5 Mistakes Forex Traders Make When Withdrawing Funds (And How to Avoid Them)

Beirmancapital12 min read·Just now

Beirmancapital12 min read·Just now--

Struggling with forex withdrawal delays, rejected requests, or hidden fees? Discover the 5 critical mistakes forex traders make when withdrawing funds and how to avoid them for smooth, fast payouts.

You worked hard analyzing charts, managing risk, and finally turning a profit. But when it is time to withdraw your earnings, the process suddenly becomes complicated.

Withdrawal delays. Hidden fees. Rejected requests. Account holds.

Sound familiar?

The truth is, most forex withdrawal problems are 100% avoidable. They happen not because brokers are dishonest (though some are), but because traders skip critical steps that seem unimportant until they are standing between you and your money.

This guide breaks down the 5 most common forex withdrawal mistakes, explains why they happen, and gives you actionable tips to ensure your profits move from your trading account to your bank account without friction.

Beirman Capital Portal | Account

Edit description

client.beirmancapital.com

Why Forex Withdrawals Go Wrong More Often Than You Think

Before diving into the mistakes, it is important to understand the landscape.

The global forex market processes over $7.5 trillion in daily volume. Yet, a surprisingly high number of traders report issues with withdrawals every year. According to various trader review platforms, withdrawal problems are consistently the #1 complaint against forex brokers.

The reasons range from broker negligence to trader error. This guide focuses on what you can control.

