BIS Project Agorá Just Reimagined Cross-Border Payments. One Question Remains.

Yash Hiranandani7 min read·Just now

Yash Hiranandani7 min read·Just now--

On May 27, 2026, the Bank for International Settlements published its technical findings on Project Agorá — a public-private prototype built with 7 central banks and 40+ financial institutions, designed to rethink the plumbing of cross-border wholesale payments.

The paper is dense. Most industry coverage of it isn’t. What follows is a product perspective on what Agorá actually solves, the trade-offs it makes, and the critical problem it intentionally defers.

The 320 Trillion USD Bottleneck

Wholesale cross-border payments, the kind of payments that move between banks and financial institutions rather than retail consumers, accounted for 91% of all cross-border payment value in 2023. By 2032, that figure is projected to reach $320 trillion.

Yet the underlying correspondent banking infrastructure remains plagued by structural drags.

The problems are neither new nor secret:

- Fragmented, siloed liquidity spread across correspondent banking chains.

- Sequential processing bottlenecks, where each leg of a payment waits for the previous one to complete.

- Limited transparency into fees, routing decisions, and payment status while funds are in transit.

- Compliance screening false positives that can freeze legitimate payments for days.

- Float risk, where capital becomes stranded in suspense accounts when a payment breaks down somewhere along a chain of intermediaries, sometimes for weeks.

These are not edge cases. They are the operating conditions of global trade.

The Core Hypothesis

The hypothesis is elegant. What if commercial bank deposits were tokenized, a unified settlement layer connected participating central banks and commercial banks, and atomic settlement ensured that cross-border payments either completed entirely or failed cleanly, with nothing in between?

The core mechanism is a distributed ledger where funds remain locked in the sender’s own account until a final trigger fires simultaneously across all participating parties.

No capital moves until every leg of the transaction is verified, compliance checked, and ready to execute.

All or nothing. Commit or cancel. The BIS paper calls this coordinated execution.

In product terms, what it produces is a deterministic state machine. Cross-border payments resolve to a strict pass or a strict fail, with mathematical guarantees around data integrity and no mid-flight fee leakage.

The Genuine Wins

Before getting to the gaps, the wins deserve to be named clearly, because they are real and significant.

1. Zero financial float risk

In today’s SWIFT network, if a payment breaks down mid-flight because an intermediary bank rejects it, capital can get stuck in a suspense account or legal limbo for days or weeks.

In Agorá, because funds are locked in your own account until the final trigger fires, the risk of money vanishing mid-transit is mathematically eliminated.

That’s not a marginal improvement. That’s a structural change.

2. The death of the asynchronous unwind

Decoupling the data exchange from the actual settlement means banks line up compliance verification, exact currency amounts, and payee confirmation before committing a single cent of liquidity.

If a payment fails, it aborts cleanly at the data layer.

It does not force a chain of banks to manually reverse and unwind transactions that have already partially settled.

3. No half-baked outcomes

The commit-or-cancel architecture ensures strict multi-ledger synchronization.

The nightmare scenario where the USD leg of a transaction successfully clears but the JPY leg fails, leaving one party exposed to overnight currency risk or counterparty default, is architecturally prevented.

For high-value treasury flows, where settlement certainty is worth the operational overhead, this is a genuinely better architecture than anything that exists today.

Where the Agorá Blueprint Meets Reality

Here is where the press release ends and the paper begins.

