7,000 Points for the S&P 500 and the Triumph of Monetarism: Why Classic Crises Are a Thing of the Past

Introduction: The Milestone That Went Unnoticed

The global financial market has literally just stepped over a most significant historical threshold. Although, to be honest, many simply failed to notice this event. While conservative economists are searching in a panic for signs of a “bubble,” and professional apocalyptists are predicting an inevitable repeat of 1929, the current reality demonstrates to us a striking, I would even say, fundamental paradox. Fresh data on retail sales show absolutely zero growth, and consumer demand in the United States is, in essence, stagnating. And yet, stock indices are synchronously storming the stratosphere.

To understand why the market is right in this case, ignoring the “bad” news, we must acknowledge one key fact. The rules of the game have changed forever. It is my belief that since 2008 we have been living in a world where monetarism has secured a final and irrevocable victory. Consequently, old economics textbooks can be officially sent to the dustbin of history.

The “Last War” Trap: Why 1929 Will Not Happen Again

The majority of investors today are making one and the same systemic error. They are stubbornly preparing for the “last war.” When they see a slowdown in the real economy, their brains automatically paint grim pictures of the Great Depression. This means soup lines, mass unemployment, and a 90% collapse in quotes.

But between 1929 and the present day, there exists a critical, insurmountable difference. In the era of the Great Depression, the world lived by the rules of a rigid gold standard. The money supply was physically tied to the metal in the vaults of central banks. When the crisis of confidence began, the Fed was powerless. It could not simply print dollars to plug holes in bank balance sheets. Simply because it did not have that much gold. A deflationary collapse occurred: there was less money than accumulated debts. The system imploded.

In 2008, Ben Bernanke applied a completely new “cure.” As soon as credit markets froze, the Fed literally flooded the fire with liquidity. This scenario was brought to its absolute in 2020. Now, in any unclear situation, the regulator presses the “Print” button. A classic deflationary crash has become physically impossible. The risk of liquidity vanishing has been reduced to zero by the actions of regulators.

The “Debt Vacuum” Theory and the New Formula of Money

The primary theoretical error of modern “bears” lies in the misunderstanding of exactly how the modern monetary system functions. Fisher’s classic formula — $MV = PQ$ — is hopelessly outdated. It naively assumes that money is needed only to service the real turnover of goods.

In reality, we are dealing with a completely new formula:

$MV = PQ + Debts$

The modern economy is a gigantic debt pyramid. Money is needed not only for buying bread, but also for servicing trillion-dollar obligations. The credit market possesses the property of a “vacuum cleaner.” As soon as the slightest stress is noted in the economy, debts begin to suck in all available liquidity. If the Central Bank does not expand the monetary base, this vacuum cleaner will momentarily suck the money out of the real sector.

Today, regulators have finally understood: for the system not to explode, the volume of liquidity must grow at an outstripping pace. This is necessary to cover both the commodity mass and the inflated debt market. In my opinion, Dow 50,000 is by no means a reflection of stormy GDP growth. It is an indicator that there is enough “fuel” in the system for the debt monster to remain fed.

December 2025: The Hidden Signal That Everyone Missed

Many ask the question: why is the market growing against the background of terrible retail data? The answer lies in the events of December 2025. It was then that the Fed made a statement which many considered routine, but which was in fact a turning point.

The announcement of the commencement of purchasing Treasury bills (T-bills) to maintain “ample reserves” is a veiled form of QE. Behind the bureaucratic term “balance sheet management” lies the Fed’s readiness to provide unlimited liquidity upon first demand.

When data arrives showing 0% growth in retail sales, traders do not get scared. They know: bad news for the economy is excellent news for liquidity. Stagnation unties the Fed’s hands. If the consumer, figuratively speaking, has has run out of steam, it means inflationary pressure will fall. And consequently, one can switch on the printing press at full power. The market grows on expectations of cheap money, not on expectations of sales growth in supermarkets.

The New Reality: Recession Is Cancelled, Devaluation Begins

We have found ourselves in a completely new environment. The economy no longer balances between growth and crisis in the classic sense. Now it balances exclusively between liquidity and inflation.

What does this mean for a sensible investor?

- Crises in the style of “all is lost” no longer exist. Any hint of systemic risk will be flooded with freshly printed trillions. Market falls are prevented by the press of a single key.

- The real risk is inflation. When you flood a fire with money, you save the system from collapse, but you pay for it with the purchasing power of the currency.

- The exchange rate of the currency is secondary. In the conditions of the new monetarism, holding cash is the most dangerous strategy. One needs to own assets that “absorb” excess liquidity.

The “Compressed Spring” of Credit and the Illusion of the Cycle’s End

Everyone says that we are at the “peak of the cycle” and a fall is inevitable. But if we look at the structure of the money supply, we will see a shocking picture: we are not at the peak. We are at the very bottom.