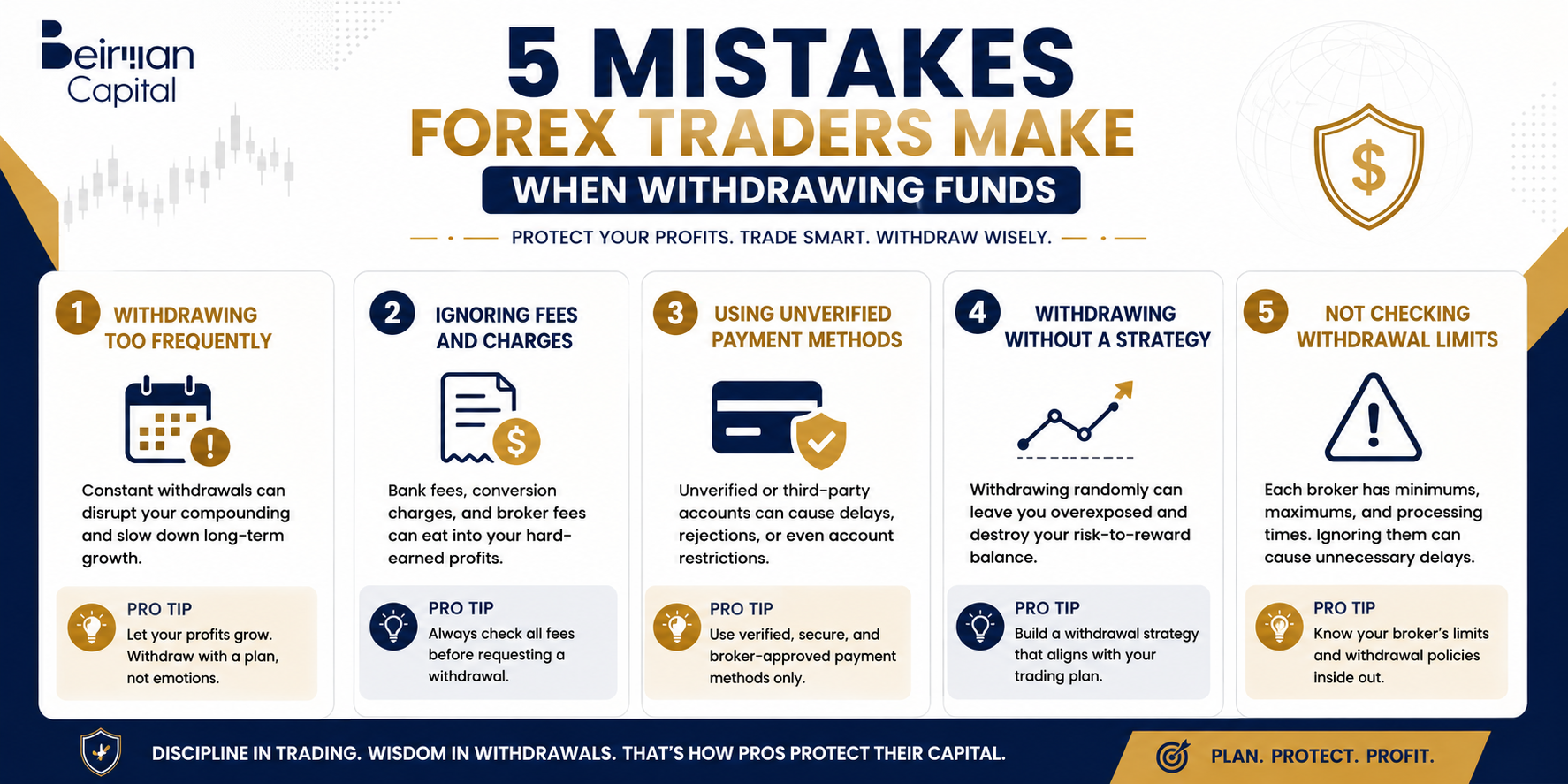

Mistake #1: Not Reading Your Broker’s Withdrawal Policy Before Depositing

This is the most overlooked step in all of forex trading, and it costs traders thousands of dollars every year.

Most traders research a broker’s:

- Spreads

- Leverage

- Trading platforms

- Asset selection

But very few read the withdrawal terms and conditions before depositing real money.

Some brokers also reserve the right to review or delay large withdrawals without prior notice. If you are unaware of this policy, you may interpret a legitimate compliance check as broker fraud — creating unnecessary panic.

The Fix

Read the full withdrawal terms before you make your first deposit. If the broker does not publish clear withdrawal policies on their website, treat that as a serious red flag. Legitimate, regulated brokers are always transparent about how and when you can access your money.

Pro Tip: Copy the withdrawal policy into a document and refer to it every time you plan to request a withdrawal. Rules can also change, so revisit the terms periodically.

Mistake #2: Delaying KYC (Know Your Customer) Verification

KYC verification is the process brokers use to confirm your identity before allowing you to withdraw funds. It is a regulatory requirement enforced by financial authorities worldwide, including:

- FCA (UK)

- ASIC (Australia)

- CySEC (Cyprus/EU)

- FSCA (South Africa)

What KYC Typically Requires

- Government-issued photo ID (passport, national ID, or driver’s license)

- Proof of address (utility bill, bank statement, or government letter — usually less than 3 months old)

- Proof of payment method (a photo of your card or a bank statement)

- Selfie or live verification (some brokers now require biometric confirmation)

Why Traders Get Caught Out

The most common scenario: a trader spends weeks or months building their account. When they finally hit a withdrawal milestone and request their funds, they are suddenly asked to verify their identity.

The documents they submit are:

- Expired

- Blurry or cropped

- In a language not supported by the broker

- Mismatched (name on ID does not match the account name)

This can delay your withdrawal by days or even weeks during a period when you may urgently need your funds.

Worse, if your verification fails multiple times, your account may be flagged for additional review.

The Fix

Complete your KYC verification immediately after opening your account — before you make your first deposit or place your first trade. This way, by the time you are ready to withdraw, there are zero barriers.

Pro Tip: Store digital copies of all your verification documents in a secure folder. Check expiry dates on your ID annually and update your broker immediately if your address changes.