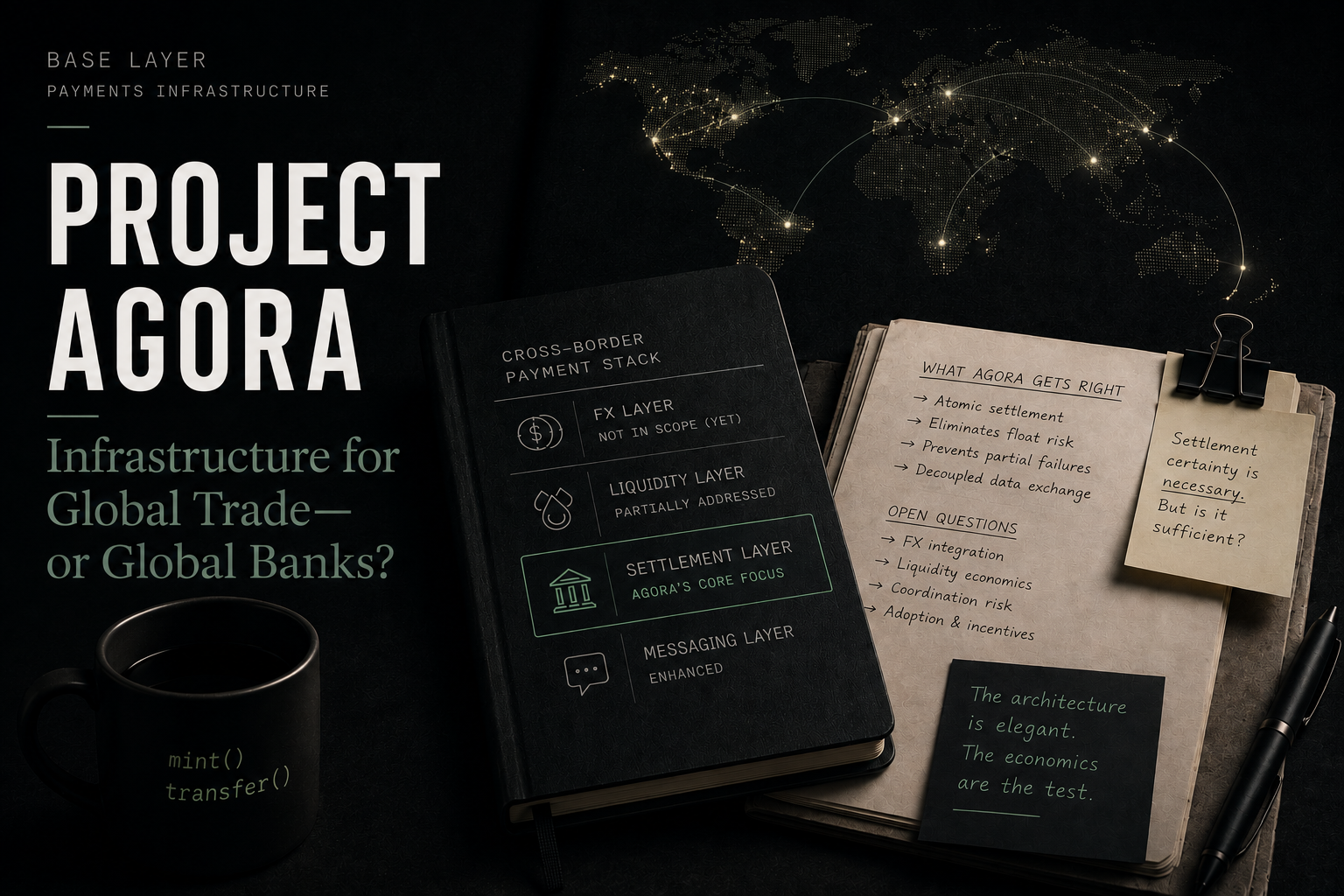

1. The Deferred FX Elephant

This is the most significant gap in the POC and the one least discussed in coverage of Project Agorá.

Cross-border payments are, at their core, a foreign exchange problem. You are moving value denominated in one currency into a settlement denominated in another. The rate, the timing, and the counterparty for that conversion are central to the economics of every transaction.

The Project Agorá blueprint explicitly defers FX integration to a later phase.

For a payment architect building a system designed to reimagine correspondent banking infrastructure, leaving FX out of the proof of concept is roughly equivalent to building a new aircraft and noting that the engine integration will be addressed in phase two.

2. The Triple-Ledger Reconciliation Paradox

Today, correspondent banking requires reconciliation between a bank’s core ledger and the RTGS (Real-Time Gross Settlement) system.

Agorá adds two new layers: the unified tokenized settlement layer and a jurisdictional layer for each participating central bank.

The reconciliation overhead doesn’t decrease. It multiplies.

