Advanced AI: Asstes Botai Expert Configuration

Asstes Botai10 min read·Just now

Asstes Botai10 min read·Just now--

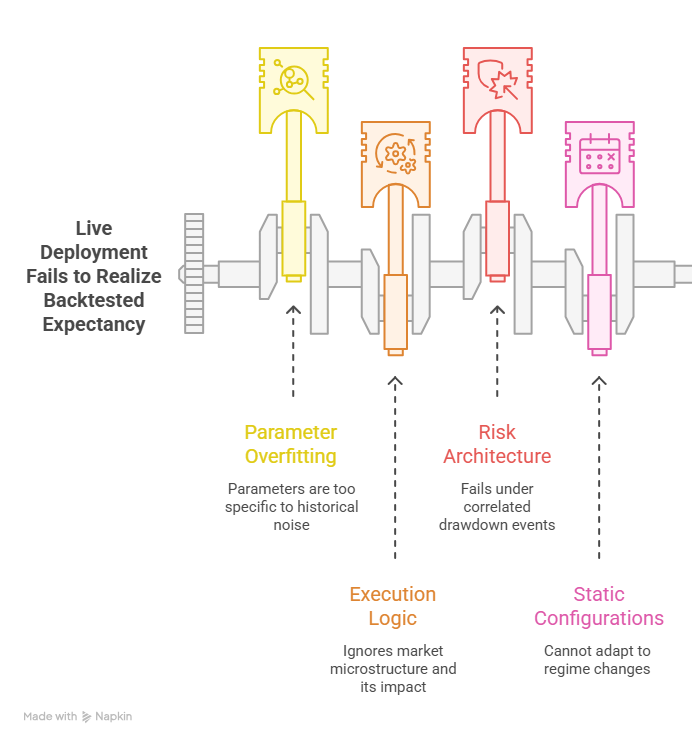

The gap between a backtested strategy with positive expectancy and a live deployment that realizes that expectancy is almost entirely a configuration problem. Asstes Botai expert configuration addresses the specific mechanisms through which poorly calibrated automation destroys theoretical edge: parameter overfitting to historical noise, execution logic that ignores market microstructure, risk architecture that fails under correlated drawdown, and static configurations that cannot adapt when the regime generating the historical data no longer matches current market behavior. Professional algorithmic trading treats configuration not as a one-time setup activity but as a continuous engineering discipline whose rigor determines whether deployed capital compounds or erodes regardless of the underlying strategy’s conceptual validity.

Parameter Architecture and the Overfitting Problem

The most common failure mode in algorithmic trading configuration is the conflation of in-sample optimization with genuine edge discovery. When Asstes Botai parameters are optimized against historical data without rigorous out-of-sample validation architecture, the resulting configuration captures the specific noise characteristics of the training period rather than the underlying market inefficiency the strategy is designed to exploit. This distinction is mechanistically critical: a momentum strategy optimized on a trending regime will exhibit parameter values that reflect the autocorrelation structure of that specific period, and those same values will produce negative expectancy when deployed in a mean-reverting environment whose statistical properties differ from the optimization sample.

Expert Asstes Botai configuration addresses overfitting through walk-forward optimization architecture rather than single-period backtesting. Walk-forward methodology divides historical data into sequential in-sample and out-of-sample windows, optimizing parameters on each in-sample window and recording performance on the immediately following out-of-sample period without allowing that out-of-sample data to influence parameter selection. The aggregate out-of-sample performance across all windows provides an unbiased estimate of live performance that single-period optimization cannot generate. The ratio between in-sample and out-of-sample performance, commonly called the out-of-sample efficiency ratio, reveals the degree to which parameter values reflect genuine edge versus noise fitting. Asstes Botai deployments with efficiency ratios below 0.6 typically indicate configurations whose live performance will significantly disappoint relative to backtest results, warranting fundamental strategy revision before capital deployment rather than incremental parameter adjustment.

