bitcoin exposure. QR Asset marketed QSOL11 as the world's first spot Solana ETF, and Brazil approved Ethereum ETF products in 2021, years before US spot Ethereum ETFs became standard market infrastructure.

Bitcoin futures debuted on B3 in April 2024 with financial settlement, and the stock exchange acted as the CCP. By the first anniversary, $400 billion in trading volume and 41 million contracts had established the product as a functioning hedging market, with non-resident investors accounting for 53% of participation, individuals for 39%, and funds for 7%.

What Wall Street sees in this

Collateral, clearing, margin, and settlement are the systems that let institutions hedge, lever and manage risk at scale, representing crypto adoption's next phase.

That is exactly the infrastructure layer BlackRock is working to modernize in Washington, and it is exactly where Brazil has been building for four years.

When BlackRock argues that tokenized assets should enter derivatives collateral systems, the claim is that crypto-linked financial products are mature enough to operate within risk-management infrastructure, and Brazil's record supports that empirically.

B3 has a CCP, margining and settlement frameworks, crypto futures with $400 billion in volume, and now a guaranteed OTC flexible option tied to a crypto ETF inside the same clearinghouse stack.

Brazil's innovation stack, consisting of Pix for payments, B3 for listed and OTC market infrastructure, crypto ETFs for regulated exposure, and Bitcoin futures for hedging, operates as a coherent whole rather than isolated bets.

How far the plumbing extends

In the bull case, B3's infrastructure stack becomes a reference model for how crypto-linked assets can graduate into regulated clearing machinery, more crypto underliers enter OTC flexible options, and the collateral menu broadens.

A measurable threshold, such as crypto-linked OTC notional reaching 1% to 5% of B3's guaranteed flexible-options stock within the next 12 to 24 months, would confirm the HASH11 option has moved from a one-off institutional trade into a functioning market segment.

| Scenario | What happens next | Signal to watch | Article implication |

|---|---|---|---|

| Bull case | More crypto underliers enter OTC flexible options; collateral menu broadens | Crypto-linked OTC notional reaches 1%–5% of B3’s guaranteed flexible-options stock | Brazil becomes a reference model for regulated crypto derivatives plumbing |

| Base case | HASH11 options repeat, but remain institution-focused | A handful of new trades, mostly bespoke | Brazil is ahead, but adoption is gradual |

| Bear case | Liquidity, volatility and margin constraints limit expansion | Collateral pool remains dominated by Selic federal debt | Crypto stays mostly in wrappers, not core market plumbing |

| Black-swan case | Market shock or regulatory caution triggers tighter eligibility | Higher haircuts, fewer eligible products, slower approvals | Crypto infrastructure narrative stalls |

In the bear case, B3's $146 billion collateral pool was more than 82% Selic federal debt as of May 2026, and crypto-linked exposure carries liquidity and volatility characteristics that work against it in the core collateral stack, where margin requirements and haircuts are the binding constraint.

If regulatory caution tightens eligibility or liquidity proves thin, the HASH11 OTC option stays a bespoke institutional product, and crypto stays in investment wrappers.

Brazil laid the groundwork for this infrastructure race, enabling financial innovations to move quickly from experiment to functioning market infrastructure, while BlackRock is still making its regulatory case in Washington.

The distance between where Wall Street wants to go and where Brazil already is keeps widening.

The post Brazil just moved a crypto ETF into market plumbing Wall Street still wants opened appeared first on CryptoSlate.