Mistake #2: Delaying KYC (Know Your Customer) Verification

KYC verification is the process brokers use to confirm your identity before allowing you to withdraw funds. It is a regulatory requirement enforced by financial authorities worldwide, including:

- FCA (UK)

- ASIC (Australia)

- CySEC (Cyprus/EU)

- FSCA (South Africa)

What KYC Typically Requires

- Government-issued photo ID (passport, national ID, or driver’s license)

- Proof of address (utility bill, bank statement, or government letter — usually less than 3 months old)

- Proof of payment method (a photo of your card or a bank statement)

- Selfie or live verification (some brokers now require biometric confirmation)

Why Traders Get Caught Out

The most common scenario: a trader spends weeks or months building their account. When they finally hit a withdrawal milestone and request their funds, they are suddenly asked to verify their identity.

The documents they submit are:

- Expired

- Blurry or cropped

- In a language not supported by the broker

- Mismatched (name on ID does not match the account name)

This can delay your withdrawal by days or even weeks during a period when you may urgently need your funds.

Worse, if your verification fails multiple times, your account may be flagged for additional review.

The Fix

Complete your KYC verification immediately after opening your account — before you make your first deposit or place your first trade. This way, by the time you are ready to withdraw, there are zero barriers.

Pro Tip: Store digital copies of all your verification documents in a secure folder. Check expiry dates on your ID annually and update your broker immediately if your address changes.

Mistake #2: Delaying KYC (Know Your Customer) Verification

KYC verification is the process brokers use to confirm your identity before allowing you to withdraw funds. It is a regulatory requirement enforced by financial authorities worldwide, including:

- FCA (UK)

- ASIC (Australia)

- CySEC (Cyprus/EU)

- FSCA (South Africa)

What KYC Typically Requires

- Government-issued photo ID (passport, national ID, or driver’s license)

- Proof of address (utility bill, bank statement, or government letter — usually less than 3 months old)

- Proof of payment method (a photo of your card or a bank statement)

- Selfie or live verification (some brokers now require biometric confirmation)

Why Traders Get Caught Out

The most common scenario: a trader spends weeks or months building their account. When they finally hit a withdrawal milestone and request their funds, they are suddenly asked to verify their identity.

The documents they submit are:

- Expired

- Blurry or cropped

- In a language not supported by the broker

- Mismatched (name on ID does not match the account name)

This can delay your withdrawal by days or even weeks during a period when you may urgently need your funds.

Worse, if your verification fails multiple times, your account may be flagged for additional review.

The Fix

Complete your KYC verification immediately after opening your account — before you make your first deposit or place your first trade. This way, by the time you are ready to withdraw, there are zero barriers.

Pro Tip: Store digital copies of all your verification documents in a secure folder. Check expiry dates on your ID annually and update your broker immediately if your address changes.

Mistake #2: Delaying KYC (Know Your Customer) Verification

KYC verification is the process brokers use to confirm your identity before allowing you to withdraw funds. It is a regulatory requirement enforced by financial authorities worldwide, including:

- FCA (UK)

- ASIC (Australia)

- CySEC (Cyprus/EU)

- FSCA (South Africa)

What KYC Typically Requires

- Government-issued photo ID (passport, national ID, or driver’s license)

- Proof of address (utility bill, bank statement, or government letter — usually less than 3 months old)

- Proof of payment method (a photo of your card or a bank statement)

- Selfie or live verification (some brokers now require biometric confirmation)

Why Traders Get Caught Out

The most common scenario: a trader spends weeks or months building their account. When they finally hit a withdrawal milestone and request their funds, they are suddenly asked to verify their identity.

The documents they submit are:

- Expired

- Blurry or cropped

- In a language not supported by the broker

- Mismatched (name on ID does not match the account name)

This can delay your withdrawal by days or even weeks during a period when you may urgently need your funds.

Worse, if your verification fails multiple times, your account may be flagged for additional review.

The Fix

Complete your KYC verification immediately after opening your account — before you make your first deposit or place your first trade. This way, by the time you are ready to withdraw, there are zero barriers.

Pro Tip: Store digital copies of all your verification documents in a secure folder. Check expiry dates on your ID annually and update your broker immediately if your address changes.