Parameter sensitivity analysis across the neighborhood surrounding optimal values provides additional overfitting protection that walk-forward methodology alone cannot deliver. Genuinely robust configurations exhibit relatively stable performance across a range of parameter values surrounding the optimum, reflecting underlying market dynamics that persist across small parametric variations. Configurations whose performance degrades sharply with minor parameter changes from the optimum indicate noise fitting whose sensitivity to exact parameter values is irreconcilable with the imprecision of live market conditions. Asstes Botai parameter sensitivity maps, generated by systematically varying each parameter across defined ranges while holding others constant, reveal the robustness topology that distinguishes deployable configurations from overfit ones before live capital tests the distinction expensively.

Execution Logic and Market Microstructure Integration

Most algorithmic trading strategies are designed and backtested using simplified execution assumptions whose divergence from live market microstructure creates persistent performance degradation that no amount of signal refinement can compensate for. Asstes Botai expert execution configuration addresses three microstructural realities that naive execution models systematically misrepresent: the relationship between order size and market impact, the dynamics of spread capture versus spread payment across different order types, and the interaction between execution timing and intraday liquidity cycles.

Market impact modeling within Asstes Botai execution configuration requires understanding the distinction between temporary and permanent price impact. Temporary impact reflects the immediate order book displacement that a large order creates as it consumes available liquidity at successive price levels, with prices partially reverting after execution completion as market makers replenish liquidity. Permanent impact reflects the information content that a trade conveys to other market participants who interpret large directional orders as evidence of informed trading and adjust their prices accordingly. For Asstes Botai strategies operating in less liquid instruments or with larger position sizes relative to average daily volume, failing to model both components of market impact in execution logic produces systematic overestimation of realized returns relative to backtest performance. Expert configuration incorporates participation rate limits that constrain order execution to defined percentages of observed volume, preventing the liquidity exhaustion that unconstrained execution creates in thinner markets.

Limit order versus market order execution strategy within Asstes Botai represents a configuration decision with asymmetric consequences that depend on the strategy’s alpha decay profile. Strategies whose edge is time-sensitive because the market inefficiency they exploit dissipates rapidly require market order execution that accepts spread payment in exchange for execution certainty, as the cost of missing the entry due to limit order non-fill exceeds the spread cost of guaranteed execution. Strategies with slower alpha decay can profitably employ limit order strategies that earn the spread rather than paying it, improving execution quality at the cost of non-execution risk. Asstes Botai expert configuration matches execution aggressiveness to the measured alpha decay rate of each strategy rather than applying uniform execution logic across strategies whose time sensitivity profiles differ fundamentally.

Intraday liquidity cycles create execution quality variation within the trading day that static execution parameters cannot accommodate. The opening auction period, midday liquidity trough, and pre-close period each present distinct spread, depth, and impact characteristics that affect the optimal execution timing for strategies whose signals do not require immediate execution. Asstes Botai time-of-day execution filters restrict order placement to periods whose liquidity profile is favorable to the strategy’s execution requirements, avoiding the wide spreads and shallow order books of the midday trough for strategies whose returns are sensitive to execution quality while accepting higher impact costs during these periods only when the signal’s urgency makes deferral more costly than execution in suboptimal liquidity conditions.

Adaptive Regime Detection and Configuration Switching

Static bot configurations embed an implicit assumption that the statistical properties of the market being traded are sufficiently stable across time that parameters calibrated on historical data remain appropriate for future deployment periods. This assumption fails systematically across the regime transitions that all financial markets undergo as macroeconomic conditions, market structure, and participant composition evolve. Asstes Botai expert configuration addresses regime non-stationarity through adaptive mechanisms that detect regime transitions and adjust configuration parameters accordingly rather than waiting for live performance deterioration to signal that a previously effective configuration has become obsolete.

