Written by Zoltan Vardai,Staff Writer

Written by Zoltan Vardai,Staff Writer Reviewed by Bryan O'Shea,Staff Editor

Reviewed by Bryan O'Shea,Staff EditorBitcoin whales shift $100M+ as oil spike rattles markets

55 minutes agoAncient Bitcoin holders moved millions to exchanges as Middle East tensions drove oil higher, fueling a broader risk-off shift across crypto and traditional markets.

Cointelegraph in your social feed

Subscribe on Subscribe onAncient Bitcoin holders moved tens of millions of dollars to exchanges as Bitcoin fell and energy prices jumped after attacks on Gulf oil and gas infrastructure deepened the conflict involving Iran, Israel and the United States.

Ancient whale “bc1ql” sent 1,000 Bitcoin (BTC), worth around $71 million at current prices, to Binance on Wednesday, according to blockchain data platform Arkham. The whale initially bought 5,000 BTC 13 years ago and still holds about 1,500 BTC worth about $106 million, according to blockchain analytics platform Onchain Lens.

The same day, one of the earliest Bitcoin holders, Owen Gunden, also transferred 650 BTC ($46 million) to crypto exchange Kraken, marking his first large sale in five months, when he sold a total of 11,000 BTC ($1.12 billion), according to analytics platform Lookonchain.

The transfers added to signs of profit-taking among some long-term holders as traders reacted to a broader risk-off move driven by the Middle East energy shock.

The whale movements follow reports of Israel striking Iran’s giant South Pars gasfield on Wednesday, after killing Iran’s intelligence minister, Esmail Khatib, the third senior Iranian figure assassinated over the past few days, the BBC reported. South Pars is part of the world’s largest natural gas field, with Qatar and Iran both operating facilities in the area.

After the strikes, Brent crude rose above $119 a barrel before easing to about $114.77, while WTI briefly touched $100 and later traded near $96.59, according to data from Trading Economics.

Wholesale gas prices in Europe and the UK also spiked after Iran attacked Qatar’s Ras Laffan natural gas complex on Wednesday and Thursday, reported Bloomberg.

Related: Binance says US midterms could boost Bitcoin and stocks

Bitcoin sell-off began after attack on Qatar gas complex

Bitcoin’s latest sell-off occurred shortly after Iran’s strike on Qatar’s energy infrastructure, according to Aurelie Barthere, principal research analyst at crypto intelligence platform Nansen.

“BTC began to sell off yesterday around noon CET, following the escalation of the war between Iran and Israel and the attack on gas infrastructure in Qatar, ” she told Cointelegraph, adding:

“If we fail to hold the $70K–$71K level, we could return to the previous range of approximately $60K–$71K.”

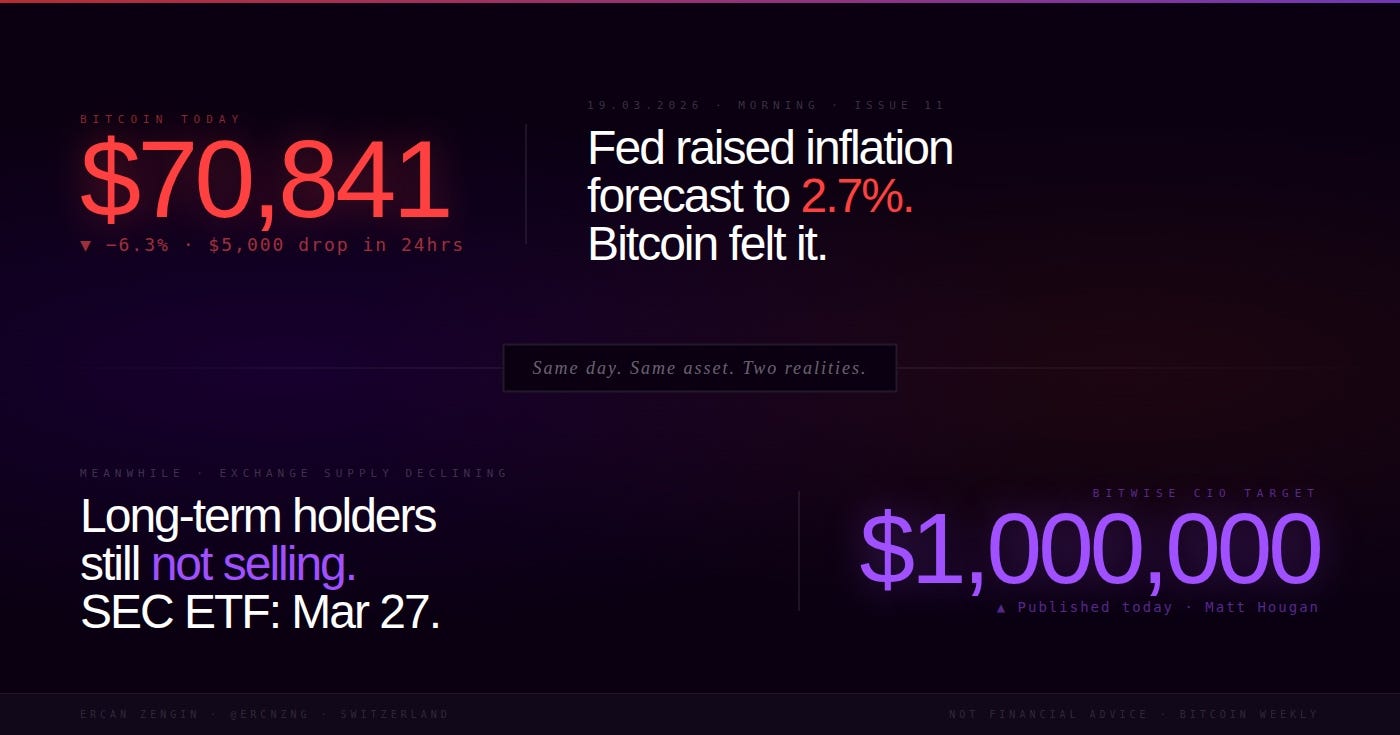

Bitcoin’s price fell 5% during the past 24 hours and was trading at $70,439 as of 10:15 a.m. UTC, according to CoinMarketCap data.

Bitcoin’s decline mirrored a 4.2% drop in gold prices over the past 24 hours, as the leading precious metal traded at $4,686 per oz on Thursday, according to Gold Price data.

The simultaneous drop of the two assets suggests that investors are staging a “broader risk-off move” rather than a pivot to safe-haven assets, Alvin Kan, chief operating officer at Bitget Wallet, told Cointelegraph.

Magazine: Bitcoin’s ‘biggest bull catalyst’ would be Saylor’s liquidation — Santiment founder

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently. Read our Editorial Policy https://cointelegraph.com/editorial-policy