Mistake #3: Using a Different Payment Method to Withdraw Than You Used to Deposit

This is one of the most misunderstood rules in forex trading, and it catches both beginner and experienced traders off guard.

The “Same Source” Rule Explained

The vast majority of regulated brokers enforce a same-source withdrawal policy. This means:

- If you deposited via Visa credit card, your withdrawal must first go back to that same Visa card

- If you deposited via bank wire, your withdrawal must go back to the same bank account

- If you deposited via PayPal or Skrill, your withdrawal must return to that same e-wallet

Only after your original deposit amount has been returned to the source method are you typically allowed to withdraw remaining profits via an alternative method.

Why This Rule Exists

This is not a broker trick. It is an anti-money laundering (AML) compliance requirement mandated by financial regulators globally. The logic is simple: money must return the same way it came in.

Common Payment Methods Compared

Payment MethodDeposit SpeedWithdrawal SpeedTypical FeesCommon IssuesBank Wire Transfer1–3 business days3–7 business daysLow–MediumSlow processing, bank chargesCredit/Debit CardInstant3–5 business daysLowRefund limits, card expiryPayPalInstant1–2 business daysMediumNot available with all brokersSkrill / NetellerInstant1–2 business daysMediumAccount verification requiredCrypto (USDT, BTC)Near-instantNear-instantVery LowPrice volatility risk

The Fix

Use one primary payment method consistently for both deposits and withdrawals. Before depositing, think ahead: will this method still be available and active when you want to withdraw? For example, avoid depositing with a card that is about to expire.

Pro Tip: If you plan to use multiple brokers, maintain a dedicated bank account or e-wallet for forex activity. This keeps your transaction history clean and simplifies any future compliance checks.

Mistake #4: Ignoring Fees, Conversion Costs, and Net Withdrawal Amounts

Many traders focus entirely on their gross profit — the number displayed in their trading account — without calculating what they will actually receive after all deductions.

This disconnect between account profit and actual payout is one of the most frustrating experiences in forex trading.

The Hidden Costs of Forex Withdrawals

Here are the fees that can quietly reduce your withdrawal amount:

1. Broker Withdrawal Fees

Some brokers charge a flat fee (e.g., $25 per wire transfer) or a percentage of the amount withdrawn. These are disclosed in the terms but frequently ignored.

2. Payment Processor Fees

The payment gateway (Skrill, Neteller, bank) that handles the transaction may also charge their own fee, separate from the broker.

3. Currency Conversion Costs

If your trading account is in USD but your bank account is in EUR, GBP, or another currency, conversion fees apply. These are often hidden inside the exchange rate offered (spread), meaning you receive a worse-than-market rate without realizing it.

4. Intermediary Bank Fees

International wire transfers often pass through one or more intermediary banks before reaching your local bank. Each one may charge a fee deducted from your transfer — completely outside of the broker’s control.

5. Receiving Bank Charges

Your own bank may charge a fee for receiving an international transfer.

A Real-World Example

Imagine you withdraw $1,000 from your broker:

DeductionAmountBroker withdrawal fee-$25.00Payment processor fee-$5.00Currency conversion spread (2%)-$20.00Intermediary bank fee-$15.00Receiving bank charge-$10.00Amount received$925.00

A 7.5% reduction before the money even touches your account — and none of these charges are the broker “stealing” from you. They are all disclosed somewhere in the fine print.

The Fix

Before submitting any withdrawal request, calculate your net amount. Ask your broker directly: “What is the total amount I will receive after all fees?” Consolidate withdrawals where possible to reduce the frequency of fixed fees.

Pro Tip: E-wallets like Skrill, Neteller, or crypto transfers (USDT on TRC-20) often have significantly lower fees than bank wire transfers. If your broker supports these methods, they can be more cost-effective for frequent withdrawals.

Mistake #5: Withdrawing at the Wrong Time Open Trades, Margin, and Bonus Conditions

Timing your withdrawal incorrectly is a mistake that can lead to cancelled requests, forced position closures, and even account margin calls.