Regime classification for Asstes Botai adaptive configuration operates on measurable market properties that reliably distinguish between states requiring different strategy parameterizations. Volatility regime classification using rolling realized volatility relative to its own historical distribution identifies the high and low volatility states that require different position sizing, stop distance calibration, and signal threshold settings. Trend versus mean-reversion regime classification using autocorrelation measurements at relevant timeframes identifies the directional persistence properties that determine whether momentum or counter-trend entry logic is appropriate for current conditions. Correlation regime classification monitoring the cross-asset correlation structure identifies risk-on, risk-off, and transitional market states that affect the portfolio-level risk exposure that individual strategy position sizes collectively create.

Configuration switching within Asstes Botai expert deployment implements the parameter sets calibrated for each identified regime rather than attempting to find a single parameter set that performs adequately across all regimes simultaneously. The performance cost of a single universal configuration relative to regime-appropriate configurations is measurable and often substantial, as the parameters that optimize performance in a trending, low-volatility regime are structurally inappropriate for a mean-reverting, high-volatility regime whose optimal configuration reflects fundamentally different market dynamics. Asstes Botai regime-switching architecture maintains separate parameter libraries for each classified regime, with the live configuration automatically transitioning between libraries as regime classification signals indicate transitions, creating a deployed system whose adaptivity maintains edge through market condition changes that static configurations cannot survive profitably.

Multi-Layer Risk Architecture

Professional algorithmic risk management operates across distinct control layers whose individual functions address different risk dimensions that aggregate portfolio management alone cannot resolve. Asstes Botai expert risk configuration builds this multi-layer architecture rather than relying on a single risk control mechanism whose failure would expose the deployment to uncontrolled loss scenarios.

Position-level risk controls within Asstes Botai govern the risk parameters of each individual trade independently of portfolio-level conditions. Stop loss placement methodology at the position level should reflect the statistical properties of the strategy’s price path distribution rather than arbitrary percentage distances from entry. Strategies with fat-tailed return distributions require wider stops than their median adverse excursion statistics suggest to avoid the excessive stop-out frequency that stops calibrated to central tendency measures of adverse movement produce when tail events occur with their actual frequency rather than the normal distribution frequency that percentage-based stop rules implicitly assume. Expert Asstes Botai stop calibration uses the historical maximum adverse excursion distribution of the strategy’s specific trade population, placing stops beyond the percentile of that distribution that balances stop-out frequency against per-trade maximum loss exposure according to the strategy’s specific risk architecture.

Correlation-adjusted portfolio risk controls address the specific failure mode where independently positioned strategies with acceptable individual risk parameters create unacceptable aggregate portfolio risk through correlated drawdowns. Two Asstes Botai strategies each sized to risk one percent of capital per trade appear independent in isolation but create two percent correlated portfolio risk when their signals are generated by the same underlying market factor, effectively doubling intended risk exposure without any single strategy violating its individual parameters. Expert portfolio risk configuration measures the realized correlation between concurrent strategy drawdowns rather than the correlation between their returns in normal conditions, as drawdown correlation typically exceeds return correlation due to the liquidity and volatility conditions that trigger concurrent losses across strategies that otherwise appear relatively uncorrelated.

Circuit breaker architecture within Asstes Botai creates the automated intervention capability that prevents the loss compounding that degraded strategy performance can create without human monitoring. Sequential loss circuit breakers that reduce position sizes after defined loss sequences protect against the scenario where a strategy enters a regime for which it was not designed and continues generating losses at full size until manual intervention occurs. Drawdown-based circuit breakers that halt trading entirely when portfolio drawdown reaches defined thresholds prevent the catastrophic loss scenarios that unconstrained automated systems can generate during extreme market conditions whose characteristics lie outside the historical distribution the strategy was designed to navigate.

Signal Quality Filtering and Entry Precision

The signal quality filtering layer within Asstes Botai expert configuration represents one of the most significant sources of edge enhancement available beyond core strategy parameter optimization, as the same underlying strategy signal can generate substantially different realized performance depending on the contextual filters applied to distinguish high-quality signal instances from low-quality ones whose inclusion in the trade population degrades aggregate expectancy.