This could be a material operational cost for banks with existing reconciliation teams and systems.

3. The Coordinated Execution Chokepoint

The atomic settlement model requires all participating banks’ middleware to be operational simultaneously.

If one bank’s middleware or banking API goes down mid-coordination, the entire transaction stalls.

SWIFT’s failure mode is asynchronous fragility. Payments get stuck and require manual unwinding.

Agorá’s failure mode is synchronous fragility. The entire coordinated transaction freezes when any single participant has a system issue.

This is a different failure mode, not a safer one. Its systemic ripple effects across tightly linked multi-currency corridors are harder to isolate.

4. The Always-On RTGS Illusion

Project Agorá promotes 24/7 cross-border payment capability as a core benefit.

But the tokenized issuance mechanism depends on RTGS availability. RTGS (Real-Time Gross Settlement) systems are the central bank-operated payment rails that commercial banks use to settle money with finality.

Most central bank RTGS systems have operating hours, maintenance windows, and occasional outages.

An always-on payment network with an operating-hours dependency at its issuance layer is not, in practice, always on.

5. The Sanctions “Tipping-Off” Contradiction

Agorá attempts to parallelize compliance checks by having banks broadcast binary pass/fail flags (Flag 0 or Flag 1) within a transaction’s privacy group.

The paper openly admits that multiple participating banks flagged this as a legal hazard.

Sharing a compliance failure outcome across counterparties could violate strict domestic anti-tipping-off laws during active AML or sanctions investigations.

The Defensible Trade-Off

Project Agorá is not a broken system. It is a classic engineering exercise in balancing trade-offs.

It gives up capital liquidity flexibility, because funds must be pre-committed before settlement can proceed, in exchange for absolute settlement certainty and operational predictability.

That trade-off is exactly the right choice for specific use cases.

High-value, low-frequency treasury transactions, where the cost of a failed settlement far exceeds the cost of pre-funding.

However, it is a much harder case to make for high-volume, lower-value flows such as SME cross-border payments, supplier payments, and cross-jurisdiction payroll.

In these corridors, the operational overhead of three-way reconciliation and intensive pre-funding requirements can easily outweigh the savings from fewer settlement failures.

The prototype proves the settlement layer works. It does not prove the system works end to end, at scale, across the payment flows that carry the most economic weight for the people who need it most.

The Exporter’s Dilemma

If you were a product manager building a premium treasury platform on top of Project Agorá, would a system that virtually eliminates settlement failures be worth the liquidity planning, middleware coordination, and reconciliation overhead it requires?

For a CFO managing $50 million in treasury flows across six convertible currencies, the answer is probably yes.

For a mid-sized exporter in Vietnam paying forty suppliers across fragmented emerging-market corridors, the answer is less obvious. The exporter does not care about settlement architecture.

They care about cost, working capital, liquidity access, and whether money arrives when expected.

Settlement velocity matters. It is simply not the only outcome that matters. That is where the economics of the platform begin to matter.

The question is not whether settlement certainty is valuable. It clearly is. The question is whether the capital and operational costs required to achieve that certainty are justified for every payment flow.

Project Agorá has built something technically remarkable at the settlement layer. But the next phase needs to answer a much harder question.

Who does this platform actually serve, at the capital economics it requires?

The answer will determine whether Agorá becomes infrastructure for global trade, infrastructure for global banks, or both.

The Honest Limits of the Argument

The counter-argument to this critique is that these structural frictions may simply be the accepted constraints of an early-stage prototype.

The BIS paper explicitly categorizes liquidity management solutions, such as adapting offsetting and netting features from traditional RTGS systems into DLT (distributed ledger technology) workflows, as high-priority areas for future exploration.

If central banks successfully layer native liquidity optimization mechanisms and integrated FX workflows directly into the unified ledger layer in a future phase, many of today’s capital-efficiency and coordination concerns could be significantly reduced.

What appears today as an architectural bottleneck could ultimately prove to be a temporary implementation constraint.

Originally published on Base Layer on Substack. I write about financial infrastructure, payments, digital assets, and the market forces that shape them through a product management lens at Base Layer.

Find me on LinkedIn.