Problem A: Withdrawing With Open Positions

When you have active trades on the market, a portion of your funds is tied up as margin — a deposit held by the broker to cover potential losses on your open positions.

If you submit a withdrawal request that reduces your account balance below the required margin level, the broker will either:

- Reject the withdrawal request automatically

- Close your open positions to free up the funds (triggering a margin call)

Neither outcome is good, especially if your open trades were profitable and moving in your favor.

Problem B: Bonus and Promotion Conditions

Forex brokers frequently offer deposit bonuses, welcome bonuses, or cashback promotions. These are attractive on the surface but come with strict withdrawal conditions called volume requirements or lot requirements.

For example:

“Receive a 50% deposit bonus. To withdraw bonus funds or profits derived from the bonus, you must complete a minimum trading volume of 30 lots.”

If you withdraw before meeting this condition, the broker is legally entitled to:

- Remove the bonus from your account

- Reject the withdrawal request

- In some cases, recalculate your profit balance without the bonus

Problem C: Withdrawal Timing and Market Hours

Some payment methods are only processed during business hours on business days. A withdrawal submitted on a Friday afternoon may not be processed until the following Monday or Tuesday longer if there is a bank holiday.

The Fix

Before submitting a withdrawal request, run this 3-point checklist:

- Close all open trades or verify that remaining funds exceed margin requirements after the withdrawal

- Check bonus terms and confirm you have met all volume requirements

- Submit withdrawals early in the week (Monday or Tuesday) to avoid weekend processing delays

Pro Tip: Many experienced traders maintain a separate withdrawal buffer — a portion of their account they never trade with — specifically so they can always access a base amount of funds without affecting open positions.

Best Practices for Fast, Smooth Forex Withdrawals

Beyond avoiding the five mistakes above, here are the habits of traders who consistently experience zero withdrawal problems:

Choose a Regulated Broker From the Start

Regulation is your first line of protection. Verify your broker is licensed by a recognized authority:

- FCA (UK)

- ASIC (Australia)

- CySEC (EU)

- FSCA (South Africa)

- NFA/CFTC (USA)

Use independent broker verification platforms to check their status before depositing.

Complete KYC Before Your First Deposit

Do not wait. Verify your identity the moment you open an account.

Standardize Your Payment Method

Pick one method and use it consistently for both deposits and withdrawals.

Keep a Withdrawal Log

Record every withdrawal request with the date, amount, method, and expected arrival date. This creates a paper trail if you ever need to dispute a transaction.

Test With a Small Withdrawal First

Before making a large withdrawal, test the process with a small amount (e.g., $50–$100). This confirms everything works correctly before your major payout.

Maintain a Clean Trading Account

Avoid mixing bonus funds and personal funds if possible. This simplifies compliance and speeds up processing.

Conclusion: Your Profits Are Only Real When They Are in Your Account

Generating consistent profits in forex trading is a remarkable achievement. But the journey is not complete until those profits are safely withdrawn and in your control.

The five mistakes covered in this guide ignoring broker withdrawal rules, delaying KYC, using mismatched payment methods, overlooking fees, and withdrawing at the wrong time are entirely preventable. They are not complicated. They simply require awareness and preparation.

By building good withdrawal habits from the very beginning of your trading career, you protect yourself from unnecessary delays, hidden costs, and frustrating rejections.

At Beirman Capital, transparency and efficiency are not afterthoughts — they are core to how we operate. Our traders benefit from clear withdrawal policies, fast processing, and a support team that guides them through every step of the payout process. Because we believe that when you earn it, accessing it should never be a problem.

Home

Beirman Capital offers leverage & security for Forex, Stocks, Crypto & Currency Trading. Join best brokers and maximize…

beirmancapital.com

Blogs

Beirman Capital has multiple blogs on forex, commodities, stocks, indices, and others. Get well-versed in the trading…

beirmancapital.com

📩 Join Investor’s Handbook Digest — get the best investing, markets, and wealth-building insights each week.