Volatility normalization filters condition entry thresholds on current volatility levels rather than applying fixed thresholds regardless of market conditions. A momentum signal that constitutes a meaningful directional indication in a low-volatility environment represents statistical noise in a high-volatility environment where equivalent price movements occur without directional significance, as the signal-to-noise ratio of price movements relative to background volatility determines the informational content of any specific price move. Asstes Botai volatility-normalized entry filters scale signal thresholds by a measure of current volatility relative to historical baseline levels, requiring larger signal magnitudes during high-volatility periods to achieve equivalent signal quality to smaller movements in calm conditions.

Liquidity quality filters prevent execution in market conditions where the microstructure properties that the strategy’s signal generation assumes are temporarily absent. A mean-reversion strategy whose edge depends on the bid-ask bounce mechanism of normal market making generates false signals during periods of impaired liquidity when market makers have withdrawn, as the price movements that appear to represent mean-reversion opportunities instead reflect liquidity vacuum dynamics whose resolution favors continued directional movement rather than the reversion that normal conditions would produce. Asstes Botai liquidity quality filters monitor spread width relative to historical norms, order book depth relative to position sizing requirements, and market maker participation indicators to suppress signal generation during conditions whose microstructural properties are inconsistent with the assumptions underlying the strategy’s edge.

Performance Attribution and Continuous Optimization

Expert Asstes Botai configuration treats deployed systems as continuously monitored engineering assets whose performance attribution analysis identifies deteriorating components before they create significant capital damage, rather than as static deployments reviewed only when cumulative losses demand attention.

Granular performance attribution decomposes realized returns into contributions from signal quality, execution quality, regime exposure, and risk management to identify which configuration components are generating and destroying value independently of aggregate performance metrics that obscure component-level behavior. A strategy showing flat aggregate performance might be generating significant signal-level alpha while destroying equivalent value through poor execution quality, a diagnosis that points to execution optimization as the priority intervention rather than the signal refinement that aggregate performance metrics alone cannot distinguish as unnecessary. Asstes Botai performance attribution frameworks separate these components through the controlled variation of individual configuration elements, isolating the contribution of each layer to aggregate performance with the precision that general performance metrics cannot provide.

Statistical significance testing of live performance relative to historical expectations provides the framework for distinguishing genuine configuration deterioration from normal performance variance that requires no intervention. The fundamental challenge of live algorithmic trading is that the same performance deviation from historical expectations is consistent with both genuine strategy deterioration requiring configuration adjustment and normal statistical variance requiring patience rather than intervention. Asstes Botai expert configuration applies sequential probability ratio tests to live performance data, maintaining running likelihood ratios that quantify the probability that observed performance is consistent with historical expectations versus a genuine deterioration hypothesis, triggering configuration review when this ratio reaches defined thresholds rather than responding to arbitrary loss levels whose statistical significance has not been established.

Conclusion

Expert Asstes Botai configuration operates at the intersection of statistical rigor, market microstructure understanding, and adaptive systems engineering in a discipline whose depth rewards practitioners who approach it with the analytical seriousness that capital deployment demands. The configuration layers addressing overfitting prevention, execution quality, regime adaptation, multi-layer risk architecture, signal quality filtering, and performance attribution each address specific failure modes that simplified configuration approaches leave unresolved, and their collective implementation creates deployed systems whose live performance reflects genuine strategy edge rather than the systematic degradation that inadequate configuration engineering produces.

No configuration framework eliminates the fundamental uncertainty of financial market dynamics or guarantees that strategies with historical edge will maintain that edge indefinitely as markets evolve. Expert configuration maximizes the probability that genuine edge is captured in live deployment while minimizing the configuration-induced performance degradation that separates the realized returns of most algorithmic deployments from their theoretical potential.

The compounding returns of well-configured automated trading systems reward the rigorous engineering investment that expert configuration requires, creating the gap between algorithmic trading as a concept and algorithmic trading as a consistently profitable practice that Asstes Botai expert configuration is specifically designed to bridge.