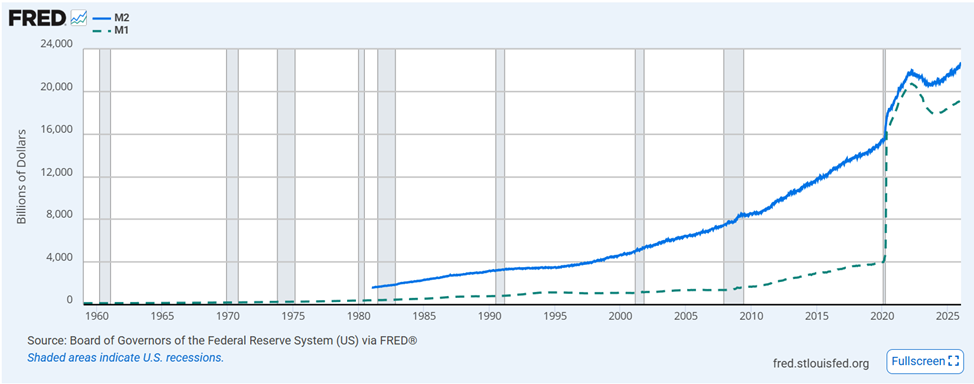

The M1 and M2 Paradox: A Loaded Gun

Over recent years, we have seen a catastrophic convergence of the M1 and M2 aggregates. This means that a huge mass of money in the economy is in its most liquid form. This is “hot money.” It is not locked in instruments, but is ready to pour into the market at any moment.

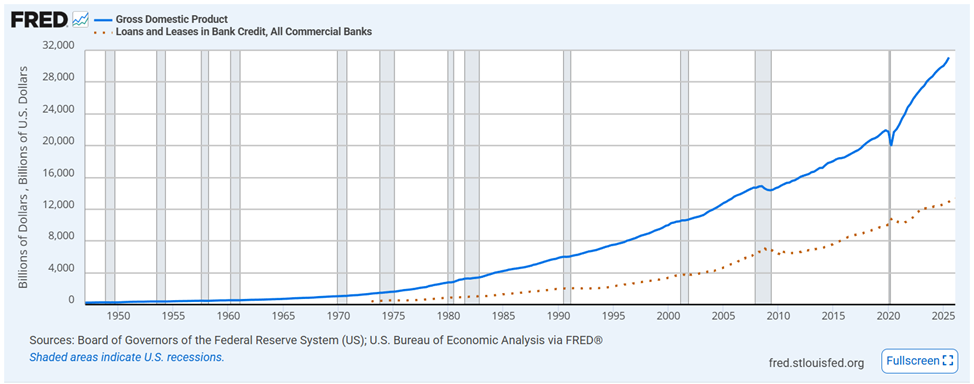

The problem of inflation today is restrained only by a low level of lending. But look at the figures: US GDP has grown, while the credit portfolios of banks have lagged. The economy has grown, while its “credit refueling” has not even taken place yet.

The Money Multiplier: A Trap for the Fed

Recall the basic formula for the money supply:

$M = m \times MB$

(Where $m$ is the multiplier and $MB$ is the monetary base).

The Fed has created a colossal monetary base. While the multiplier is low (banks are afraid to lend), inflation seems manageable. But as soon as the Fed begins to lower the rate, the “spring” will uncoil. Even a slight revival of lending will lead to an explosive growth of the M2 money supply. This will be a real inflationary storm.

The Echo of the ’80s: Growth Through Fire

We may find ourselves in a situation that resembles the 1980s. Then, the economy grew amid high inflation. Soon we may see the same: an explosive growth of nominal GDP against the background of a devaluing dollar.

The regulator will have two paths:

- Panic Braking: Sharply hike rates and guaranteedly crash the economy.

- “Let it burn”: Allow inflation to be above the target (5–7%), while keeping rates moderate. This will allow debts to burn away in the flames of inflation.

If I were in Powell’s place, I would choose the second option. And the market is betting precisely on this. The authorities may simply “let go” of inflation. Especially since already at the end of spring we will have a new Fed head, whom Donald Trump will bring. The development of the situation according to the second scenario will become very likely.

The New Methodology of Management

We must acknowledge: the methodology of management has changed completely.

- Before: The credit market sucked out money = Liquidity deficit = Recession.

- Now: Any risk of a liquidity deficit = Money printing = Asset growth.

Market self-regulation in its old form through cleansing crises no longer works. In the future, “cleansing” will occur through inflation. Debts are not written off; they are devalued. This is the “New Economy.” In it, there is no place for classic downturn cycles.

Conclusion: Do Not Prepare for the Last War

Folks, you may be surprised by the figures, but we are only at the beginning of the journey. Yes, this growth is specific. It is growth in conditions where the theoretical foundations of economics have been rewritten on the fly.

Investors need to fear not a 50% collapse of the S&P 500 index, but that their dollars will lose 50% of their value. We are at the bottom of a credit cycle with a huge supply of “gunpowder.” Do not seek analogies in 1929 or 2008.

The main challenge of the future is not recession. It is the inability of the authorities to cope with the simultaneous growth of the economy and prices. But as long as the press is running — the road upward is open. This battle will be won by liquidity.

Your Business — On AutoPilot with DDImedia AI Assistant

(Join Our Waitlist)

Visit us at DataDrivenInvestor.com

Join our creator ecosystem here.

DDI Official Telegram Channel: https://t.me/+tafUp6ecEys4YjQ1

Follow us on LinkedIn, Twitter, YouTube, and Facebook.

7,000 Points for the S&P 500 and the Triumph of Monetarism: Why Classic Crises Are a Thing of the… was originally published in DataDrivenInvestor on Medium, where people are continuing the conversation by highlighting and responding to this story.